If you're asking "how much superannuation do I need to retire?", you're not alone. This is the most common question Australian pre-retirees face, and the answer isn't as simple as a single number.

The amount of super you need depends on multiple factors: your desired lifestyle, whether you're single or a couple, your expected Age Pension eligibility, and how long you expect to live. Your withdrawal strategy also matters, the wrong approach can run out years early. Let's break it down.

Get Your Free Retirement Readiness Checklist

A quick 15-point checklist to see if you're on track. Plus weekly tips on super, Age Pension, and retirement planning.

No spam. Unsubscribe anytime.

Calculate Your Retirement Needs Now

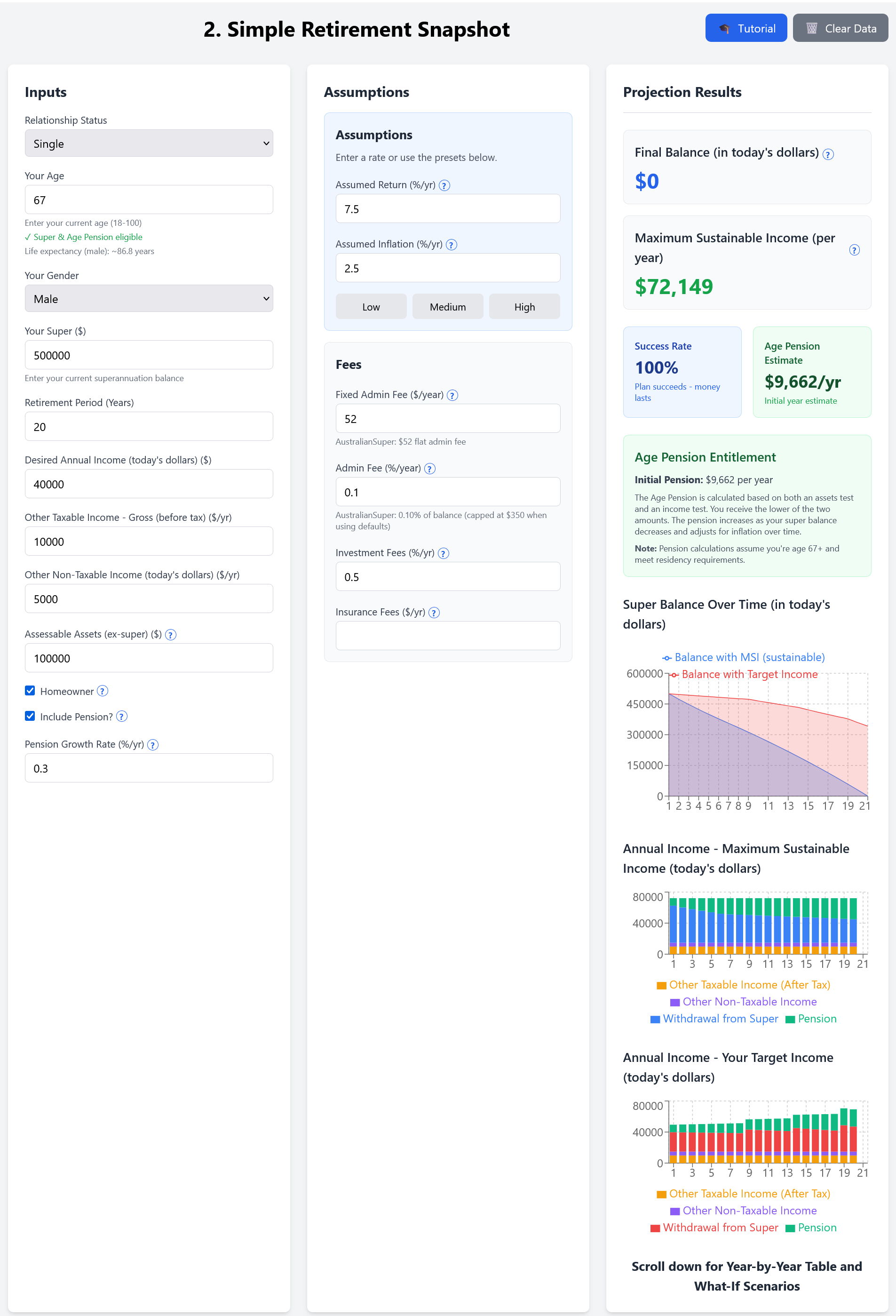

Enter your details and see exactly how much super you need. The calculator uses real market data from 1928, tests against historical crashes, and integrates Age Pension calculations.

Run the 60-Second Stress-TestNo signup required · Instant results · 100% private

The ASFA Retirement Standard (2026)

The Association of Superannuation Funds of Australia (ASFA) publishes retirement standards that provide a benchmark for "comfortable" and "modest" retirement lifestyles. ASFA increased the comfortable lump sums in its 2026 update to $630,000 for a single homeowner and $730,000 for a couple, assuming a part Age Pension.

| Lifestyle | Single (Annual) | Couple (Annual) |

|---|---|---|

| Comfortable | $51,278 | $72,148 |

| Modest | $32,417 | $46,620 |

Comfortable retirement includes private health insurance, a reasonable car, good clothes, a range of electronic equipment, domestic and occasional international travel.

Stress-test the assumption: See your Age Pension and retirement income year by year. Run the 60-Second Stress-Test. Run the Advanced Calculator →

Modest retirement covers basic activities with limited discretionary spending. Think basic transport, limited holidays (mainly domestic), and occasional leisure activities.

How Much Super Do You Need? The Numbers

What's your number? The amounts above are guidelines. Your actual super needs depend on your age, current super balance, expected returns, and lifestyle. Model your exact scenario with the calculator. Calculate how much you need →

For a Comfortable Retirement

Based on the ASFA standard and assuming you qualify for a part Age Pension, here are the super balances you'd need at retirement (age 67):

Comfortable Retirement Super Requirements

- Single person: $630,000 in super

- Couple: $730,000 combined super

These figures assume you own your home outright and will receive some Age Pension.

For a Modest Retirement

If you're content with a modest lifestyle and expect to qualify for the full Age Pension:

Modest Retirement Super Requirements

- Single person: $100,000 - $150,000 in super

- Couple: $150,000 - $200,000 combined super

With lower super, you'll rely more heavily on the Age Pension to meet modest living standards.

The Age Pension Impact

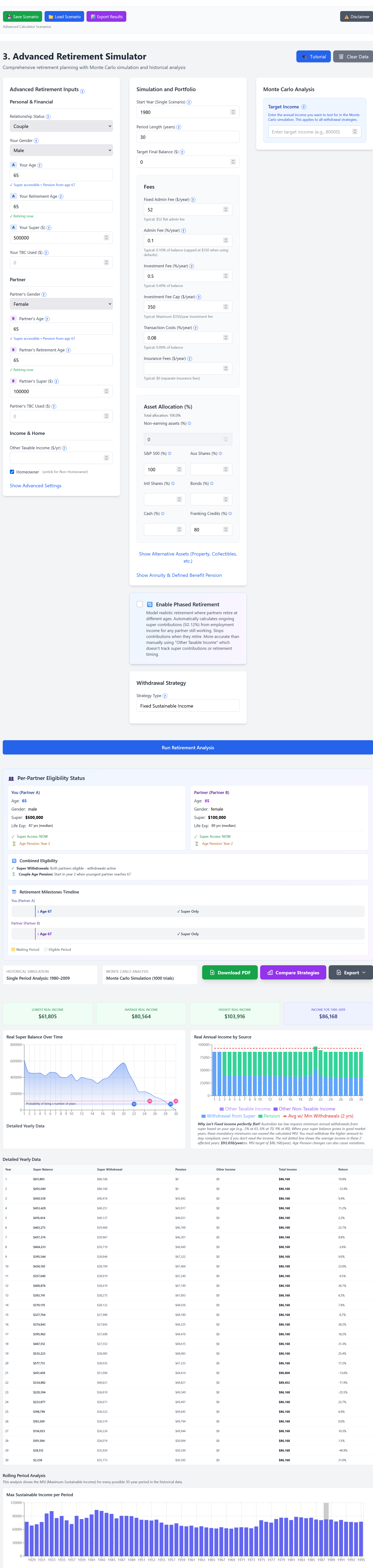

Model your own retirement scenario with SuperCalc Pro

The Australian Age Pension is a critical component of retirement income for most Australians. As of 2025-26, the maximum fortnightly Age Pension rates are:

- Single: $1,200.90 per fortnight ($31,223 per year)

- Couple (combined): $1,810.40 per fortnight ($47,070 per year)

However, the Age Pension is means-tested. Both your assets and income are assessed, and you receive whichever test results in a lower pension amount.

Age Pension Asset Test Thresholds (2025-26)

For homeowners, the asset test free areas are:

- Single: $327,000 (full pension) to $727,000 (zero pension)

- Couple: $490,500 (full pension) to $1,093,500 (zero pension)

If your assessable assets exceed these limits, your Age Pension is reduced by $3 per fortnight for every $1,000 over the threshold (above the free area).

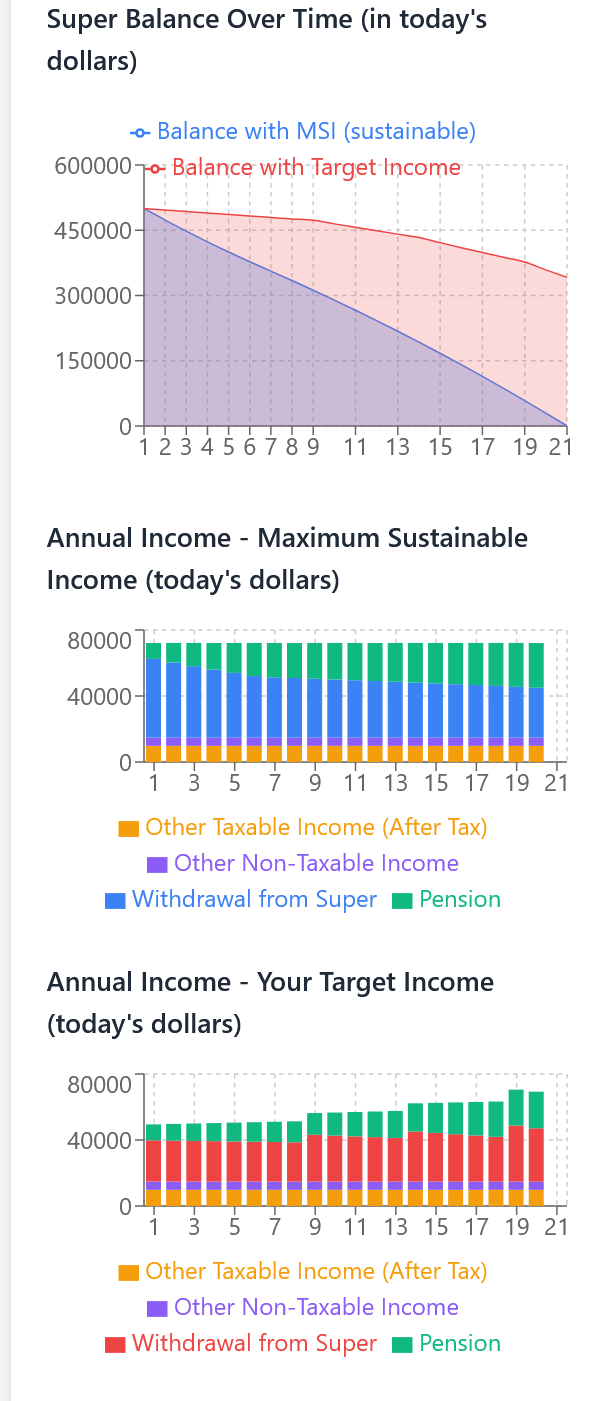

How super drawdowns and Age Pension combine over retirement

Real-World Examples

Example 1: Sarah, Single Homeowner

Situation: Sarah is 67, single, owns her home, and has $400,000 in super.

Strategy:

- Assets $73,000 over threshold ($400K - $327K) = pension reduced by ~$5,700/year

- Qualifies for part Age Pension (~$25,000/year after asset test)

- Withdraw ~$26,000/year from super to reach comfortable lifestyle

- Total income: ~$51,000/year

- Super lasts approximately 20+ years with conservative 5% returns, then full pension kicks in

Result: Sarah can maintain a comfortable lifestyle. As her super depletes, her Age Pension increases automatically.

Example 2: John & Mary, Couple Homeowners

Situation: John (68) and Mary (66) own their home and have $650,000 combined super.

Strategy:

- Assets $159,500 over threshold ($650K - $490.5K) = pension reduced by ~$12,400/year

- Qualify for part Age Pension (~$34,000/year after asset test)

- Withdraw ~$38,000/year from super

- Total household income: ~$72,000/year (comfortable lifestyle)

- Super lasts approximately 25+ years, then full pension kicks in

Result: John and Mary achieve a comfortable retirement with security well into their 90s.

Example 3: David, Single Non-Homeowner

Situation: David is 67, rents, and has $300,000 in super.

Challenge: Non-homeowners have higher asset test thresholds ($590,000 for singles). David's $300,000 is below this, so he passes the assets test. However, the income test (using deeming) slightly reduces his pension. His $300K is deemed to earn ~$7,700/year ($64,200 at 1% + remainder at 3%), which is ~$2,000 over the $5,668 free threshold.

Strategy:

- Receives near-full Age Pension (~$30,000/year after income test reduction)

- Withdraw ~$18,000/year from super to supplement

- Total income: ~$48,000/year

- After rent (~$15-20K): $28,000-$33,000 for living expenses (modest lifestyle)

- Super lasts 20+ years as a supplement to pension

Which example sounds like you? Sarah had $400K, John & Mary had $650K, David had $300K. Every situation is different. Model your exact scenario with your super balance, age, and lifestyle goals. Calculate your personalized retirement plan →

Result: David maintains a modest lifestyle. His near-full pension provides a secure base, with super providing extra comfort.

Factors That Affect Your Super Needs

1. Life Expectancy

Australians are living longer. Current life expectancy at age 67 is:

- Males: 85 years (18 years in retirement)

- Females: 88 years (21 years in retirement)

Planning to age 90-95 is prudent, especially if you have good health and longevity in your family.

2. Investment Returns in Retirement

Your super doesn't stop growing when you retire. Common retirement investment strategies return:

- Conservative (70% bonds, 30% shares): 4-5% p.a. after fees

- Balanced (50/50 bonds/shares): 5-6% p.a. after fees

- Growth (70% shares, 30% bonds): 6-7% p.a. after fees

Higher returns allow your super to last longer, but come with higher volatility and risk.

3. Inflation

Inflation erodes purchasing power over time. At 3% inflation, $50,000 today will need to be $67,000 in 10 years to maintain the same lifestyle. The Age Pension is indexed to inflation, providing some protection.

4. Healthcare Costs

Healthcare expenses typically increase in later retirement (ages 75+). Budget an additional $5,000-$10,000/year for health insurance, medications, and dental/optical care.

5. Unexpected Expenses

Major home repairs, car replacement, or helping adult children can impact retirement plans. A buffer of 10-15% above your desired income is wise.

Test your retirement plan against real historical market data from 1928 onwards

Common Retirement Planning Mistakes

1. Underestimating Longevity

Planning only to age 80 when you might live to 95 is a recipe for running out of money. Use conservative longevity estimates.

2. Ignoring the Age Pension

Many Australians qualify for at least a part Age Pension. Failing to factor this in leads to over-saving or excessive frugality in retirement. Read our complete guide to the Age Pension asset test to understand the current thresholds and how to maximise your entitlement.

3. Withdrawing Too Much Early

Taking large amounts in the first years of retirement (for travel, renovations, etc.) can significantly shorten how long your super lasts.

4. Not Considering Tax

Super withdrawals after age 60 are tax-free in pension phase. However, other income (rental, part-time work) is still taxable. Plan accordingly.

5. Forgetting About the Transfer Balance Cap

If you have a large SMSF, the Transfer Balance Cap ($2.0M in 2025-26) limits how much you can transfer to pension phase. Excess amounts remain in accumulation phase and are taxed at 15%.

How to Think About Your Personal Retirement Needs

Rather than relying only on generic figures or rules of thumb, many people find it useful to think about their own retirement needs in terms of:

- Your desired annual income - Looking at current spending and how it might change in retirement (for example, fewer work costs but more leisure)

- Your current super balance - Using your latest statement as a starting point

- Years until retirement - How long you expect to keep contributing

- Expected investment returns - Both before and during retirement, noting that these are always uncertain

- Age Pension eligibility - Considering how the asset and income tests might apply to you

- Other assets and income - Such as rental properties, part-time work, annuities or other investments

Next Steps

Now that you understand how much super you might need, here are your next actions:

- Calculate your retirement goal - Use the calculator to model your specific situation

- Check your current super balance - Log into your super fund to see where you stand

- Increase contributions if needed - Salary sacrifice or after-tax contributions can boost your balance

- Review your investment strategy - Ensure your super is invested appropriately for your time horizon

- Consider professional advice - A licensed financial adviser can provide personalized strategies

What it costs to keep modelling

Run Advanced Retirement free first. Unlimited scenarios, historical stress tests, and PDF exports are $149 a year, or $14.99 a month if you’d rather not commit upfront, typically less than one hour of paid advice for the same modelling work.

Run the Advanced Calculator →No card required to try it. Subscribe only if the model is useful enough to keep using.