What is a downsizer contribution?

A downsizer contribution is a special super contribution available after selling an eligible Australian home. If you meet the rules, each member of a couple can contribute up to $300,000 from sale proceeds, without the normal work test or total super balance limit applying to the downsizer contribution itself.

The downsizer contribution is one of the most generous super strategies available. If you're 55 or older and sell your home, you can contribute up to $300,000 to super, regardless of your age, work status, or existing super balance. For a couple, that's $600,000 combined. See how it interacts with the Age Pension asset test and Transfer Balance Cap.

Eligibility Requirements

You must meet ALL of these:

- Aged 55 or older at time of contribution

- Owned the home for at least 10 years

- Home was your main residence at some point

- Home is in Australia

- Contribution made within 90 days of settlement

- Never made a downsizer contribution before (one-time only)

What Makes It Special

The downsizer contribution bypasses almost all normal super restrictions:

| Normal Rules | Downsizer Rules |

|---|---|

| Normal non-concessional caps and balance limits apply | Separate $300K downsizer cap with no total super balance limit |

| $120K non-concessional cap | $300K per person |

| General transfer balance cap can block non-concessional contributions | No total super balance limit |

| Age 75 cut-off | No age limit |

Example: The Smiths Downsize

John (72) and Mary (70) sell their Sydney home for $1.5 million. They've lived there for 25 years. They buy a smaller apartment for $800,000, leaving $700,000.

Each can contribute $300,000 to super as a downsizer contribution. Total: $600,000 added to their retirement savings, despite being over 70 with no work test.

See the projection, not just the rule: Model your downsizer contribution and see the impact on Age Pension and retirement projections in one place. Open the Advanced Calculator

⚠️ Age Pension Warning: Downsizer contributions count toward the Age Pension assets test. See our detailed article: The Downsizer Contribution Trap, when it hurts more than it helps.

$300K downsizer boost to super = great. But Age Pension impact? Model your complete downsizer strategy with pension trade-offs. Calculate downsizer impact →

Process: How to Make the Contribution

- Complete the Downsizer contribution into super form (NAT 75073)

- Give the form to your super fund BEFORE or WITH the contribution

- Transfer funds within 90 days of settlement

- Your fund will report it to the ATO

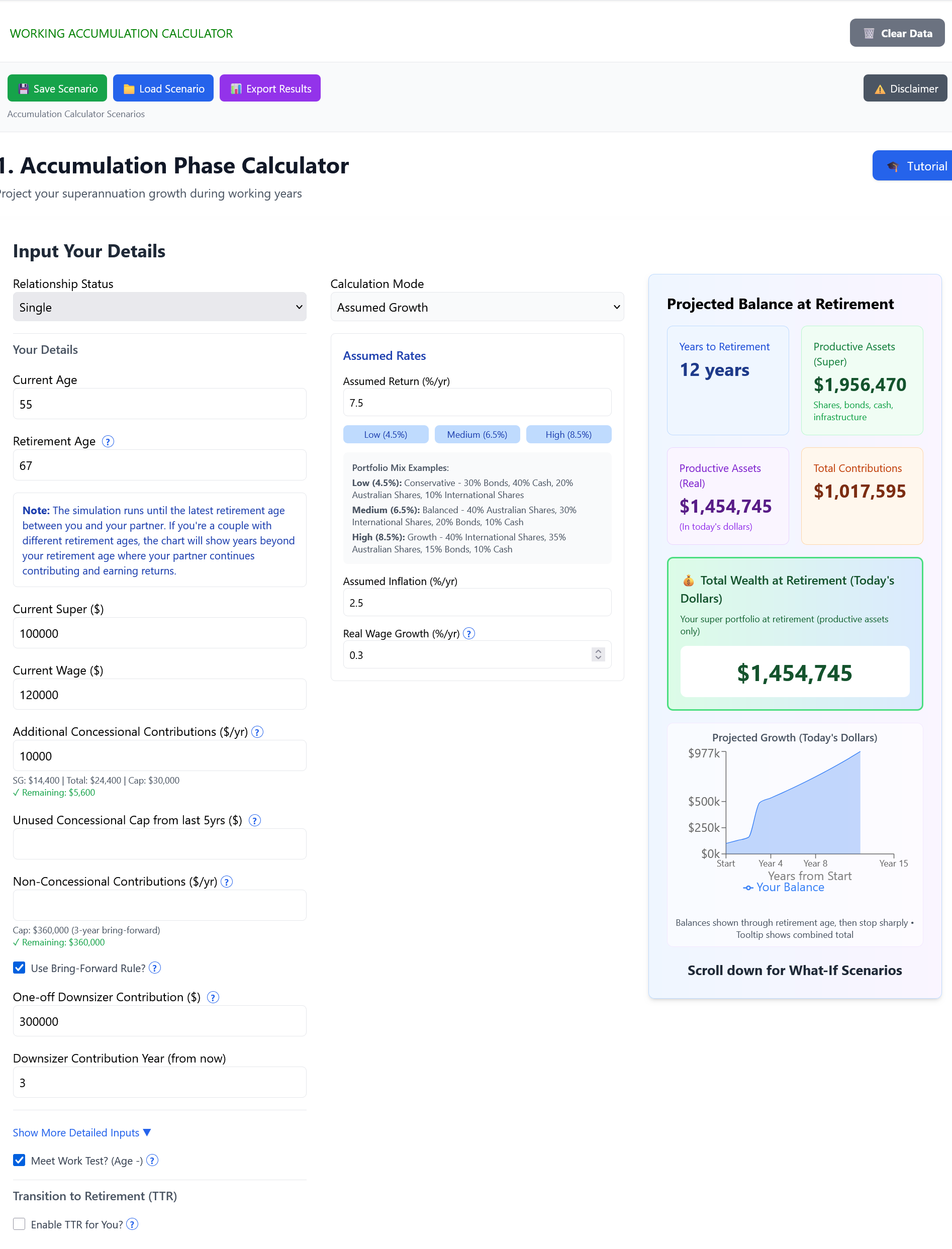

Accumulation calculator modeling a downsizer contribution

Strategic Considerations

- Transfer Balance Cap: Downsizer contributions don't count toward your TBC until you start a pension

- Tax-free vs taxable: The contribution is non-concessional, so withdrawals after 60 are tax-free

- Estate planning: Super death benefits have different tax treatment than personal assets

Common mistakes to avoid

- Missing the 90-day deadline, contributions must land in super within 90 days of settlement

- Forgetting the one-time rule, you can only ever make one downsizer election per person, lifetime

- Ignoring Age Pension impact, the full amount counts as an assessable asset immediately

- Not completing NAT 75073, without the form, the fund may treat it as a normal non-concessional contribution

Compare strategies with the downsizer contribution planner and the Advanced Australian retirement calculator before you exchange contracts.

Key tip: You don't have to actually "downsize." You can sell and rent, or even sell and buy something more expensive. The name is misleading; it is really a "home sale contribution."

Sell for $1.5M, buy for $800K = $600K available. But TBC, Age Pension, and estate planning all matter. Model your complete downsizer strategy. Calculate the full impact →

Model Your Downsizer Contribution Strategy

See the precise impact on your Age Pension, Transfer Balance Cap, retirement income, and estate planning. Calculate before you sell.

Calculate Downsizer StrategyRun your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator