Most retirement calculators quietly assume a neat household: both partners retire together, both draw super together, and Age Pension arrives as a single event. Real households are messier. One partner may leave work at 60 because of health, redundancy, or burnout while the other keeps working to 65 or 67. A five-year age gap can turn a simple retirement projection into a staged cash-flow problem.

Why Standard Calculators Fail

A typical calculator asks for one retirement age. That is the problem. A phased retirement has years where one partner works and one does not, where one super balance is accessible and the other is still preserved, and where Age Pension eligibility may apply to only part of the household. The order of withdrawals matters because the younger partner's balance may still be compounding while the older partner is already drawing income.

The Cost of Using Standard Calculators for Phased Retirement

Here's what happens when you use a standard calculator for a phased retirement scenario:

Real Example: The 5-Year Gap

Couple: Partner A (60, retiring now, $500K super), Partner B (55, retiring at 60, $300K super, $80K salary)

Standard Calculator Result:

- Assumes both retire at 60

- Combined super: $800K

- Sustainable income: $40K/year

- Problem: Doesn't account for Partner B working 5 more years

Phased Retirement Result:

- Years 1-5: Partner A draws $30K/year, Partner B works and contributes

- At Year 6: Combined super = $850K (Partner B contributed $50K)

- Sustainable income: $52K/year

- Benefit: +$12K/year = +$360K over 30 years

The gap: Using a standard calculator for phased retirement can underestimate your sustainable income by 15-30%. That's $10K-20K per year you're missing — or $300K-600K over a 30-year retirement.

Why this happens: standard calculators flatten a household into one date and one combined balance. That misses the years where salary, preservation age, super withdrawals and pension eligibility are all changing at once.

Basic free calculators are useful for rough orientation, but they rarely model this household transition properly. If your ages, work dates and balances differ, the answer can be directionally wrong even when the arithmetic inside the calculator is correct.

Common Phased Retirement Scenarios

Scenario 1: Age Gap Couple

John (62) and Sarah (55) want to retire together. John can access super now, but Sarah can't until 60. For the next 5 years, they'll rely primarily on John's super while Sarah continues working part-time.

Planning challenge: How fast can John draw down without running out before Sarah's super kicks in?

Scenario 2: Staggered Retirement

Mike (58) and Lisa (56) are the same age, but Mike wants to retire at 60 while Lisa loves her job and will work until 67. For 7 years, Lisa's salary covers expenses while Mike's super grows untouched.

Planning challenge: Should Mike start a TTR pension? When should they start drawing his super?

Scenario 3: Health-Driven Early Retirement

David (57) has health issues and needs to stop work. His wife Emma (54) will work until 65. They need David's super to supplement Emma's income for 8 years before both are fully retired.

Planning challenge: Can David access super early? How do they bridge the gap?

Key Considerations for Phased Retirement

1. Preservation Age Matters

Each partner can only access their own super when they reach preservation age (60 for most). If one partner is 58 and the other is 62, only the older partner's super is accessible.

2. Whose Super to Draw First?

Generally, draw from the older partner's super first because they have access earlier, allowing you to start withdrawals as soon as possible. The younger partner's super has more time to grow if left untouched, potentially generating significant additional returns over the years before it's needed. Drawing from the older partner's super first may also help with Age Pension timing, as it can help equalise balances and optimise your pension entitlement when both partners eventually qualify.

3. Age Pension Timing

You can't get Age Pension until 67. If one partner reaches 67 while the other is still working, the working partner's income affects the pension. This creates complex interactions.

4. Income Phases

The household can move through several income phases: both working, one working, both retired before pension age, one partner eligible for Age Pension, then both eligible. Each phase changes the pressure on super. That is why phased retirement is not just a softer name for retiring slowly; it is a different modelling problem.

The key insight: Phased retirement isn't just about when you stop work. It's about coordinating two people's super access, income needs, and pension eligibility across multiple phases.

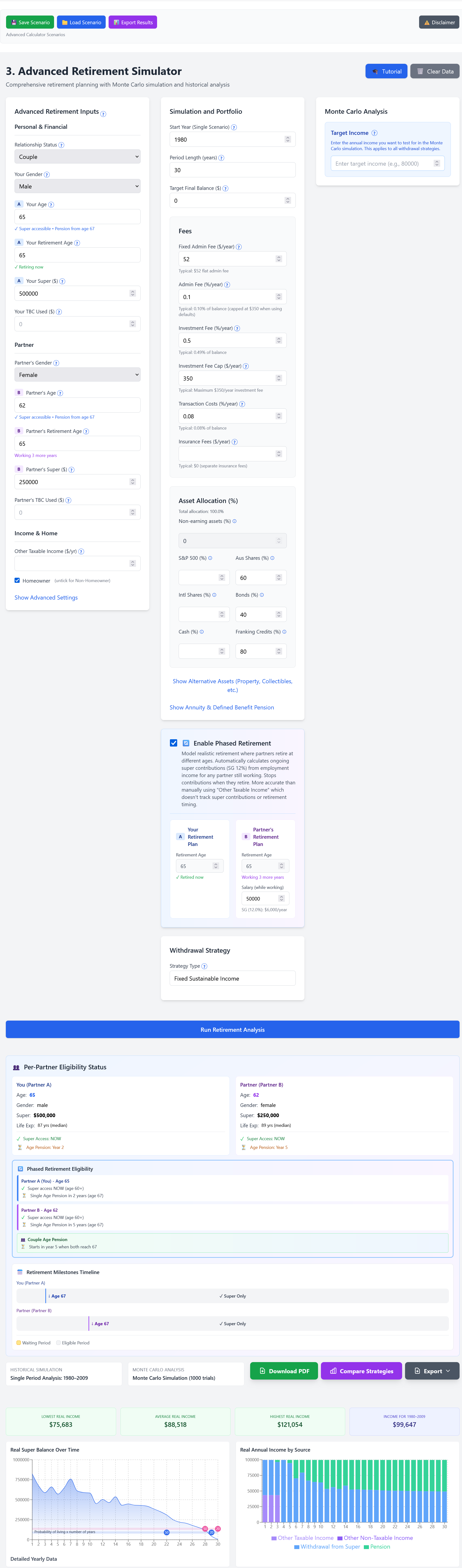

Show the advanced calculator with couple inputs and different retirement ages

The Value of Phased Retirement Planning

Phased retirement is not only about timing. It is about seeing which years are doing the financial work. In some households the working partner's salary protects the retired partner's super. In others, the early retiree's withdrawals eat too much capital before the second balance is available.

How it works: when one partner keeps working, salary and ongoing super contributions can reduce the drawdown pressure on the household. The benefit is not automatic. It depends on spending, whose super is accessible, and whether work income delays or reduces Age Pension support.

Real-World Impact

Scenario: A couple where Partner A retires at 60 and Partner B works to 65.

- Standard calculator: "You can spend $45K/year" (assumes both retire at 60)

- Phased retirement calculator: "You can spend $58K/year because Partner B's contributions during those 5 years increase your final balance"

Result: That's $13K more per year — or $390K over 30 years. Standard calculators miss this entirely.

Bottom line: If you and your partner are retiring at different ages, you need phased retirement planning. Standard calculators will underestimate your income — sometimes by hundreds of thousands of dollars over your retirement.

Planning Tips

Effective phased retirement planning requires several strategic considerations that go beyond simple retirement calculators.

Start by modelling each phase separately. Your income needs will change dramatically depending on whether one partner is working or both are retired. When one partner works while the other is retired, you need to calculate what income you need from the retired partner's super to supplement the working partner's salary. When neither partner works but both are under Age Pension age, you're entirely reliant on super withdrawals. When one partner reaches 67 and qualifies for Age Pension while the other doesn't, you have a mixed income structure. Each phase has different expenses, different income sources, and different tax implications. Calculating what you need in each phase helps you understand how much super you need and when you need it.

Consider a Transition to Retirement (TTR) pension for the working partner. This can provide significant tax benefits while allowing them to access some super while still contributing. A TTR pension allows you to draw between 4% and 10% of your super balance each year while still working, which can help you reduce your taxable income and potentially access some super earlier than you otherwise could. This is particularly useful when one partner has retired and needs income, but the other partner is still working and could benefit from the tax advantages of a TTR pension.

Equalise balances if one partner has much more super than the other. If one partner has $1.5 million and the other has $300,000, you're missing opportunities for better Age Pension eligibility and more flexible withdrawal strategies. Consider spouse contributions or contribution splitting to balance the accounts. Spouse contributions allow you to contribute to your partner's super and potentially claim a tax offset. Contribution splitting allows you to transfer some of your concessional contributions to your spouse's account. These strategies can help equalise balances, which can improve your Age Pension eligibility and give you more flexibility in deciding whose super to draw from first.

Finally, plan for the surviving spouse scenario. What happens if one partner dies early? This is a difficult question, but it's essential for proper planning. You need to understand how super death benefits work — typically, the super balance passes to the surviving spouse tax-free, but the income structure changes dramatically. Age Pension rates change for singles, which can significantly impact the surviving partner's income. A couple might receive $1,777 per fortnight in Age Pension, but a single person receives only $1,191. This reduction, combined with the loss of one partner's super income, can create a significant income gap. Ensuring the surviving partner has sufficient income to maintain their lifestyle requires careful planning, including potentially taking out life insurance, ensuring super death benefit nominations are up to date, and understanding how the surviving partner's income will change.

Run your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator