An SMSF that made perfect sense when you were 55 might not make sense when you're 85. Circumstances change. Health declines. A spouse passes away. The compliance burden starts to feel overwhelming, or the fund balance drops to a point where the fixed costs no longer stack up. When that happens, closing your SMSF and rolling into a retail or industry fund can be the right call.

Closing an SMSF is not as simple as stopping. There is a formal wind-up process. Skip it and you can end up with ongoing compliance obligations, ATO penalties, and a mess that costs a lot to fix. This is how to close your SMSF properly.

When to Consider Closing

The decision to close an SMSF is often triggered by a change in circumstances rather than a sudden realisation that it was a bad idea. Understanding the common triggers helps you recognise when it might be time.

Health or cognitive decline is perhaps the most common trigger. Being an SMSF trustee requires mental capacity. You're making investment decisions, signing documents, and ensuring compliance with complex regulations. If you or your fellow trustee (often a spouse) are experiencing cognitive decline, the trustee duties become impossible to fulfil properly. Rather than risk compliance breaches or poor investment decisions, it's better to roll to a fund where professionals handle everything.

The death of a member, particularly in a two-member fund, often prompts closure. The surviving spouse may not want to manage the fund alone, or may not have the knowledge or interest to do so. While you can appoint a professional trustee or add a new member, many people simply find it easier to close the fund and move on.

A falling balance can make SMSFs uneconomic. The fixed costs of running an SMSF (audit, accounting, ASIC fees, ATO levy) typically run $2,000 to $5,000 per year regardless of balance. When your fund was $800,000, that was 0.25% to 0.6% of assets. If the balance has dropped to $200,000, those same costs now represent 1% to 2.5%, and that can be more than you'd pay in an industry fund.

Sometimes people simply tire of the administration. The compliance burden of SMSFs is real: annual audits, investment strategy reviews, trustee minutes, contribution tracking, pension documentation. Some people enjoy this involvement; others find it a chore. If maintaining the fund feels like a burden rather than an opportunity, that's a signal worth heeding.

Family conflicts can make SMSFs untenable. If the trustees (often spouses) are separating, or if there are disputes between members about investment strategy or fund management, the fund may need to be wound up as part of resolving the conflict.

Moving overseas creates complications. SMSFs have residency requirements. The fund must be an Australian resident, which generally requires Australian-resident trustees and central management in Australia. If you're moving overseas permanently, maintaining an SMSF becomes problematic or impossible.

The Wind-Up Process

Winding up an SMSF is a multi-step process that typically takes three to six months. Rushing it leads to mistakes; taking too long extends the period of compliance obligations and costs.

The process begins with a formal trustee decision. Hold a trustee meeting, discuss the reasons for winding up, and document the decision in minutes. The minutes should record who was present, the reasons for the decision, and the proposed process and timeline. This documentation matters. It shows the wind-up was a considered decision by the trustees, not an abandonment of the fund.

Next, you need to convert assets to cash or arrange transfers. Most receiving funds (industry and retail funds) only accept cash rollovers, so you'll typically need to sell all investments. Shares can be sold through your broker; term deposits can be broken (possibly with a penalty); property must be sold on the open market. If the receiving fund accepts in-specie transfers (some do for listed securities), you can transfer assets directly without selling, which may save brokerage and avoid crystallising capital gains.

Before you can wind up, all fund liabilities must be paid. This includes any outstanding accountant or audit fees, ASIC fees, ATO supervisory levy, and any taxes owing. The fund must have zero liabilities. You can't wind up with debts outstanding. Make sure you've budgeted for final-year costs, including the wind-up audit and final tax return preparation.

A final audit is required, covering the period from the last audit to the wind-up date. Even if you're winding up mid-year, you need an audit. The auditor will verify that the wind-up has been conducted properly, that all assets have been dealt with appropriately, and that there are no outstanding compliance issues.

Once assets are liquid and liabilities are paid, you roll member benefits to the receiving fund. This is done through the standard rollover process. The receiving fund will provide forms, and you'll need to complete a rollover benefits statement. Make sure you have the receiving fund details correct; rolling to the wrong fund creates complications.

The final SMSF annual return must be lodged, marked as a "final return". That notifies the ATO that the fund has wound up. Pay any tax owing. The return will calculate any final tax liability. Once the final return is lodged and any tax paid, the ATO will cancel the fund's ABN.

Finally, close the fund's bank accounts. There's no point keeping them open once everything is done. But don't close them too early. You need the accounts to receive the final asset sales and pay the final liabilities.

Do not just stop: An SMSF that stops operating without proper wind-up is still legally required to lodge annual returns and meet compliance obligations. The ATO actively pursues non-lodging funds, and the penalties accumulate. If you're not going to wind up properly, you're creating a problem that will only get worse.

Costs of Winding Up

Winding up an SMSF isn't free. You should budget for a final audit, which typically costs $500 to $1,000. That's similar to a regular audit, though some auditors charge more for wind-up audits because of the extra work involved. Accountant fees for preparing final financial statements and the final tax return typically run $1,000 to $2,500, depending on the complexity of the fund.

If you're selling assets, there may be brokerage fees (for shares) or agent fees (for property). There may also be capital gains tax if assets have appreciated. CGT is at the concessional super rate of 10% for assets held more than 12 months, or it can be zero if the fund is entirely in pension phase.

All up, expect to pay $2,000 to $4,000 to wind up a straightforward SMSF, potentially more for complex funds with property or other complications. This is a one-time cost that ends the ongoing annual costs of running the fund.

Key insight: The wind-up cost ($2K-$4K) is usually one-time. But if you stay in the SMSF, you pay $2K-$5K annually. After one year of not closing, the annual fees often exceed the one-time wind-up cost. Use the calculator to see: at your current balance, how many years until annual SMSF costs exceed your wind-up cost?

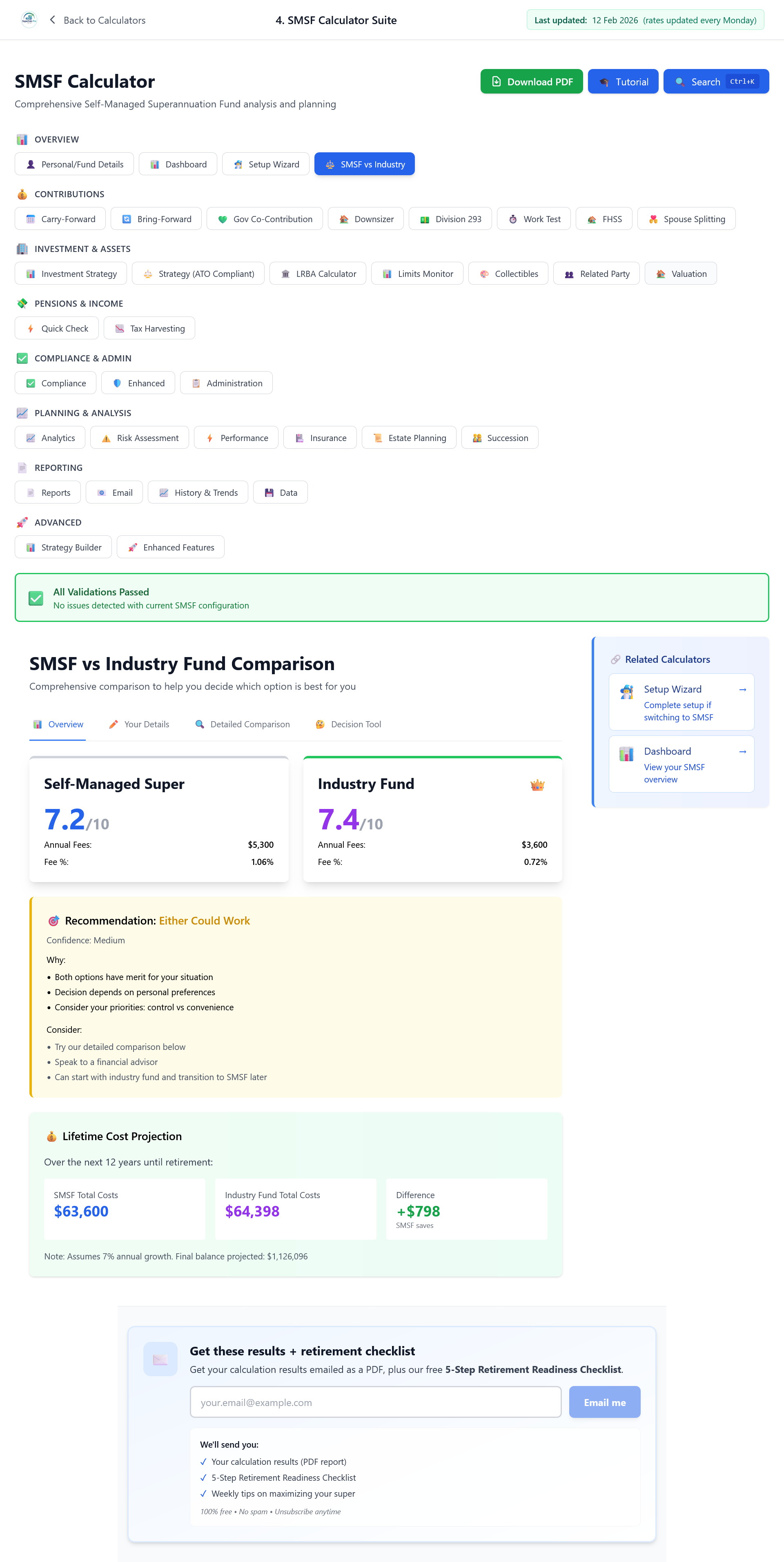

Use our calculator to model your specific costs. The SMSF Suite lets you input your fund balance, estimate wind-up costs, and compare ongoing fees to an industry or retail fund. Run different scenarios (balance at $200K, $500K, $1M) to see when the fixed costs of running an SMSF stop making sense. It's the fastest way to know if closing is financially the right move.

SMSF Suite: Compare SMSF running costs vs industry fund fees to find your breakeven point at different balances.

Where to Roll Your Super

When you close your SMSF, you need somewhere for the money to go. The main options are industry funds, retail funds, or another SMSF.

Industry funds like AustralianSuper, Hostplus, or Australian Retirement Trust offer low fees, simple administration, and decent investment options. They're a good default choice for people who want to stop thinking about their super. You won't have the control of an SMSF, but you also won't have the responsibility.

Retail funds offer more investment choice and features, but typically at higher fees. They might suit someone who wants some control over investment selection without the full compliance burden of an SMSF.

Rolling to another SMSF makes sense in some cases. You might be consolidating with a spouse's fund, or setting up a new fund with a different structure (for example a corporate trustee). But if you're closing your SMSF because you're tired of the compliance burden, rolling to another SMSF defeats the purpose.

What Happens to Your Pension

If you're receiving a pension from your SMSF, the pension must be dealt with as part of the wind-up. Generally, this means commuting the pension (converting it back to a lump sum) and then rolling that lump sum to the receiving fund.

You can start a new pension in the receiving fund if you want to continue receiving retirement income. Be aware that this can have Transfer Balance Cap implications. Commuting a pension creates a debit to your transfer balance account, and starting a new pension creates a credit. If your circumstances have changed since you started the original pension, you may have more or less TBC space available.

The transition doesn't have to interrupt your income. You can time the rollover and new pension commencement to minimise any gap in payments. Discuss the timing with both your SMSF administrator and the receiving fund to ensure a smooth transition.

Keeping Records

Even after your SMSF is wound up, you need to keep records. The law requires SMSF records to be kept for at least 10 years (some records for 5 years). This includes the trust deed and any amendments, all financial statements and tax returns, audit reports, trustee minutes, member statements, and records of contributions and benefit payments.

Store these records securely. If the ATO ever queries something about your former fund, even years later, you'll need to be able to produce the relevant documents. Digital storage is fine, but make sure you have backups.

Pro tip: Start the wind-up process early. It typically takes three to six months to properly close an SMSF, and rushing creates mistakes. If you're thinking about closing due to health concerns, don't wait until the situation is critical. Start the process while you're still able to manage it properly.

Don't guess - calculate your wind-up costs and compare fees

Our SMSF Suite calculates what it costs to close your fund, compares it to industry and retail fund fees for your specific balance, and shows you the breakeven point. Model your scenario in 2 minutes. Educational tool only; we don't recommend whether to wind up. That's for you and your adviser.

Open the SMSF SuiteDisclaimer: This article is general information only and does not constitute financial, tax or legal advice. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). Winding up an SMSF has legal, tax and financial implications. You should consult a licensed SMSF specialist, accountant and, where appropriate, a licensed financial adviser before proceeding. We do not recommend whether you should open, close or change any super fund. That is a decision for you based on your own circumstances and professional advice.