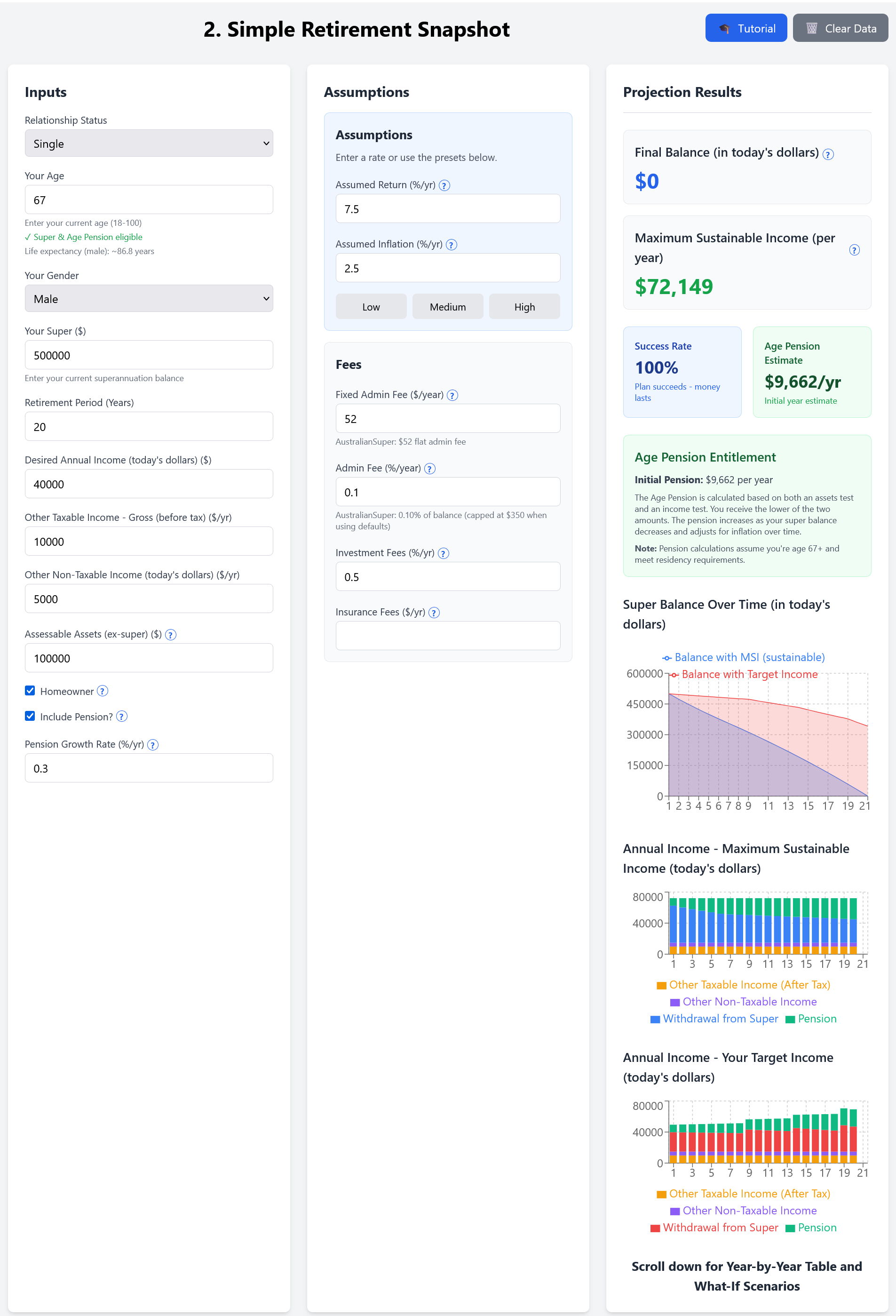

Important: This article is general educational information only. It is not personal advice, not financial product advice, and not a recommendation. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services License (AFSL). Rules and thresholds can change. If you need advice for your situation, speak to a licensed financial adviser.

The Age Pension asset test counts most of what you own. But some assets are completely exempt. Understanding what is exempt can make a significant difference to your pension entitlement. For the full picture of thresholds and how the test works, see our Age Pension asset test guide and the taper trap.

The biggest exemption is your home. But there are others that matter. Here is what Centrelink excludes from the asset test.

Your principal home

Your principal home is completely exempt from the Age Pension asset test. This is the most valuable exemption for most people.

The exemption applies to the home you live in. It does not matter how much the home is worth. A $500,000 home is exempt. A $5 million home is also exempt. The value does not count toward the asset test.

You can own up to two hectares of land around your home. This is roughly five acres. If you own more than two hectares, the excess land is assessable. But the home itself and the first two hectares remain exempt.

If you move into aged care, the home exemption continues for up to two years. After two years, the home becomes assessable unless your spouse or dependent child still lives there.

Key point: Your home is exempt regardless of value. This is why homeowners have lower asset test thresholds than non-homeowners. The home exemption is built into the threshold differences.

$5M home? Exempt. $150K car? Exempt. But that $50K in savings? Assessable. Knowing what counts and what doesn't can mean thousands in pension payments. Calculate your exact entitlement →

One motor vehicle

One motor vehicle is exempt from the asset test. This includes cars, motorcycles, and other vehicles used for personal transport.

If you own multiple vehicles, only one is exempt. The others count toward the asset test at their market value.

The exemption applies regardless of the vehicle's value. A $5,000 car is exempt. A $150,000 luxury car is also exempt. But if you own two cars, the second one counts toward your assets.

This exemption is straightforward. One vehicle, fully exempt. Additional vehicles, assessable.

Funeral bonds up to $15,000

Funeral bonds are exempt up to a combined value of $15,000. This exemption applies to prepaid funeral arrangements.

If you have $10,000 in funeral bonds, that is fully exempt. If you have $20,000 in funeral bonds, the first $15,000 is exempt and the remaining $5,000 counts toward the asset test.

This exemption encourages people to prepay funeral expenses. It is a legitimate way to reduce assessable assets while covering future costs.

Life insurance policies

Life insurance policies are exempt from the asset test. This includes term life insurance, whole of life insurance, and other life insurance products.

The exemption applies to the surrender value of the policy. If you have a life insurance policy with a $50,000 surrender value, that $50,000 is exempt.

This exemption is often overlooked. Many people do not realize their life insurance policies are exempt assets.

Funeral bonds, life insurance, car exemptions—they add up. Optimizing your exempt vs assessable assets could increase your pension by $5,000-15,000/year. See your optimized strategy →

Accommodation bonds in aged care

If you pay an accommodation bond to enter aged care, that bond is exempt from the asset test. This exemption applies while you are in aged care.

The exemption recognizes that accommodation bonds are not liquid assets. You cannot access that money while you are in care.

This is different from accommodation charges, which are ongoing fees. Accommodation bonds are lump sum payments that are exempt.

Personal effects and household contents

Personal effects and household contents are generally exempt, but there is a catch. Centrelink uses reasonable estimates for these items.

Normal household contents like furniture, appliances, and personal items are exempt. But if you own valuable collectibles, artwork, or jewelry worth more than $10,000, those items may be assessable.

In practice, Centrelink rarely assesses household contents unless you declare valuable items. But if you own expensive artwork or collectibles, those should be declared and may count toward the asset test.

What is not exempt

Most other assets count toward the asset test. This includes:

- Superannuation balances (if you are pension age)

- Bank accounts and term deposits

- Shares and managed funds

- Investment properties

- Business assets

- Boats, caravans, and other vehicles beyond the first one

- Valuable collectibles and artwork (over reasonable thresholds)

These assets all count toward the asset test thresholds. The more you have, the more your pension reduces.

Strategic implications

Understanding exempt assets helps you structure your finances effectively.

If you are a homeowner, your home is your biggest exempt asset. This is why homeowners have lower asset test thresholds. The exemption is built into the threshold calculation.

If you are planning to downsize, consider the impact. Selling your exempt home and moving the proceeds to super converts an exempt asset into an assessable one. This can reduce your pension entitlement.

Funeral bonds can be a legitimate way to reduce assessable assets. If you have spare cash and want to reduce your assessable assets, prepaying funeral expenses up to $15,000 is exempt.

Life insurance policies are exempt. If you have life insurance with a surrender value, that value does not count toward the asset test.

Remember: The asset test applies the lower result of the asset test and income test. Even if you have assets above the threshold, you might still qualify for pension if your income is low enough.

See how exempt assets affect your Age Pension entitlement

How the Advanced Calculator helps: The app applies the correct exemptions (home, one car, etc.) and projects your pension year by year. Open the Advanced Calculator

Calculate your Age Pension entitlement

See how exempt and assessable assets affect your pension payment.

Run the 60-Second Stress-TestDisclaimer: This article is for general informational and educational purposes only and does not constitute financial product advice or a recommendation. SuperCalc Pro Pty Ltd (ABN 31 692 042 872) does not hold an Australian Financial Services License (AFSL). The information provided does not take into account your personal circumstances, financial situation, or needs.

Before making any financial decisions, consider whether the information is appropriate for your circumstances and consider seeking professional advice from a licensed financial adviser. Tax and super rules can change. All investments carry risk.