Many people compare SMSF costs and returns to industry funds and assume self-management wins. The marketing says "lower fees," "more control," "better returns." But the data on how SMSF trustees actually perform tells a more nuanced story. Research commissioned by the SMSF Association (University of Adelaide) concluded that SMSFs with balances above about $200,000 were more able to compete with larger funds on investment performance, which implies that below that level they generally face a tougher path. In practice many comparisons use a band of roughly $200k to $500k as the zone where industry funds often win on cost and value; the exact breakeven is not settled. Some analyses put cost breakeven closer to around $520,000, and the answer changes a lot depending on whether you compare to a typical balanced industry option or a low-cost indexed fund. For many trustees with balances under about $1 million, industry funds often deliver better outcomes when you add up costs, returns, and risks, but your mileage varies.

Behavioural finance research suggests self-directed investors sometimes underperform through timing, concentration, and trading; figures in the order of 1% to 2% per year appear in some studies of retail investors. Evidence specific to SMSF trustees is more mixed and less definitive than that broad literature, so treat any single number as illustrative, not a proven SMSF penalty. Below roughly $200k to $500k, SMSF costs as a share of assets are usually high and industry funds are typically cheaper; above that range, competitiveness depends on balance, provider, strategy, and advice. This is not a recommendation to open or close a fund. You can compare your own position in our SMSF Suite.

The Real Return Comparison

Historically, many large industry fund balanced or growth options have delivered mid- to high single-digit returns after fees over long periods. SMSF outcomes are more varied: very small SMSFs (for example under $200k) can show poor or negative returns and much higher effective cost ratios; ATO and researcher data show that for larger SMSFs (for example above about $200k to $500k), average returns are often competitive with APRA funds, though the distribution of outcomes is wide and behaviour and concentration still matter.

A sustained return gap of even about 1% to 2% per year compounds over time. On a $500,000 balance over 20 years, that kind of gap would mean a large difference in ending balance. We use that range as a stress illustration from behavioural finance, not as a guaranteed SMSF shortfall. Many trustees do not factor in how behaviour and concentration might affect outcomes when they choose self-management.

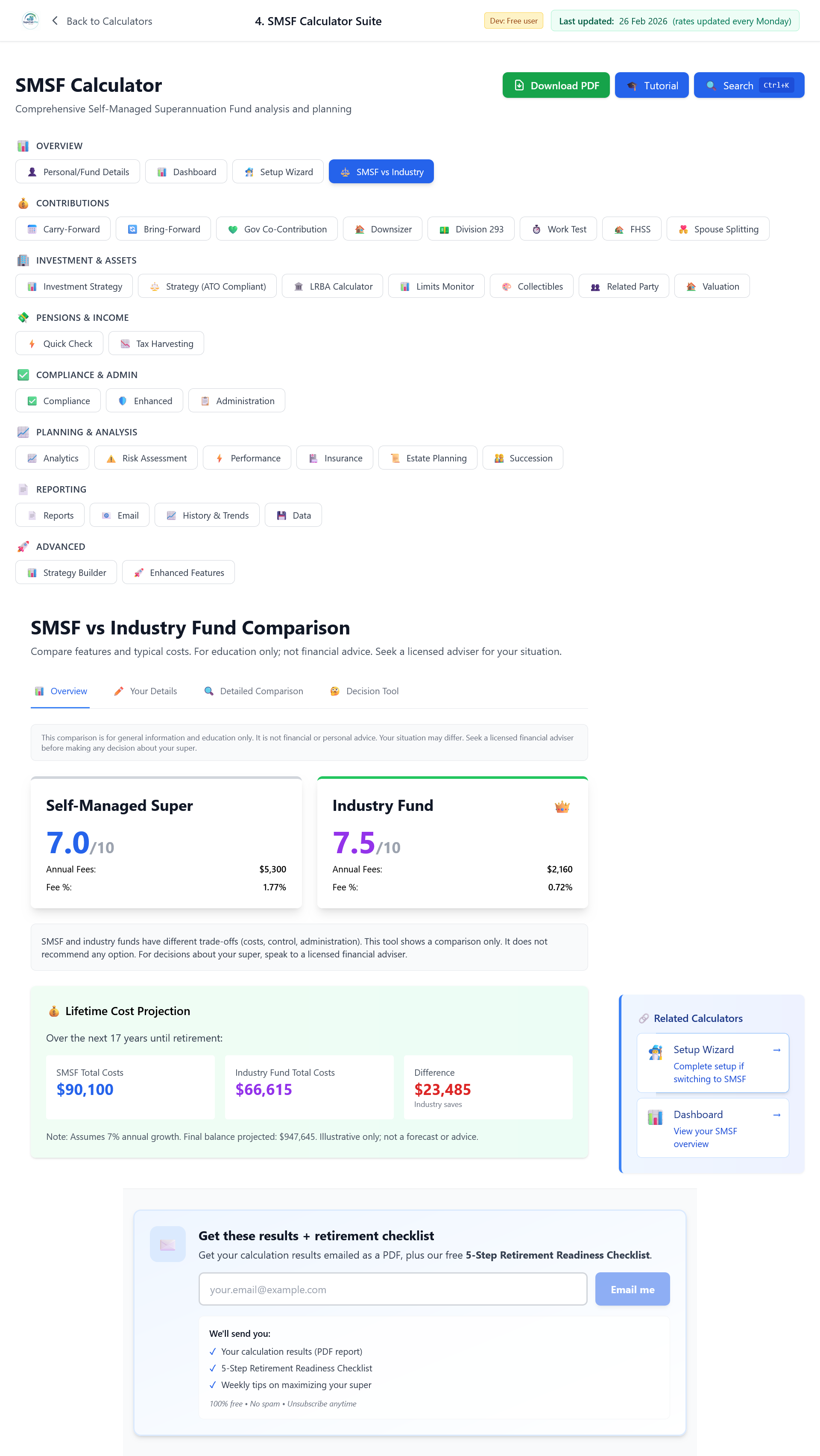

SMSF vs industry fund: cost and outcome comparison at a sample balance (from All Access SMSF Suite).

The Cost Comparison

Typical administration and audit costs for an SMSF often sit in the roughly $3,000 to $5,000 per year range, depending on provider and complexity. That figure is not the whole story. ATO statistics (for example, data around the March 2025 quarter) have put median administration and operating expenses near about $4,600, while median total SMSF expenses (including investment-related costs) have been reported around $9,300. Totals vary widely by fund; the point is that a casual reader should not anchor only on the lower admin-only band. Investment fees, advice, insurance, and other costs sit on top. We mention the $3k to $5k band here as an admin and compliance slice, not as full running costs.

Read the full cost picture: Compare admin or "running cost" estimates to total fund expenses in the ATO data and in your own statements. Underestimating total costs flatters the SMSF case.

Many mainstream industry fund balanced or growth options charge around 0.5% to 1% in fees; low-cost indexed options can be materially cheaper, which raises the bar for SMSF cost competitiveness if that is your benchmark. Below roughly $200k to $500k, SMSFs are usually more expensive as a share of assets; above that range, cost competitiveness depends on your provider, complexity, and how much external advice you pay for. Industry funds usually include insurance in their fees. SMSF members often need to arrange insurance separately; depending on age and level of cover, premiums can add thousands of dollars per year. Industry funds have professional investment teams; SMSF trustees either manage investments themselves (taking time and potentially making mistakes) or pay for advice (adding to costs). When you add all of that, industry funds are typically cheaper at lower balances, and competitiveness at higher balances depends on your situation and what you compare against.

The Diversification Advantage

Industry funds have professional teams managing diversified portfolios across many investments and sectors. SMSF trustees often hold concentrated portfolios; a significant share have most of their assets in a single investment, often property. That concentration creates risk. If that one investment or sector falls, the whole retirement plan can suffer. Industry funds are not exposed to the same single-asset risk because they are diversified.

The Expertise Advantage

Industry funds have access to research, management, and tools that most SMSF trustees do not. Behavioural finance work on self-directed investors sometimes cites gaps in the order of about 1% to 2% per year; the SMSF-specific evidence base is less clear-cut. Many trustees still overestimate their skill, which can lead to excessive trading, concentration, timing errors, and other mistakes that may reduce returns.

When SMSFs Make Sense

SMSFs can be cost-effective, but usually only under specific conditions. Some analyses suggest competitiveness can start from roughly $500k to $800k depending on provider, strategy, and how lean you run the fund. Using around $1.5 million as a threshold is a conservative rule of thumb where fixed costs are often a smaller share of assets; it is not the only view in the industry literature. You need genuine investment expertise and the time and interest to run the fund properly, and you need to avoid costly mistakes. For many trustees, those conditions are not met. ATO figures for recent years put average assets per SMSF around $1.63 million and, with typical two-member funds, roughly $880,000 per member on average; many funds are much smaller. Many trustees do not have specialist investment expertise or the time to manage the fund well. Mistakes are common. None of this is a recommendation to open, close, or change a fund; it is general information. For advice tailored to your situation, see a licensed financial adviser or SMSF specialist.

The Bottom Line

Below roughly $200k to $500k, SMSFs are usually more expensive and the evidence on cost drag is relatively clear; for many people in that range, industry funds deliver better value. In the mid-range, cost and performance can go either way depending on provider, behaviour, and whether you compare to a typical balanced option or a low-cost index fund. Some breakeven estimates sit nearer $520k than $200k. Above roughly $1 million, SMSFs can be cost-competitive or better for capable trustees, but the band from about $500k upward is debated. Do not let marketing alone drive the decision. Compare the full cost picture and the real numbers for your balance and situation, and seek advice from a licensed adviser before opening, closing, or changing any super fund.

Compare Your Running Costs

Use the SMSF Suite to see your running costs and how they compare at your balance. No recommendation to open or close a fund; just the numbers.

Open the SMSF SuiteWhat it costs to keep modelling

Try the SMSF Suite free first. Unlimited SMSF tools plus Advanced Retirement are All Access at $399 a year, or $39.99 a month if you’d rather not commit upfront.

Open the SMSF Suite →Free SMSF suite runs first, no card required. Subscribe only if the tools are useful enough to keep using.

Disclaimer: This article is general information only. It is not financial product advice or personal advice. SuperCalc Pro does not hold an Australian Financial Services Licence (AFSL). We do not recommend that you open, close, or change any super fund or product. ATO cost and balance statistics are updated over time; check current ATO publications before relying on any figure. The comparison of SMSF and industry fund costs and returns is educational. Your situation is unique; for advice tailored to you, consult a licensed financial adviser, SMSF specialist, or accountant.