The Age Pension asset test is one of the most misunderstood aspects of retirement planning in Australia. Every year, thousands of retirees either miss out on pension payments they're entitled to, or structure their finances poorly because they don't understand how the test actually works.

The rules aren't complicated once you understand them, but the details matter. The asset test works together with the Age Pension taper: as your assets rise above the lower threshold, your pension reduces by $3 per fortnight for every $1,000. A couple with $500,000 in assets might receive full pension, partial pension, or no pension at all, depending entirely on how those assets are structured and whether they own their home. For what counts (and what doesn't), see our guide to Age Pension exempt assets.

Get Your Free Retirement Readiness Checklist

A quick 15-point checklist to see if you're on track. Plus weekly tips on super, Age Pension, and retirement planning.

No spam. Unsubscribe anytime.

Where do your assets sit? The difference between $500K and $550K in assets can mean $4,000/year in pension. Know your exact entitlement before you retire. Calculate your Age Pension now →

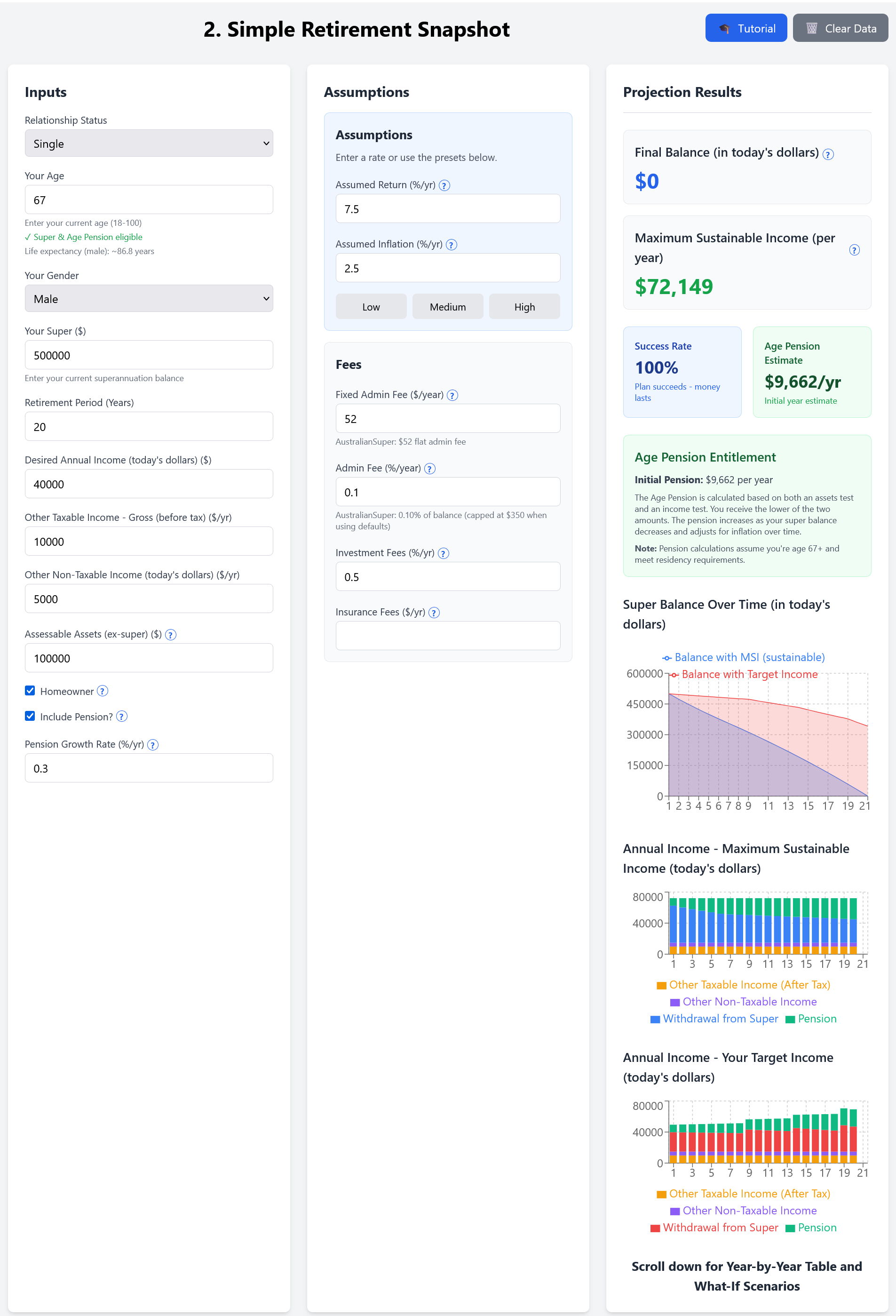

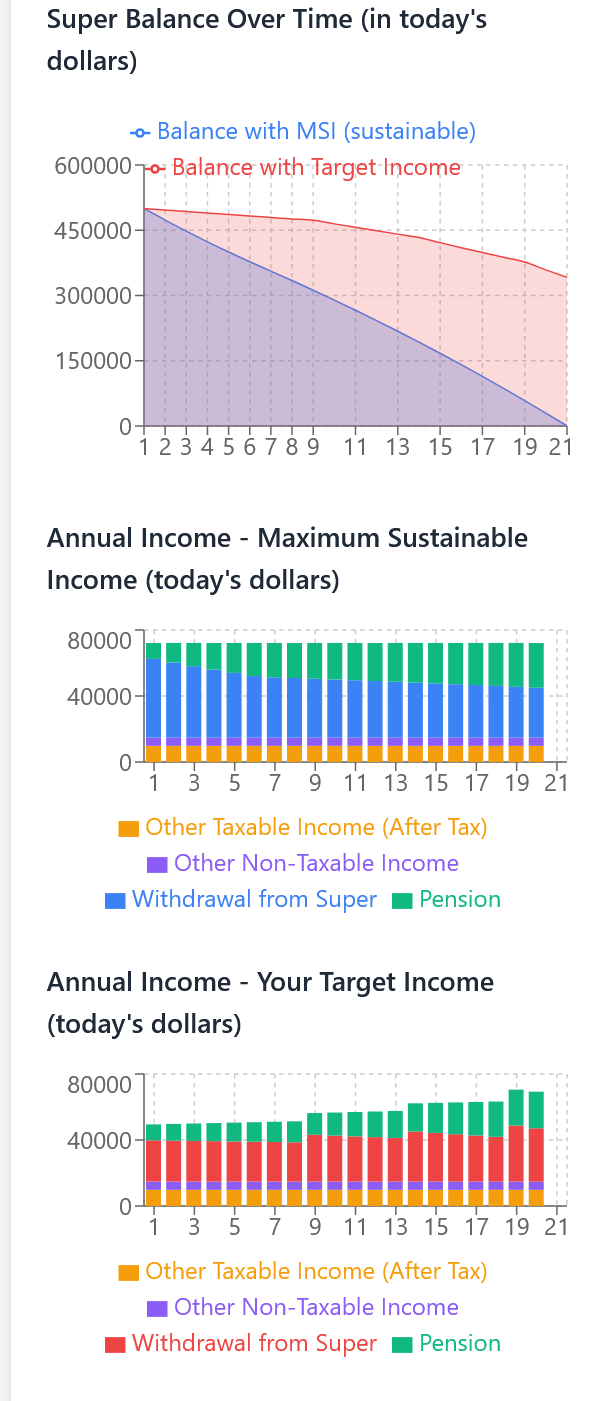

See the projection, not just the rule: Enter your assets and situation to see your Age Pension entitlement and year-by-year projections. Run the 60-Second Stress-Test. Open the Advanced Calculator →

How the Asset Test Actually Works

How Centrelink Calculates Your Age Pension: Step-by-Step

The first thing to understand is that there are actually two tests: the Assets Test and the Income Test. Centrelink calculates your pension under both tests and pays you the lower amount. Many people focus only on assets and forget that the income test might be what's actually reducing their payment. Learn more about how Age Pension combines with super in our retirement planning guide.

The asset test has two key thresholds. The "lower threshold" (sometimes called the "full pension limit") is the amount of assets you can have and still receive the full pension. The "upper threshold" (or "cut-off point") is where your pension stops entirely.

Between these two thresholds, your pension reduces by $3 per fortnight for every $1,000 in assets above the lower threshold. This is called the "taper rate" and it's crucial for understanding how much pension you'll actually receive.

Example: How the Taper Works

Sarah is a single homeowner with $400,000 in assessable assets. The lower threshold for single homeowners from 20 March 2026 is $321,500.

Reduction: $78,500 / $1,000 x $3 = $235.50/fortnight

Pension: $1,200.90 - $235.50 = $965.40/fortnight

Sarah receives a part pension of $965.40 per fortnight, not the full $1,200.90.

Age Pension Entitlement: Single Homeowner Example

March 2026 Asset Test Thresholds

These thresholds are updated in March, July, and September each year to account for changes in the cost of living. The figures below are current from 20 March 2026.

Homeowners

If you own your home (or are paying it off), these thresholds apply:

| Status | Full Pension Limit | Part Pension Cut-off |

|---|---|---|

| Single | $321,500 | $722,000 |

| Couple (combined) | $481,500 | $1,085,000 |

Non-Homeowners

If you don't own your home, the thresholds are higher to account for rental costs:

| Status | Full Pension Limit | Part Pension Cut-off |

|---|---|---|

| Single | $579,500 | $980,000 |

| Couple (combined) | $739,500 | $1,343,000 |

Asset Test Thresholds: All Scenarios Compared

Key insight: Non-homeowners get $263,000 extra for singles and $263,000 extra for couples to account for not owning a home. This significantly extends the range where you can receive Age Pension.

Key insight: The difference between homeowner and non-homeowner thresholds is $263,000. This means Centrelink effectively values home ownership at $263,000 when determining pension eligibility, something to consider if you're thinking about selling your home.

What Counts as an Asset?

Understanding what Centrelink counts, and does not count, as an asset is essential for planning. The rules aren't always intuitive.

Counted as Assets

- Superannuation (if over Age Pension age)

- Bank accounts and term deposits

- Shares and managed funds

- Investment properties

- Cars, boats, caravans

- Business assets

- Household contents (estimated value)

- Funeral bonds over $15,000

- Cryptocurrency

- Loans you've made to others

NOT Counted

- Your principal home (and up to 2 hectares)

- Funeral bonds up to $15,000

- Prepaid funeral expenses

- Life insurance policies

- Accommodation bonds in aged care

- Certain complying income streams

- Special disability trusts

- Native title rights

The Superannuation Trap

One of the most common mistakes people make is forgetting that superannuation counts as an asset once you reach Age Pension age. Before 67, your super isn't counted. The day you turn 67, it suddenly is, and this catches many people off guard.

If you're approaching 67 with significant super and were planning to apply for the pension, you need to factor this in. Your super balance on the day you apply will be assessed, regardless of whether you've started drawing from it. Understanding how much super you need for retirement helps you plan for this transition.

The Home Exemption: It's Complicated

Your principal home is exempt from the asset test, which is why many retirees choose to stay in their family home rather than downsize. But the rules around the home exemption have important nuances.

The exemption covers your home and up to two hectares of land on the same title. If you have more than two hectares, the excess is assessed as an asset. If your home is on a separate title from surrounding land, that land may be assessed.

Moving to aged care changes everything. If you move into residential aged care, your former home remains exempt for two years. After that, it's assessed as an asset unless your partner or a dependent child still lives there.

Granny flat arrangements have specific rules. If you transfer your home to family in exchange for a right to live there, Centrelink applies complex "granny flat reasonableness" tests. Get this wrong and you could be deemed to have made a gift, triggering deprivation rules.

Warning: The downsizer contribution lets you put up to $300,000 per person into super from the sale of your home. But remember: that super then becomes an assessable asset. Downsizing can actually reduce your pension entitlement if you're not careful. Consider the full implications before making this decision.

Asset Test vs Income Test: Understanding Both

Many people focus entirely on the asset test and forget about the income test. You need to pass both tests, and Centrelink pays you whichever amount is lower.

The income test uses "deeming" for financial assets. Regardless of what your investments actually earn, Centrelink assumes they earn a deemed rate of return. Currently, the first $64,200 (single) or $106,200 (couple) is deemed to earn 1.25%, and amounts above that are deemed to earn 3.25% (from 20 March 2026).

This means you can pass the asset test but fail the income test, or vice versa. A couple with $800,000 in term deposits earning 5% might pass the asset test but have their pension reduced under the income test because of the deemed income. Understanding how the taper rate works is crucial: every extra dollar saved above the threshold gives diminishing returns due to the $3 per fortnight reduction.

Legitimate Strategies to Maximise Your Pension

There are legal ways to structure your finances to maximise pension entitlements. But be careful: Centrelink has a five-year lookback period for gifts and asset transfers.

Home Renovations

Spending money on your home converts assessable assets (cash) into an exempt asset (your home). A $50,000 renovation reduces your assessable assets by $50,000 while improving your living situation. This is completely legitimate and commonly used.

Funeral Bonds

You can hold up to $15,000 per person in funeral bonds without them being counted as assets. For a couple, that's $30,000 in exempt assets. The bonds grow tax-free and can be used for funeral expenses.

Prepaying Expenses

Prepaying bills, rates, insurance, or other expenses reduces your assessable assets. Some retirees prepay a year's worth of expenses before their Centrelink assessment date.

Gifting (With Limits)

You can gift up to $10,000 per financial year, with a maximum of $30,000 over five years, without triggering deprivation rules. Gifts above these limits are still counted as assets for five years.

The Five-Year Rule: Centrelink looks back five years when assessing your assets. If you gave away $100,000 to your children three years ago, $70,000 of that ($100,000 minus the $30,000 allowance) is still counted as if you own it. Don't try to "hide" assets by giving them away shortly before applying for the pension.

Getting strategic? Home renovations, funeral bonds, prepaid expenses, gifting limits, every decision affects your pension. Model multiple scenarios to see which strategy maximizes your retirement income. Compare strategies in 2 minutes →

Common Mistakes to Avoid

Forgetting super counts after 67. Your super is invisible to Centrelink until Age Pension age, then it's suddenly a major factor. Plan for this transition, and consider your Transfer Balance Cap and super drawdown strategies well before you reach 67.

Undervaluing household contents. Centrelink expects a reasonable estimate of your household contents, typically $10,000-30,000 for most retirees. Claiming $2,000 for a house full of furniture will trigger questions.

Not updating when assets change. You're required to notify Centrelink within 14 days of significant changes to your assets. Inheriting money, selling property, or receiving a large gift all need to be reported.

Assuming the home is always exempt. The home exemption has conditions. Renting out part of your home, moving to aged care, or having land on separate titles can all affect the exemption.

Ignoring the income test. Even if you pass the asset test comfortably, the income test might reduce your pension. Always check both.

Model Your Situation

The best way to understand how the asset test affects you is to model your specific situation. Try different scenarios: What if you spent $50,000 on renovations? What if you gifted $10,000 to each grandchild? What happens when your term deposit matures and you reinvest it? Understanding the impact of these decisions before you make them is crucial.

Age Pension Asset Test 2025-26 Quick Reference Guide

Get all thresholds, formulas, and examples on one printable page. Perfect for your records or financial planning discussions.

Download Free PDF GuideThe Bottom Line

The Age Pension asset test isn't designed to be punitive; it is designed to target government support to those who need it most. Understanding the rules lets you structure your finances appropriately and claim the entitlements you're eligible for.

Key takeaways:

- Two tests apply (assets AND income): you get the lower payment

- Your home is exempt, but the rules have important conditions

- Super counts as an asset from age 67

- The taper rate is $3/fortnight per $1,000 over the threshold

- Centrelink looks back five years for gifts and transfers

- Legitimate strategies exist, but timing matters

Don't leave money on the table. If you're approaching retirement or already retired, understanding these rules could be worth thousands of dollars per year. Use our retirement calculator to model your specific situation and see exactly how different asset structures affect your pension entitlement.

Know Your Exact Entitlement

Asset thresholds, taper rates, homeowner status, deeming rules, they all interact in complex ways. Stop guessing. See your exact Age Pension entitlement and optimize your retirement strategy.

Run the 60-Second Stress-TestRun your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator