Important: This article contains factual educational information only. It is not financial

product advice, personal financial advice, or a recommendation. SuperCalc Pro does not hold an AFSL and

cannot tell you what to do. Always seek advice from a licensed financial adviser who can consider your

personal circumstances. This article describes what retirement planning involves; it does not tell you whether

any approach is suitable for you.

To be clear: Scott Pape has done more for Australian financial literacy than almost anyone.

His advice is sound for the vast majority of people. This article is about where general accumulation principles

end and where retirement-specific planning begins. It's not a critique. It's a factual description of different

planning stages.

The Barefoot Investor recommends a simple approach: choose a low-cost industry fund (Hostplus Indexed Balanced),

set and forget, don't tinker. For someone in their 30s or 40s building wealth, this is excellent advice. The

logic is sound: low fees, diversification, long time horizon, consistent contributions. It works because the

mathematics of accumulation favors simplicity.

But there's a problem. Building wealth and drawing down wealth are different problems. The same way that the

physics of a rocket going up differs from a rocket coming down, accumulation and decumulation have different

dynamics. You can't use the same approach for both and expect optimal results.

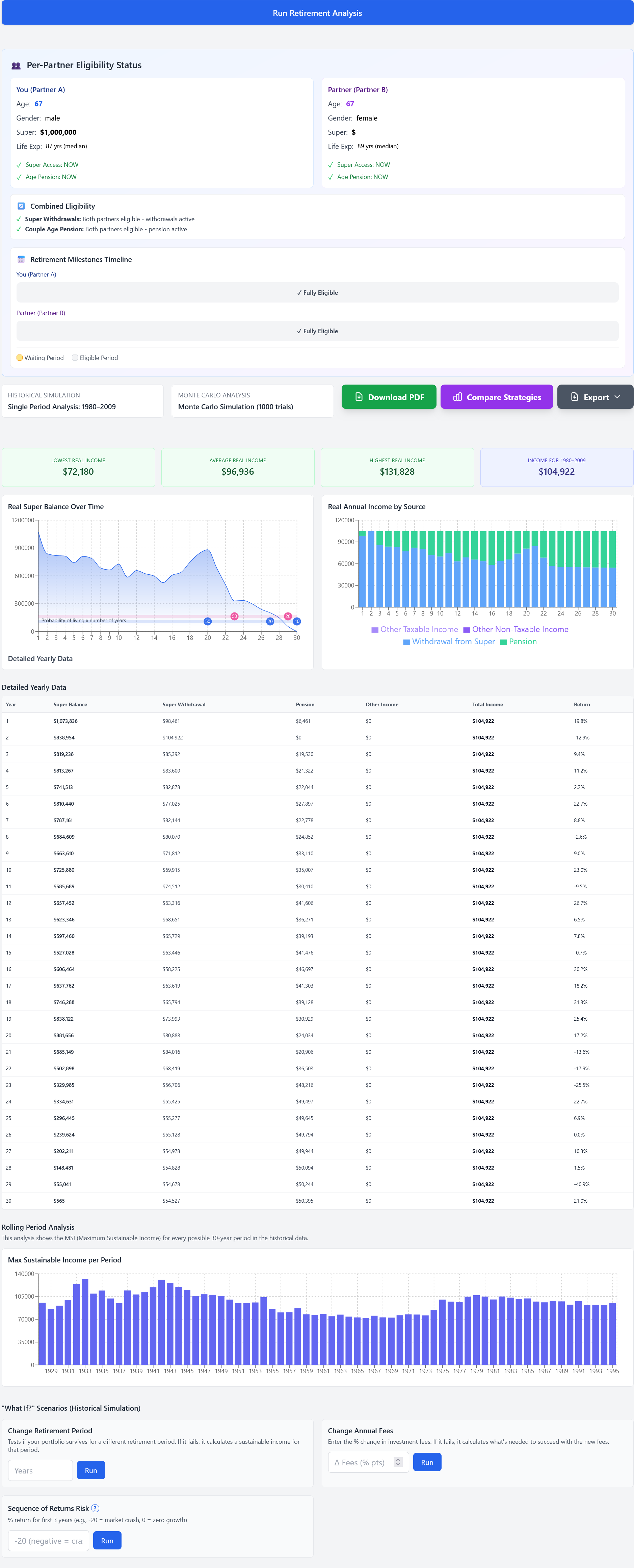

How the Advanced Calculator helps: The app projects drawdown phase with Age Pension and real market sequences. You see how long your balance lasts and what sustainable income looks like against 98 years of data. Run the 60-Second Stress-Test to model your decumulation.

The Logical Flaw in "Set and Forget" for Retirement

Consider this scenario. You're 65, retiring with $1 million in Hostplus Indexed Balanced (roughly 70% growth assets).

The fund has served you well for 30 years. Markets crash 30% in your first year of retirement. Your balance drops

to $700,000, and you're withdrawing $50,000 per year to live on.

Now compare that to someone who retired in a different year, with markets up 15% in their first year. Their balance

grows to $1.15 million while they withdraw the same $50,000. Same starting point, same strategy, wildly different

outcomes. This is sequence of returns risk, and it's not a theory. It's mathematics.

The "set and forget" approach that worked brilliantly during accumulation now exposes you to the most critical

risk of retirement. A 30-year-old experiencing a market crash simply keeps contributing monthly at lower prices.

A 65-year-old withdrawing monthly has no such luxury. The damage is permanent.

What Accumulation Strategies Don't Address

Scott Pape's book is intentionally simple. That's its strength. But simplicity means not covering everything.

Here's what accumulation-focused advice typically doesn't address:

Age Pension integration. The Age Pension applies two tests: an asset test and an income test.

The asset test reduces your pension by $3 per fortnight for every $1,000 over the threshold. That's a 7.8%

annual taper rate. Your super balance directly affects how much pension you receive. Accumulation advice doesn't

model this because it's not relevant yet.

Withdrawal strategy selection. You can withdraw a fixed dollar amount each year. You can withdraw

a fixed percentage. You can use dynamic strategies that adjust based on performance. You can implement guardrails

or floor/ceiling approaches. Each produces different results for income stability and portfolio longevity.

Accumulation advice doesn't cover this because you're not withdrawing yet.

Transfer Balance Cap management. The $2 million Transfer Balance Cap limits tax-free pension

phase balances. Amounts above this remain taxed at 15% in accumulation phase. Personal caps depend on when you

first entered pension phase due to proportional indexation. Accumulation advice doesn't address this because

it's a pension-phase issue.

Couples with different retirement dates. One partner retires at 60, the other at 67. Household

income management during that transition, partial Age Pension eligibility, super balance equalisation, tax

implications. These aren't covered in accumulation-focused advice because both partners are still working.

Historical stress testing. What if you retired in 1929? 1973? 2008? Testing your specific plan

against every historical retirement period shows worst-case outcomes. Accumulation advice doesn't do this because

time heals most wounds when you're still contributing.

Barefoot works for accumulation. Retirement needs Age Pension, TBC, withdrawal strategies. Model YOUR complete retirement plan beyond "set and forget."

Plan your retirement strategy →

The Mathematics Are Different

Here's the fundamental issue. During accumulation, you're optimizing for "how much will I have?" During retirement,

you're optimizing for "how long will it last?" Those are different mathematical problems.

Accumulation favors high growth asset allocation because crashes are recovered through continued contributions and

time. A 30% crash followed by recovery is just a buying opportunity. Retirement doesn't have that luxury. A 30% crash

in year one, combined with withdrawals, creates a hole you may never recover from.

Consider two retirees. Both have $1 million. Both experience the exact same average returns over 25 years, let's say

7% per year. But Retiree A gets those returns in one order (crash first, boom later), while Retiree B gets them in

the opposite order (boom first, crash later). They will end up with vastly different balances. This is mathematically

provable. It's not speculation, it's arithmetic.

Super fund projections (the kind that say "you'll have $1.2 million at retirement") smooth returns into averages.

They assume you get 7% every single year. Real markets don't work that way. Some years are +20%. Some are -30%.

The order matters enormously when you're withdrawing.

The Downsizer Contribution Example

Let's take a specific example that illustrates the gap between accumulation advice and retirement planning.

People aged 55+ can contribute up to $300,000 from selling their home under downsizer contribution rules.

This contribution doesn't count toward any caps, doesn't require work tests, applies regardless of total

super balance.

The Barefoot Investor doesn't discuss this. Not because it's wrong or irrelevant, but because the book focuses

on accumulation for younger people. Downsizer contributions are a retirement-phase consideration. Whether

putting $300,000 into super is right for any individual depends on their circumstances, Age Pension implications,

cash flow needs, estate planning goals.

That's the difference. Accumulation advice is broad and applicable to many. Retirement planning is specific

and depends on individual circumstances. Both are valuable, but they solve different problems.

Sequence of returns risk. Age Pension tapers. TBC limits. Accumulation advice doesn't cover these. Model YOUR retirement with all variables.

Calculate your retirement plan →

Testing the Logic

Here's a thought experiment. Let's assume you could have a retirement calculator that tested your exact plan

against every historical period since 1928. Every possible retirement start year. Every market crash. Every

combination of Age Pension rules and super balances. It would show you the worst case, the best case, the median.

Now, if someone said "you don't need that, just keep your money in Hostplus and withdraw $50,000 per year,"

what would be the logical response? If the calculator showed the same result as the simple approach, you'd

ignore the calculator. But if the calculator showed materially different results, say showing that $50,000

per year would deplete your balance by age 80 in the worst historical scenarios, would you still ignore it?

That's the question accumulation-focused advice doesn't answer. Not because the advice is wrong for accumulation,

but because it's answering a different question. "How do I build wealth?" versus "How long will my wealth last?"

The key point: Accumulation strategies and retirement strategies are solving different

problems. You build wealth one way. You manage drawdown another way. The same approach optimized for

both is mathematically unlikely.

Testing retirement plans against historical periods shows outcomes that averaging masks

Where Licensed Advice Comes In

Here's what this article cannot do: tell you whether any of this applies to you. That requires personal financial

advice from someone holding an AFSL. They can assess your specific circumstances, recommend strategies, provide

Statements of Advice, take responsibility for ensuring recommendations are appropriate.

This article describes what retirement planning involves. It explains why accumulation and retirement are different

problems. It outlines what calculations exist. But it cannot, and does not, tell you what to do. Only a licensed

adviser who knows your situation can do that.

The Barefoot Investor provides excellent accumulation advice for the majority of Australians. Retirement planning

exists as a separate field because the problems are different. Whether you need retirement-specific planning is

not a question this article can answer. That's what licensed advisers are for.

Retirement Planning Calculators

Educational tools that perform the calculations described in this article: historical testing, Age Pension

modeling, withdrawal strategy comparison. These are educational tools only, not personal advice.

Run the 60-Second Stress-Test

Disclaimer: This article contains factual educational information only. It is not financial

product advice, personal financial advice, or a recommendation. SuperCalc Pro does not hold an Australian

Financial Services Licence (AFSL). This article:

• Does not consider any person's objectives, financial situation, or needs

• Does not recommend any product, strategy, fund, or approach

• Does not suggest when, whether, or why any concept might apply to any individual

• Cannot replace licensed financial advice

No Affiliation: We have no affiliation with The Barefoot Investor, Scott Pape, Hostplus,

or any financial advice provider. This article is not a critique or endorsement of any person, book, fund,

or strategy.

Before making any financial decisions, seek advice from a licensed financial adviser (AFSL holder), read

relevant Product Disclosure Statements, and ensure advice considers your personal circumstances. Past

performance does not guarantee future results.