Important: This article is general information only, not financial product advice. SuperCalc Pro does not hold an Australian Financial Services Licence. Consider your own circumstances and seek advice from a licensed adviser before acting.

If you have ever seen a retirement projection based on “7% per year” or a smooth line on a chart, you have seen a model that mostly ignores sequence of returns risk, the same limitation our piece on Monte Carlo versus reality describes when tools smooth out volatility. In the real world, returns arrive in a messy order. For Australian retirees drawing an account-based pension from super, that order can matter as much as the long-run average, which is why historical stress tests (for example around the GFC) matter alongside long-run averages. Two people with identical balances, identical spending, and identical average returns can end up with wildly different outcomes, because one retired into a bull market and the other retired into the teeth of a crash.

This article explains what sequence risk is, why it hits retirees harder than workers still contributing, how it fits the Australian system (super, minimum drawdowns, Age Pension), and what you can do to stress-test your plan using real historical paths, not fantasy smooth curves. For how spending rules interact with balance over time, see super drawdown strategies in an Australian context.

Plain English: Sequence of returns risk means when you earn returns matters, not just how much on average, once you start selling investments to live on.

Who this matters most for

Sequence risk bites hardest when market-linked drawdowns fund a large share of living costs, spending is relatively fixed compared with the balance, and there is little cash buffer. Typical profiles:

- Heavily self-funded retirees or those with balances well above Age Pension assets tests, where super drawdowns must cover material spending.

- Higher withdrawal rates (spending as a percentage of starting balance) and limited ability to cut spending after a crash.

- Growth-heavy portfolios through the first years of retirement without de-risking or a cash runway.

Often less central: households where the Age Pension already covers most living costs and super is supplementary. Total cashflow can depend more on Centrelink rules than on whether equities rose a few percent in a given year (though investment risk never disappears).

What is sequence of returns risk?

Sequence of returns risk is the possibility that the order of investment returns will damage your retirement outcome even when the long-term average return looks fine. Imagine two sequences over ten years: both average 6% per year. In one sequence, the first three years are strongly negative (like a global financial crisis at the start of retirement). In the other, those same negative years happen at the end, when your balance is smaller and you have fewer years left to fund.

The arithmetic average does not change. The experience of the retiree changes completely. In the bad-early-years path, you sell more units at depressed prices to raise the same annual income. You lock in losses. You hold fewer shares for the eventual recovery. That is sequence risk in one sentence: withdrawals plus volatility plus bad timing.

Why order matters more than the average

While you are working and making regular contributions, bad years are partly offset by buying more units when prices are low. Time is on your side; you are not forced to sell a fixed dollar amount every year to eat. In the years just before and after retirement (the so-called retirement risk zone) you often flip from buyer to seller. The same market crash has a different mechanical effect: you must sell assets to fund living costs, and if the portfolio is down, each dollar of spending consumes more of the remaining capital.

Financial planners sometimes illustrate this with two hypothetical retirees who experience the exact same annual returns, but in reverse order. One path ends in ruin; the other funds a long retirement. The average return was identical. Only the sequence differed.

Large drawdowns early, while spending is high and the balance is largest

Strong returns early, building a buffer before weaker years

Same inputs, different start year: numbers from the Advanced engine

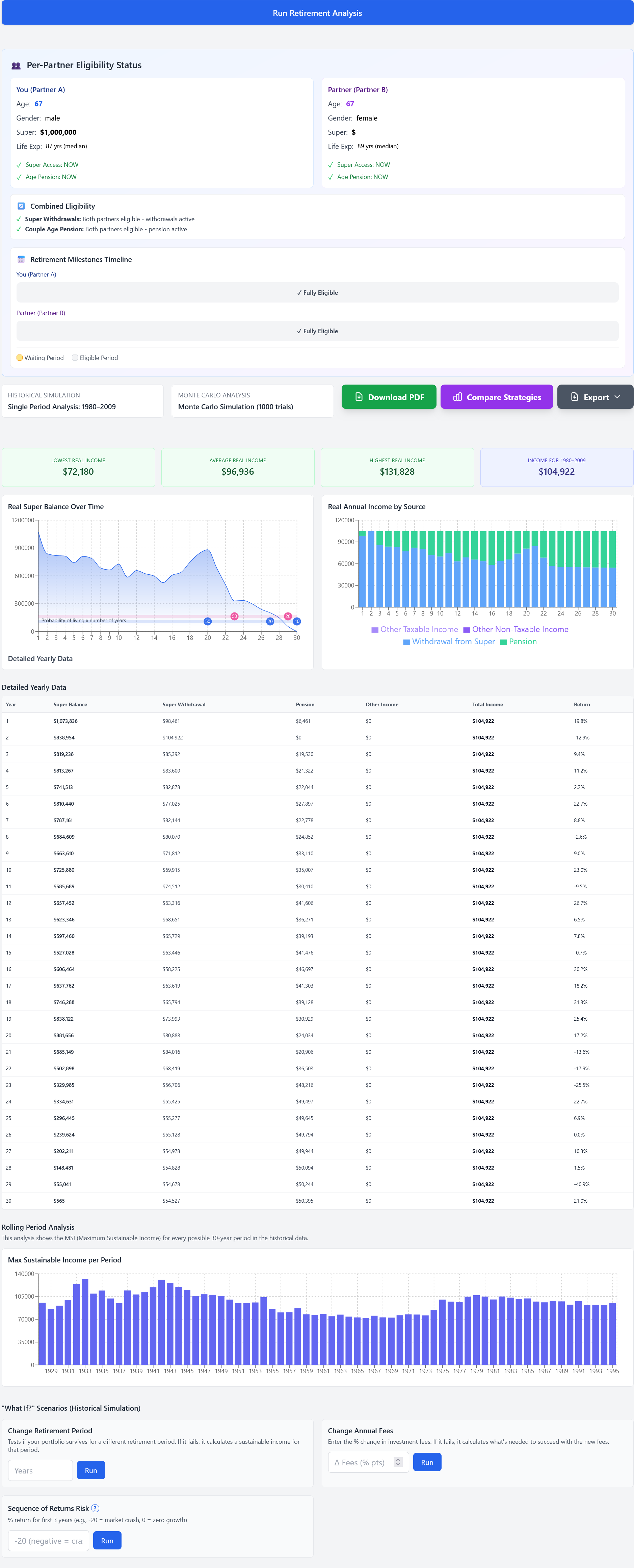

These numbers were run through the same historical market and inflation series that power SuperCalc Pro’s Advanced Calculator (Australian and global data from 1928 to 2025). We used a typical balanced mix with fixed weights that match the calculator’s balanced preset: 35% US equities, 15% Australian shares, 20% international shares, 20% bonds, and 10% cash, plus 0.5% a year in investment fees (adds to 100%). Each year’s return is adjusted for that year’s Australian inflation so we are not pretending prices stayed flat while markets moved. Spending starts at $50,000 in the first year and rises each year in line with CPI so your standard of living in the model stays about the same. For this table only, we left out Age Pension and tax, so you can see the pure effect of when the good and bad years arrived, not other parts of the system.

Two retirees both start with $800,000 in super and withdraw on the same rules. The only difference is which historical years they retire into first: one begins in 2007 (GFC arrives early in retirement), the other in 2012 (stronger years first). Both runs last 12 calendar years (2007–2018 vs 2012–2023).

Why these dates and twelve years? These two windows sit toward the stark end of what the data can show: one path hits a severe global downturn very early; the other leads with several stronger years first. They bracket one of the sharpest ordering contrasts in the dataset, not a randomly mild pair of periods. The twelve-year length keeps both runs on an identical horizon for a fair comparison and fits within the years available after each start date before the historical series ends (it is not a recommendation that your retirement lasts exactly twelve years). The point is not that every retiree will face a gap anywhere near this size, but that the ordering effect is real and measurable.

| Retirement start (1 Jan) | Ending super (after 12 years) |

|---|---|

| 2007 (global financial crisis early in the sequence) | ~$167,100 |

| 2012 (recovery years before later volatility) | ~$552,500 |

| Gap (same average “long-run” story, different order): about $385,400 more super left on the 2012 path than the 2007 path, holding behaviour identical. | |

How to verify: Open the Advanced Calculator, set a balanced portfolio, turn off Age Pension if you want to mirror this stripped-down check, enter $800k and spending in that ballpark, and compare historical stress using different retirement start years. Your exact balance will differ if you include pension, fees, couples, or different allocations, but the ordering effect is what this table is meant to show.

Sequence risk and Australian super

Australia’s retirement system has layers: accumulation phase, transition to retirement, account-based pensions, Age Pension, possibly defined benefit or annuity income. Sequence risk sits squarely in the years when you depend on drawdowns from market-linked super. If you hold a diversified portfolio in pension phase (as most SMSFs and public offer funds do), you are exposed to volatility. Minimum drawdown rules for account-based pensions force a minimum percentage out each year based on age; many retirees draw more than the minimum for living costs. Either way, you are converting balance to cash on a schedule that interacts with whatever the market did last quarter.

When the Age Pension dominates the picture

For many Australians with modest-to-moderate super, once Age Pension eligibility begins, total retirement cashflow can depend more on Centrelink rules than on whether investment markets had a good or bad year. If assessable assets fall, you may receive more pension under the assets test, reducing how much you must withdraw from super to meet spending. In that cohort, investment sequence still matters for balance and bequests, but the marginal effect on annual income can be smaller than for someone with large balances above pension thresholds who must self-fund most of retirement.

That is not a reason to ignore markets: taper rates, income tests, deeming, and the partner rules all interact. But it is a reason to model super and pension together. Relying on a gut feel that “the pension will fix it if shares crash” without numbers is risky; assuming sequence risk is equally catastrophic for everyone is also misleading.

Lifecycle and MySuper vs a growth-heavy SMSF

Not every retiree enters pension phase with the same risk profile. MySuper and many lifecycle products gradually dial down growth exposure as members age, reducing peak-to-trough swings exactly when sequence risk is highest. By contrast, a self-managed fund or choice account left in high-growth investments through retirement takes more sequence risk by design. Same average return assumption, different glide path and different depth of drawdowns. Your fund’s design is part of the story.

Phased retirement and timing of pension phase

Many Australians do not flip from full-time work to 100% pension-phase drawdown overnight. Transition-to-retirement strategies, part-time work, or delaying full drawdown changes when you sell units and how much you need from super each year, so sequence risk interacts with work income and the timing of moving assets to pension phase. Contribution splitting, spouse balances, and staggered retirements within a couple add further moving parts. A single “retirement date” in a spreadsheet rarely matches real life. See also transition to retirement for the rules context.

Inflation and real returns

Sequence risk is not only about nominal share prices. The 1970s in many countries combined weak real returns with high inflation. Retirees needed more cash each year just to stand still. Stress-testing only nominal balances without thinking about real (after-inflation) spending can understate how bad periods felt. When you model retirement, the dangerous stretches are often bad real outcomes, not a single bad calendar year in isolation.

A concrete example: the GFC and why outcomes varied

Consider retirees who moved fully into pension phase around 2007 with meaningful equity exposure. The global financial crisis brought large negative returns in 2008 and into 2009. Whether that was devastating or manageable depended heavily on withdrawal rate, asset allocation, and flexibility, not on “2007” alone. A diversified investor who held through the drawdown, could trim discretionary spending, and did not need to realise large losses at the trough often saw balances recover over the 2010s. Someone with a high fixed spending target relative to balance, a concentrated growth allocation, or forced selling to meet rigid costs faced a harsher path. Comparing a 2007 retirement start with a 2012 start illustrates path-dependence; it does not prove that every diversified 2007 retiree suffered “permanent damage” relative to long-run averages.

The structural lesson stands: retirement start date, spending as a share of balance, glide path into defensive assets, and whether you can reduce drawdowns after a crash all interact with path-dependent risk. The GFC is a useful Australian-relevant stress episode; it is not a verdict on every portfolio.

Why “average return” calculators mislead

Many simple calculators project your balance forward using a constant return every year. That assumption wipes sequence risk off the map entirely. It is convenient for marketing; it is misleading for decision-making. Real markets cluster good and bad years. Real retirees raise spending with inflation, change cars, help family, and face health costs. A smooth 7% line never ran out of money in a spreadsheet; real sequences have repeatedly stressed retirement plans that looked “fine” under averages.

| Approach | What it captures | Sequence risk |

|---|---|---|

| Fixed average return each year | Long-run mean return | Ignored |

| Historical backtesting (real year-by-year returns) | Actual crash and recovery order | Visible |

| Monte Carlo (many random paths) | Distribution of outcomes, if the model matches how returns cluster in reality | Plain independent draws often mis-state clustering; regime or autocorrelation-aware models differ |

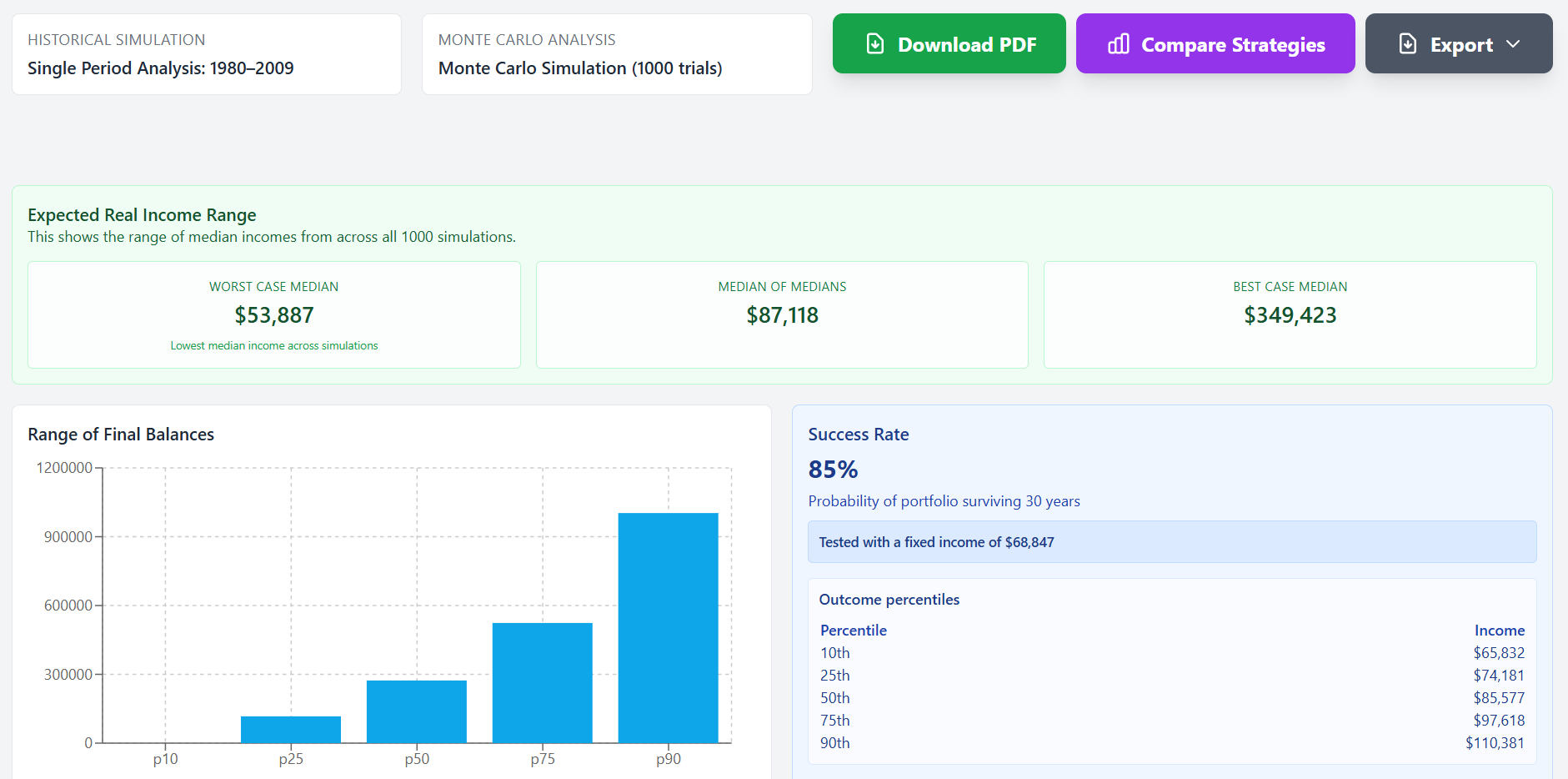

Monte Carlo and sequence risk: Saying Monte Carlo “partially” captures sequence risk was too vague. Many tools use independent random draws year to year (each year unrelated to the last). Real markets show autocorrelation (bad years bunch together) and clustering that IID models may not reproduce. That limitation is about model specification, not the word “Monte Carlo”: some simulations are too pessimistic, others miss fat-tail sequencing, depending on assumptions. Always ask how returns are generated.

What you can do in practice

No strategy eliminates market risk. You can still make sequence risk visible and manage trade-offs consciously:

- Stress-test with history. Prioritise Australian-relevant stress periods: high inflation and weak real returns in the 1970s, 1987, the early-2000s tech bust, and the GFC (when local and global markets fell sharply). If your plan only survives assuming post-2010 calm, you have learned something valuable. (Very long global datasets sometimes include episodes like the 1930s; treat those as methodological stress tests, not as literal forecasts of Australia today.)

- Build flexibility. Temporary spending cuts after large drawdowns, paid work for a few years, or drawing from cash buffers can reduce forced selling at the worst time.

- Review asset allocation through the risk zone. More growth assets can mean higher expected return and deeper drawdowns. There is no free lunch: only choices that match your capacity to bear losses while drawing down.

- Use dynamic withdrawal rules with eyes open. Fixed-dollar spending is simple; floor-and-ceiling or percentage-of-portfolio rules react to balance changes. Each approach has pros and cons.

For a deeper comparison of withdrawal strategies in an Australian context, see our article on super drawdown strategies. For a thought experiment on an extreme historical stress period (useful for how stress-testing works, not a prediction of Australian conditions), see what if you retired in 1929?

Monte Carlo and historical simulation: both useful

Monte Carlo simulation generates many possible futures by randomising returns; historical simulation replays what actually happened in order. Monte Carlo can show probability bands; history shows whether your spending would have survived real crash-and-recovery sequences. They answer related but not identical questions. As above, how the Monte Carlo engine draws returns (independent vs correlated, single regime vs multiple) changes what it says about sequence risk.

Our article on Monte Carlo versus reality explains why both appear in serious planning, why simple Monte Carlo can disagree with historical backtesting, and why neither replaces professional advice.

Tools that show only a success percentage without naming the worst historical period you would have survived leave you guessing. Tools that show worst-case sustainable income against real data give you a benchmark.

Stress-test your retirement against real Australian market history

The Advanced Calculator runs historical backtesting across decades of real returns and includes Monte Carlo analysis so you can compare approaches on your numbers.

Open Advanced Calculator (free tier available)Pick a scenario preset or enter your own age, balance, and spending. See how different retirement start dates change the story.

Bottom line

Sequence of returns risk is not an obscure academic idea. It is the reason two retirees with the same long-run average return can have very different outcomes depending on order, spending rate, and fund design. For Australians, the fix is neither panic nor complacency: it is testing your actual spending, asset mix, and pension entitlements against stressful historical periods, and recognising that who bears the most investment risk depends heavily on whether the Age Pension or super is doing the heavy lifting for your household.

Disclaimer: This content is educational. It does not consider your objectives, financial situation, or needs. Past performance is not indicative of future performance. Superannuation, tax, and Age Pension rules change; verify current rules with official sources and professional advisers.