What is preservation age?

Preservation age is the earliest age at which you can usually access preserved super if you also meet a condition of release. For most Australians now approaching retirement it is age 60, but access still depends on retirement, ceasing work after 60, starting a transition-to-retirement income stream, or another approved release condition.

Super is designed for retirement, so there are rules about when you can access it. The key concept is "preservation age", the earliest age at which access is usually possible if another condition is also met. For the practical impact of retiring at 60, including the seven-year gap before Age Pension, see the retire at 60 guide. Once money starts coming out, drawdown strategy becomes the next question.

Put numbers around the 60-to-67 gap: Enter your age, balance, and target retirement date to see the years before Age Pension starts. That bridge is the part many early-retirement plans underestimate. Open the Advanced Calculator →

The practical risk cuts both ways. Some people wait longer than necessary because they confuse super access with Age Pension age. Others get tempted by early-access schemes before they meet a real release condition. The rule itself is not complicated, but the timing matters.

Preservation Age is Now 60 for Everyone

Preservation age is now 60 for all Australians. The old birth-year table mattered when some people had preservation ages between 55 and 60. That transition has passed. If you are planning access now, the live question is no longer "which preservation age applies to me?" It is "have I met a condition of release?"

Simple rule: You can access your super when you turn 60 AND meet a condition of release (usually ceasing employment).

That distinction matters most for people thinking about finishing work at 60. Super may be accessible, but Age Pension age is still 67. A seven-year bridge can be easy to underestimate if the plan only asks whether super can be opened.

Key Ages Explained

Age 60: Preservation Age

At 60, access is possible only if a condition of release is met. The common practical route is ceasing an employment arrangement after turning 60. That does not necessarily mean never working again; it means the specific employment arrangement has ended. A transition-to-retirement pension is another route while still working, but it has its own limits, including the 10% annual withdrawal cap.

Age 65: Unrestricted Access

At 65, the work test falls away for access purposes. You can still be working full-time and access super. That is why age 65 is a clean planning line in a way age 60 is not.

Age 67: Age Pension Age

This is when you may become eligible for the Age Pension (subject to assets and income tests). It's separate from super access but important for retirement planning.

Many people confuse Age Pension age with super access age, but they are different:

- Super access: Can start at 60 (with conditions) or 65 (unrestricted)

- Age Pension: Eligibility starts at 67 (subject to means testing)

Conditions of Release

Before 65, preservation age alone is not enough. A release condition still has to be satisfied. In ordinary retirement planning, the two common conditions are permanent retirement and ceasing an employment arrangement after age 60.

Ceasing Employment

This is the point that often gets lost. Ceasing employment is about ending an employment arrangement, not proving that you will never work again. Someone who leaves one job after turning 60 may be able to access preserved super even if they later take different work. That flexibility can be useful, but it is also exactly why the paperwork and fund rules matter. The fund needs to be satisfied that a valid condition of release has actually occurred.

Permanent Retirement

If you're permanently retiring (not planning to work again), you can access your super once you reach preservation age (60).

Age 65: Automatic Access

At age 65, you gain automatic access to your super regardless of work status. There's no need to retire or cease employment. This is full, unrestricted access that applies to everyone.

Special Conditions for Early Access

There are also special conditions for early access in exceptional circumstances:

- Terminal Illness: If you have a terminal illness with a life expectancy of less than 24 months, you can access your super early.

- Permanent Incapacity: Meaning you're unable to ever work again, also qualifies for early access.

- Severe Financial Hardship: This is another condition, though it has strict criteria and typically allows only limited access. You generally need to be receiving certain government benefits and unable to meet reasonable living expenses.

- Compassionate Grounds: Cover specific circumstances like:

- Paying for medical treatment that isn't covered by insurance

- Preventing foreclosure on your home

- Paying for palliative care

- Making payments on a loan to prevent foreclosure

These special conditions require evidence and approval from your super fund and/or the ATO.

Tax on Super Withdrawals

Understanding the tax treatment of super withdrawals is important for planning:

| Age | Tax Treatment |

|---|---|

| Under preservation age | Generally can't access (except special conditions) |

| Preservation age to 59 | Tax-free up to low-rate cap ($235,000), then 15% + Medicare |

| 60 and over | Tax-free (from taxed super funds) |

Key Points:

- Once you turn 60, withdrawals from taxed super funds are generally tax-free

- The low-rate cap ($235,000) applies if you access super between preservation age and 59

- Untaxed super funds (like some public sector funds) may have different tax treatment

- Always check with your super fund about the tax treatment of your specific account

Early Access: Be Careful

Some promoters claim they can help you access super early through various schemes. Be very cautious about this: illegal early access schemes exist and carry severe penalties.

How to Spot Illegal Schemes

Red flags:

- Someone offers to help you access super early for a fee

- Promises to "get around" the rules or use "loopholes"

- Pressure to act quickly or sign documents immediately

- Vague explanations about which condition of release you're using

- Requests for super fund login details or personal information

- Claims that sound too good to be true

If someone claims they can get you early access, they're either lying or running an illegal scheme. There are no secret loopholes.

Consequences of Illegal Access

Penalties include:

- Fines of up to $15,000+ (or more for serious cases)

- Tax on the entire withdrawn amount plus penalties

- The scammer taking 20-40% of your super as their "fee"

- Criminal prosecution (yes, participants get prosecuted, not just promoters)

- Permanent damage to your retirement savings

The ATO actively pursues these schemes. A promised shortcut can become tax, penalties, and a permanent loss of retirement savings. If you do not meet a release condition, wait until you do or get advice through proper channels.

How to Verify Legitimate Access

Always verify any claims with:

- The ATO (Australian Taxation Office)

- A licensed financial adviser

- Your super fund directly

If someone offers to help you access your super early, ask:

- What specific condition of release do I meet?

- Can you provide written documentation?

- What are the fees and charges?

- What are the tax implications?

Remember: Legitimate early access is only available through the official conditions of release we've discussed. If someone offers to help you access your super early for a fee, or suggests ways to "get around" the rules, they're likely operating an illegal scheme.

Planning Your Super Access

The planning takeaway is simple but easy to misapply. Age 60 is the earliest ordinary access point, not a guarantee of unrestricted access. Age 65 is unrestricted access. Age 67 is Age Pension age, subject to means testing. A good retirement plan keeps those three ages separate instead of treating them as one retirement date.

For some households, the most realistic path is neither full retirement at 60 nor waiting untouched until 67. It is a staged exit: reduce work, use super carefully, and preserve enough capital to handle the years before Age Pension is available. Whether that works depends less on the access rule itself and more on spending, balance, and the first few years of market returns.

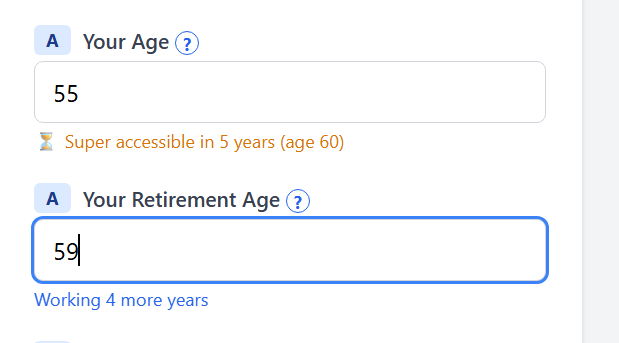

Calculator interface showing retirement age input field and how preservation age (60) is used in calculations

Plan Your Super Access Strategy

Access at 60, 62, or 65? Model the tax treatment, Age Pension timing, and income sustainability for the access path you are considering.

Run the 60-Second Stress-TestRun your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator