Important Disclaimer: This article is for educational and informational purposes only. It does not constitute financial product advice, personal financial advice, or a recommendation. SuperCalc Pro is not licensed to provide financial advice under Australian law (we do not hold an Australian Financial Services Licence).

Past performance does not guarantee future results. The examples, scenarios, and comparisons provided are hypothetical and for illustration only. Market conditions, regulations, and economic factors change over time. What worked historically may not work in the future.

You should consult a licensed financial adviser (AFSL holder) for advice specific to your personal circumstances, objectives, financial situation, and needs. Always read the Product Disclosure Statement (PDS) and consider your own circumstances before making any financial decisions. Never make financial decisions based solely on information from this article or any calculator tool.

Your super fund's projection looks great. "You'll have $1.2 million at retirement!" it says. "You can spend $60,000 per year!" But here's what they don't tell you: that projection assumes everything goes perfectly. It uses average returns. It doesn't show you what happens if you retire into a crash.

Super fund projections are designed to be optimistic. They want you to feel confident about your future. But confidence without understanding the risks is dangerous. What if you retire in 2008? What if inflation spikes? What if markets crash in your first years of retirement?

Free calculators, including your super fund's, can't answer these questions. They use averages that hide worst-case scenarios. Historical data shows the truth.

How Super Fund Projections Work

Super funds use a simple formula:

The Super Fund Formula

Starting balance: $250,000

Contributions: $10,000/year (including employer contributions)

Return assumption: 7% per year (average)

Years to retirement: 20 years

Result: $1.2 million at retirement

This looks scientific. It's based on maths. But it assumes consistent returns of exactly 7% every year, which never happens. It assumes no crashes like 2008 in your first years of retirement. It assumes inflation stays at 2.5%, which isn't always true. And it assumes the order of returns doesn't matter, when in fact it does.

The problem is that real markets don't work like this. Some years you get 20% returns. Other years you lose 30%. The order matters, especially in retirement. A crash in your first year of retirement is devastating. The same crash in your tenth year is manageable. Super fund projections can't show you this because they smooth everything into an average.

What Super Fund Projections Hide

Your super fund's projection doesn't show you the things that actually matter. It doesn't show you sequence of returns risk, where two retirees with identical average returns can have wildly different outcomes based on when they retire. The order of returns matters enormously in retirement, a crash in your first year is devastating, while the same crash in your tenth year is manageable. Super fund projections can't show you this because they use averages and assume smooth 7% returns every year. Real markets are volatile, and the order of those returns matters enormously.

They also don't show you worst-case scenarios. Super fund projections show you the "average" outcome, but what about the worst case? What if you retire into a crash like 2008? What if inflation spikes like 1974? Historical data shows that worst-case scenarios are much worse than average projections suggest. A projection that says "$60K/year" might only support $45K/year in the worst historical periods.

Many super fund projections use nominal returns, which means they don't account for inflation. They might say "You'll have $1.2M" but not tell you that with 3% inflation, that $1.2M in 20 years buys what $700K buys today. Historical data shows real, inflation-adjusted outcomes. You see what you can actually buy, not just nominal dollar amounts.

Super fund projections assume you retire at the "average" time. But what if you're forced to retire early due to health, redundancy, or other factors? What if you retire into a crash? Historical data tests every possible retirement start year. You see worst-case, best-case, and average outcomes, not just a single optimistic projection.

Super fund says $70K/year. Real 1970s data says $45K. Test your retirement against 98 years of real market crashes, not smooth assumptions.

Stress-test with historical data →

The Gap: Super Fund vs Historical Data

| Factor |

Super Fund Projection |

Historical Backtesting |

| Returns |

Fixed return for the period (e.g., 7% every year) |

Real market sequences (volatile) |

| Worst-Case |

Not shown |

Shows actual worst periods |

| Sequence Risk |

Ignored |

Tested against real sequences |

| Inflation |

May use nominal returns |

Real (inflation-adjusted) outcomes |

| Retirement Timing |

Assumes average timing |

Tests every start year |

| Actionable Insight |

"You'll have $1.2M" (optimistic) |

"Worst case = $X/year" (realistic) |

The gap illustrates the difference between methods. Super fund projections use fixed returns and might suggest spending $68,869/year based on 7% fixed returns. But historical data shows that in the worst periods like 2008, the sustainable amount would be lower because actual market sequences include crashes and recoveries. This difference shows why understanding the methodology matters when interpreting results.

Real Example: The $300K Gap

Let's look at a hypothetical example. Consider someone aged 45, with $250K super, contributing $10K/year, and planning to retire at 65.

Super Fund Projection (Calculated)

Assumptions: 7% fixed return every year, 20 years

Starting balance: $250,000

Annual contributions: $10,000/year

Result: $1,377,376 at retirement

Sustainable income: $68,869/year (5% withdrawal rate)

Confidence: "Looks good!"

Historical Backtesting (Indicative Example)

Tests: Every retirement start year since 1929

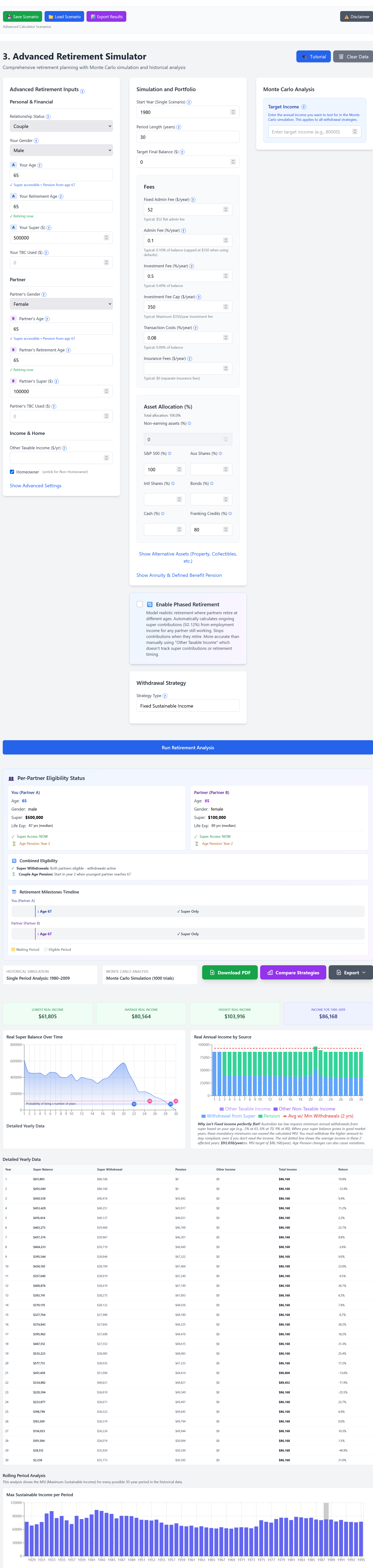

Method: The calculator runs the accumulation phase (age 45-65) with historical returns, then tests the retirement phase (age 65-95, 30 years) for each possible start year.

Results show: Worst-case, average, and best-case outcomes based on actual market sequences, not fixed returns.

Note: The figures shown are indicative examples to illustrate the concept. Actual results will vary based on your specific inputs, asset allocation, fees, and other factors. Use the calculator with your own details to get personalized results.

In this example, the super fund projection with 7% fixed returns suggests $68,869/year. Historical backtesting would show how this same plan performed in actual market conditions, including worst-case scenarios like retiring into crashes, which the super fund projection doesn't account for.

Historical backtesting shows worst-case, average, and best-case outcomes, not just a single projection

The key difference is that super fund projections use a fixed return assumption, while historical backtesting shows how the same plan would have performed in actual market conditions. If someone planned to spend $68,869/year based on the super fund projection, they might be fine in average years. But if they retired into a crash like 2008, historical backtesting would show the actual sustainable amount, which could be significantly lower. This gap illustrates why understanding both the fixed-return projection and historical worst-case scenarios matters when planning for retirement.

Run the stress test: You enter your balance, target income, and allocation; the app runs Historical Backtesting across every start year. You see the gap between "average return" projections and the worst-case that actually survived. Run the 60-Second Stress-Test to fix your projection with real data.

How to Stress-Test Your Plan

Understanding the limitations of super fund projections helps you better interpret the results you see. Historical backtesting can show your worst-case safe income, the amount that survived even the worst historical periods like 1929, 1973, or 2008. In a hypothetical example, if historical data shows a worst-case safe income of $45K/year, some people might choose to plan for $50K-55K/year instead. This provides a buffer if they retire into a crash, while knowing their absolute minimum. However, this is just one approach, different people may choose different strategies based on their circumstances.

Test different retirement ages too. What if you're forced to retire at 60 instead of 65? What if you want to retire at 55? Your super fund might say "$60K/year at 65," but historical data might show "$50K/year at 60", a $10K difference that could change your plans entirely.

Test different contribution levels. What if you can't contribute as much as planned? What if you lose your job? Your super fund assumes $10K/year contributions, but what if you can only contribute $5K/year? Historical data shows the impact on your final balance and retirement income, not just the optimistic scenario.

Test different return scenarios. What if returns are 1% lower than projected? What if they're 2% lower? Your super fund assumes 7% returns, but what if you only get 5%? Historical data shows periods with 5% average returns and how they affected retirement outcomes. You'll see how sensitive your plan is to changes, and if small changes cause big problems, your plan might be too aggressive.

Test inflation scenarios. What if inflation spikes to 5% or 10%? Historical data shows periods with high inflation like 1974 and how they affected purchasing power. Your super fund might say "$60K/year" in nominal terms, but with 5% inflation, that $60K in 20 years buys what $22K buys today. Historical data shows real, inflation-adjusted outcomes so you see what you can actually buy.

Worst-case $45K vs optimistic $70K? Test your retirement against every market crash, inflation spike, and sequence risk since 1928.

Run historical backtesting →

What Free Calculators Miss

Free retirement calculators, including super fund tools, have the same limitations. They use averages and assume smooth returns every year. They don't show historical worst periods. They ignore the order of returns, which means sequence risk is completely missing, a critical flaw that can destroy retirement plans. They may use nominal returns without inflation adjustment. And they can't test different scenarios, so you can't stress-test your plan.

The result is that free calculators give you optimistic projections that don't account for worst-case scenarios. They might indicate you're on track when historical data suggests different outcomes. A free calculator might suggest spending $60K/year based on 7% average returns, but historical data shows that in the worst periods like 2008, the sustainable amount might have been $45K/year. That $15K difference illustrates why understanding the methodology matters when interpreting results.

The Value of Historical Stress Testing

Historical backtesting is not academic window dressing. Comparing ordered market paths to a smooth average can change retirement timing, spending, or how much safety margin a household thinks it needs.

$15K+

Income gap you might discover

$300K

Balance gap (worst vs average)

100%

Historical survival (worst-case income)

How it works: Super fund projections use fixed returns and might tell you "You'll have $1.38M at retirement" (based on 7% fixed returns). But historical backtesting shows that in the worst historical periods, the actual balance at retirement could be lower because market returns vary year-to-year. This difference could mean retiring later, or having less per year to spend.

Or the reverse might happen. Super fund projections might suggest spending $60K/year based on averages. But historical data shows the worst case was $45K/year. Understanding both perspectives provides a more complete picture of potential outcomes.

Bottom line: Historical data shows what actually happened in past market conditions. Super fund projections use averages that hide worst-case scenarios. Understanding both perspectives helps you better interpret the results you see from retirement planning tools.

How to Fix Your Projection

Understanding how to interpret retirement projections can help you make more informed decisions. Historical backtesting tests your exact plan against every historical retirement start year. It shows your worst-case safe income, the amount that survived even the worst periods like 1929, 1973, or 2008. This represents a floor, the absolute minimum that historically survived.

Some people choose not to plan exactly at their worst-case floor, but instead plan 10-20% above it. This provides a buffer if they retire into a crash, while still knowing their absolute minimum. Testing different retirement ages, contribution levels, and return scenarios shows how sensitive a plan is to changes. If small changes cause big problems, the plan might be considered aggressive.

As people get closer to retirement, updating projections regularly can be helpful. Balances change, market conditions change, and needs change. Testing against historical data can help ensure plans remain on track. In a hypothetical example, if historical data shows a worst-case safe income of $45K/year, but someone wants to spend $55K/year, they might consider building a buffer through saving more, working longer, or being prepared to reduce spending if they retire into a crash. However, these are individual decisions that should be made with professional advice.

The Bottom Line

Super fund projections are designed to be optimistic. They use averages that hide worst-case scenarios. They don't show sequence risk, inflation impact, or retirement timing effects.

Historical backtesting provides a different perspective. It tests plans against every historical period. You see worst-case, best-case, and average outcomes. This helps you understand what actually happened in past market conditions, not just what looks good on paper.

Understanding the difference between super fund projections and historical backtesting helps you better interpret the results you see. Both have value, but they answer different questions. Historical data shows what actually happened. Super fund projections show what might happen if everything goes according to average assumptions. Neither guarantees future results, but understanding the methodology helps you make more informed decisions.

Don't Plan on Averages. Test Against Reality.

Run your retirement plan against 98 years of real market data. See your worst-case income, best-case income, and everything in between.

Run the 60-Second Stress-Test

Important Disclaimer: This article is for educational and informational purposes only. It does not constitute financial product advice, personal financial advice, or a recommendation. SuperCalc Pro is not licensed to provide financial advice under Australian law (we do not hold an Australian Financial Services Licence).

Past performance does not guarantee future results. The examples, scenarios, and comparisons provided are hypothetical and for illustration only. Market conditions, regulations, and economic factors change over time. What worked historically may not work in the future.

You should consult a licensed financial adviser (AFSL holder) for advice specific to your personal circumstances, objectives, financial situation, and needs. Always read the Product Disclosure Statement (PDS) and consider your own circumstances before making any financial decisions. Never make financial decisions based solely on information from this article or any calculator tool.

Data Sources: Historical market data 1928–2025, SuperCalc Pro calculator analysis. All calculations and projections are estimates only.

What it costs to keep modelling

Run Advanced Retirement free first. Unlimited scenarios, historical stress tests, and PDF exports are $149 a year, or $14.99 a month if you’d rather not commit upfront, typically less than one hour of paid advice for the same modelling work.

Run the Advanced Calculator →

No card required to try it. Subscribe only if the model is useful enough to keep using.