Buying property through your SMSF is one of the most popular reasons people set up self-managed funds. The appeal is obvious: use your super to buy an investment property, receive rental income in a tax-advantaged environment, and potentially live in the property once you retire. Property spruikers and some financial promoters have built entire businesses around this concept.

But the reality of SMSF property investment is far more complex and costly than the marketing suggests. The rules are strict, the costs are higher than property held personally, and the liquidity constraints can create serious problems as you approach and enter retirement. Before you commit, you need to understand what you're really getting into.

The Fundamental Rules

Residential Property: Strictly Hands-Off

If your SMSF owns residential property, you cannot use it personally in any way. You cannot live in it, not even for a single night. You cannot holiday in it. You cannot rent it to yourself, your spouse, your children, or any other related party. This is the "sole purpose test" in action: the property must be held solely to provide retirement benefits, not current benefits to members.

This rule catches many people off guard. They imagine buying a beach house through their SMSF, renting it out for income, and then moving in when they retire. The first two parts work fine. The third part is illegal until you actually withdraw the property from the fund (which triggers CGT and other consequences) or the fund pays the property to you as a benefit in kind.

Commercial Property: The Business Owner's Advantage

Commercial property is different, and this is where SMSFs genuinely shine. Your SMSF can own commercial property and lease it to your own business, provided the lease is at market rent and on arm's length terms. This is called "business real property" and it's specifically exempted from the related party acquisition rules that prohibit most dealings between SMSFs and members.

For business owners, this creates a powerful strategy. Your business pays rent (tax-deductible) to your SMSF. The rental income in the SMSF is taxed at just 15%, or 0% if the fund is in pension phase. Over time, you're effectively transferring wealth from your business to your super in a tax-efficient way, while your super builds an asset that will fund your retirement.

Borrowing: Limited Recourse Only

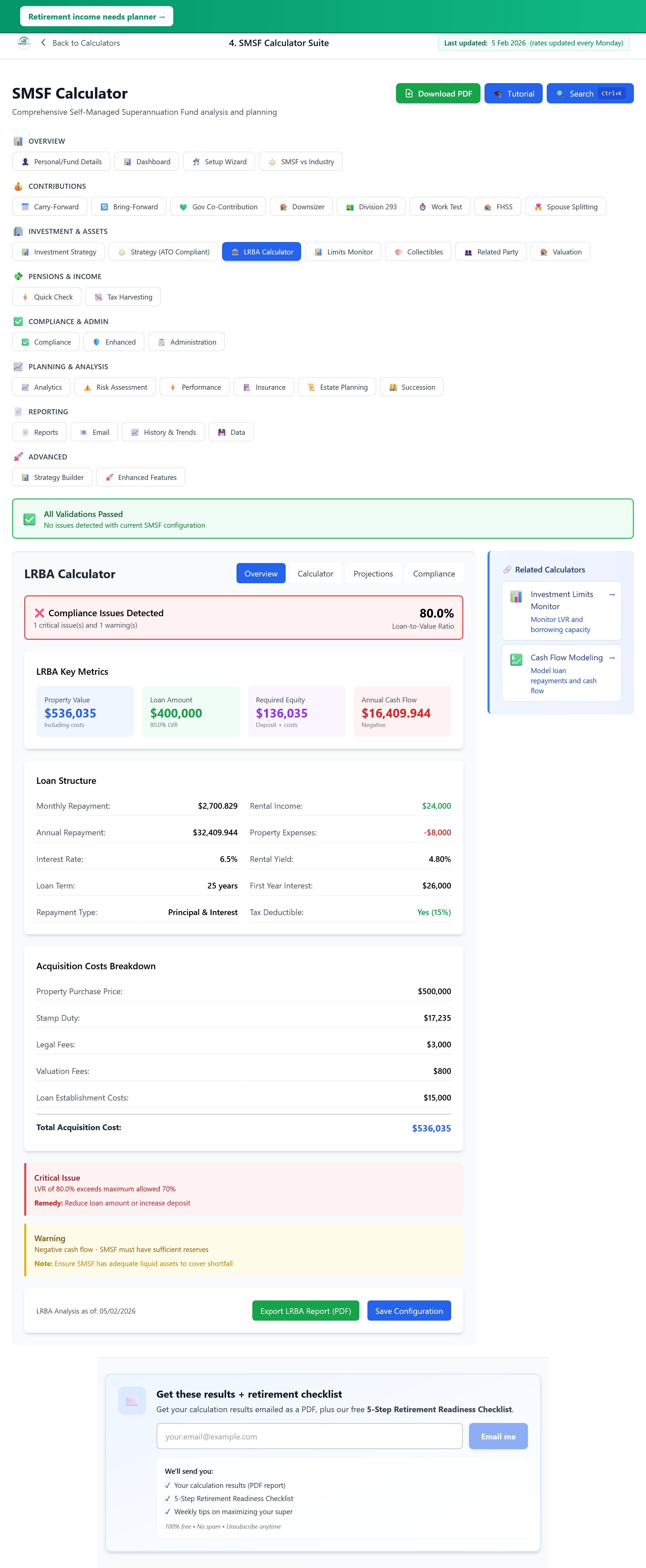

SMSFs can borrow to buy property, but only through a structure called a Limited Recourse Borrowing Arrangement (LRBA). The property must be held in a separate "holding trust" until the loan is fully repaid, at which point it transfers to the SMSF proper. The "limited recourse" part means the lender's security is limited to the property itself. They can't pursue other fund assets if the loan defaults.

LRBAs sound straightforward but come with significant restrictions. Most importantly, you cannot improve or renovate the property while it's held in the holding trust. Repairs are fine (fixing a broken hot water system or repainting); improvements are not. You can't add a bedroom, build a granny flat, or do a major renovation. Many people discover this restriction only after they've bought a property they intended to develop.

⚠️ The renovation trap: You cannot improve a property held under an LRBA. Only repairs are permitted. If you're planning to add value through renovation, SMSF property probably isn't for you. Many trustees have been caught out by this rule.

The Hidden Costs

Property in an SMSF costs more than property held personally, often significantly more. These additional costs eat into returns and can make the difference between a good investment and a marginal one.

Setting up an LRBA requires legal structures: the holding trust, the loan agreement, and various compliance documents. Expect to pay $2,000 to $5,000 for this setup, on top of your normal conveyancing costs. If anything goes wrong with the structure, rectifying it can cost even more.

SMSF loans carry higher interest rates than standard investment loans, typically 0.5% to 1% higher. On a $500,000 loan, that's $2,500 to $5,000 extra per year in interest. Lenders also require larger deposits. Most want 30% to 40% down, compared to 20% for a standard investment loan. This means you need more capital upfront and have less leverage.

Ongoing compliance costs increase when your SMSF holds property. You'll need annual property valuations for your financial statements. Your audit will cost more because the auditor needs to verify property-related compliance. If you have an LRBA, there's additional documentation to maintain and review.

Stamp duty offers no concessions for SMSFs. You pay the full rate, same as any investor. Land tax is often worse: in most states, SMSFs don't get the threshold exemptions that individual investors receive, meaning you pay land tax from the first dollar of land value.

The Liquidity Problem

Property is illiquid. You can't sell half a house. This creates problems for SMSFs that shares and other liquid assets don't.

Consider pension payments. Once you're in retirement phase, you must withdraw at least the minimum pension amount each year (4% to 14% of your balance depending on age). If 80% of your fund is tied up in a single property, where does the cash come from to make pension payments? You either need substantial liquid assets alongside the property, or you're forced to sell the property to fund your retirement, potentially at an inconvenient time.

Member exits create similar problems. If your SMSF has two members and one wants to leave (perhaps due to divorce, or simply wanting to roll to a different fund), can you pay them out? If most of the fund's value is in property, you may be forced to sell to satisfy the departing member's entitlement.

Death benefits can be complicated too. When a member dies, their benefits need to be paid to beneficiaries. If the fund's main asset is property, beneficiaries may have to wait months for the property to sell before receiving their inheritance. In some cases, disputes arise about whether to sell or how to value the property.

Concentration Risk

A $600,000 SMSF buying a $500,000 property has 83% of its assets in a single investment. Your investment strategy must justify this concentration, and you need to genuinely consider what happens if things go wrong.

What if property values in your area fall 20%? Your fund's balance drops dramatically, and if you're approaching retirement, you may not have time to recover. What if the property sits vacant for six months? You're still paying rates, insurance, and potentially loan repayments, but there's no rental income. Where does that money come from?

What if major repairs are needed (a new roof, restumping, fixing structural issues)? These costs can run to tens of thousands of dollars. In a diversified portfolio, you'd sell some shares to fund repairs. With a concentrated property holding, you may not have the liquid assets to cover unexpected costs.

When SMSF Property Actually Makes Sense

Despite all these cautions, there are situations where SMSF property investment genuinely works well.

Business real property is the clearest case. If you own a business that needs premises, buying those premises through your SMSF and leasing them back offers genuine advantages: tax-effective wealth transfer, asset protection, and eventual retirement income from an asset your business has been paying for all along.

Large fund balances change the equation. If your SMSF has $1.5 million or more, a $500,000 property represents only a third of the fund; still concentrated, but manageable. You have enough liquid assets alongside the property to handle pension payments, unexpected costs, and market fluctuations.

Long time horizons help too. If you're 45 with 20 years until retirement, you have time to ride out property cycles, pay down any LRBA, and accumulate liquid assets alongside the property. If you're 60 and planning to retire in five years, the risks are much higher.

Buying without borrowing avoids many complications. If you can purchase property outright (no LRBA), you eliminate the higher interest costs, the renovation restrictions, and the holding trust complexity. The property is simply an asset of the fund from day one.

When It Doesn't Make Sense

Small fund balances and SMSF property are a dangerous combination. If property will represent 70% or more of your fund, the concentration risk is too high. The fixed costs of the SMSF (audit, accounting, compliance) plus the property-specific costs may eat up most of your rental yield.

If you're close to retirement and need liquidity, property is problematic. You can't partially sell it to fund pension payments, and being forced to sell at a particular time removes your ability to wait for good market conditions.

If your main motivation is "I want to own property" rather than a clear financial case, pause and reconsider. Emotional attachment to property as an asset class doesn't make it a good SMSF investment. Run the numbers, including all the additional costs, and compare to alternatives like property ETFs or REITs that offer property exposure with liquidity.

The maths test: Would this property investment make sense outside super? If the answer is yes (if it's a good investment on its merits), the super tax advantages are a bonus. If the answer is no (if you're relying on tax benefits to make the numbers work), super's advantages probably won't save a marginal investment.

Does the property actually beat a diversified portfolio — with all costs included?

Higher interest rate, stamp duty, annual valuations, land tax with no threshold, audit costs. The SMSF Suite's Property vs Portfolio tool adds up all of these against your rental income and growth assumption, and shows you the real net return side-by-side against a diversified alternative. Run your numbers before you commit.

Compare Property vs Portfolio — Open the SMSF SuiteDisclaimer: This article is for general information only. It does not constitute financial product advice under the Corporations Act 2001 or legal advice. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). SMSF property investment is complex. Consult a licensed SMSF specialist, accountant, and solicitor before proceeding.