Important: This article is general educational information only. It is not personal advice, not financial product advice, and not a recommendation. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services License (AFSL). Rules and thresholds can change. If you need advice for your situation, speak to a licensed financial adviser.

The downsizer contribution lets you add up to $300,000 to super when you sell your home. It is a fantastic opportunity for many retirees. But there is a catch that is rarely discussed. Every dollar you contribute counts toward the Age Pension asset test.

The trade off explained

Your family home is exempt from the Age Pension asset test. Cash in your bank account is not. Super is not. When you sell your home and contribute the proceeds to super, you are converting an exempt asset into an assessable one.

The trap: If you are currently receiving Age Pension, a $300,000 downsizer contribution could reduce your pension by up to $23,400 per year. That is $450 per week. The taper rate is $3 per fortnight for every $1,000 of assets above the threshold, which equals $78 per year per $1,000.

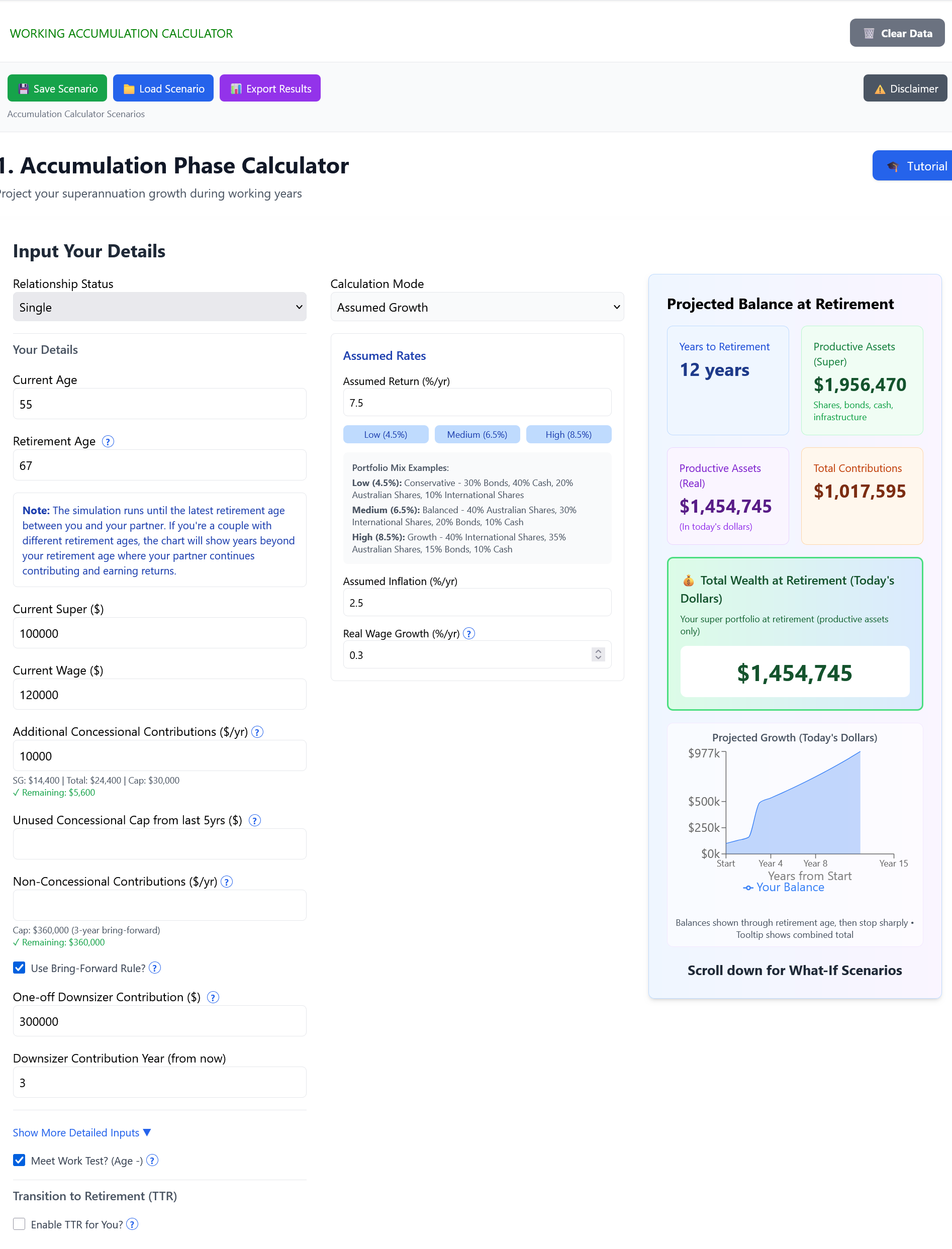

$300K downsizer = $23,400/year less pension? It depends on where you sit in the taper zone. Run the numbers before you sell. Model your exact scenario →

When downsizer contributions make sense

Downsizer contributions make the most sense in several specific scenarios.

If you are already above the pension cut-off and do not qualify for pension anyway, there is no trade-off. You can contribute the full $300,000 without any pension impact. The super boost is pure benefit.

If you are well below the threshold, a $300,000 contribution might still leave you eligible for full or part pension. You get the super boost without losing your entire pension entitlement. This is the sweet spot.

If you are relatively young, between 55 and 66, you have years before pension age. The super growth over that period may outweigh any future pension reduction. The compounding effect of having that money in super for a decade or more can be substantial.

If you have a younger spouse, the pension reduction may be temporary. Once your spouse also qualifies for pension, the combined household income may increase again. The temporary reduction can be worthwhile for the long term super boost.

When to think twice

There are situations where a downsizer contribution requires careful consideration.

If you are currently on full pension with modest assets, the contribution could push you into the taper zone or off pension entirely. That dramatically reduces your total income. The pension reduction might outweigh the benefits of having more in super, especially if you are already close to retirement age with limited time for super to grow.

If you are buying a cheaper home, it often makes more sense to keep more value in the new home. The home remains exempt from the assets test. Super does not. This is a critical distinction. Every dollar in your home is exempt. Every dollar in super counts toward the assets test.

If you are renting after the sale, you do get a higher assets threshold as a non-homeowner. But super is still assessable. You need to carefully calculate whether the contribution pushes you over the higher threshold and reduces your pension entitlement.

Example: The pension impact

Margaret is 70. She sells her home for $800,000 and buys a unit for $500,000. She has $200,000 in super and receives full Age Pension.

Option A: Keep $300,000 in bank. Assets equal $500,000. Pension reduced by approximately $15,500 per year.

Option B: Downsizer $300,000 to super. Assets equal $500,000. Same pension impact.

The downsizer contribution does not change her pension outcome in this case. But the super is more tax effective for investment returns. Earnings in pension phase are tax free. Earnings outside super are taxable.

The maths: when does super win

Super earnings are tax free in pension phase. Earnings outside super are taxable. This creates a mathematical equation that determines when a downsizer contribution makes sense despite the pension reduction.

For the downsizer contribution to win, the tax savings on investment returns must exceed the pension reduction you will face. This typically requires higher balances and longer time horizons. You need enough money in super generating enough returns that the tax savings on those returns outweigh the annual pension reduction.

For modest balances near pension age, the pension reduction often outweighs tax benefits. If you are 70 with $200,000 in super and you add $300,000, you will have $500,000 generating returns. But if that contribution reduces your pension by $20,000 per year, you would need to generate more than $20,000 in tax savings annually just to break even. That is unlikely with a $500,000 balance.

The maths only works in your favour if you have substantial balances, many years for growth, or you are already above the pension cut-off.

Should You Make a Downsizer Contribution? Decision Tree

- Already above cut-off

- Well below threshold

- Young (55-66)

- Large super balance

- Currently on full pension

- Near pension age (67+)

- Modest assets

- Buying cheaper home

Critical: Model both scenarios with exact numbers. A $300K contribution could reduce your pension by up to $23,400/year ($450/week). The pension reduction might outweigh tax benefits.

Model both scenarios to see the Age Pension impact

Key point: Model both scenarios. The right answer depends on your specific assets, age, and pension entitlement. There is no one-size-fits-all answer.

Downsizer or not? The answer depends on your exact assets, pension entitlement, and time horizon. See the precise dollar impact before you sell. Run your scenario now →

Alternatives to consider

Before committing to a downsizer contribution, consider several alternatives that might better serve your situation.

Renovating instead of downsizing allows you to keep your exempt home while improving it. You get the benefits of a better living situation without converting exempt assets into assessable ones.

Buying a more expensive home puts more value in the exempt asset category. This can be strategically valuable if you are concerned about pension eligibility.

Gifting to children is another option, though it is constrained by gifting limits. You can gift $10,000 per year or $30,000 over five years. This reduces your assessable assets while helping your family.

A partial contribution might be the sweet spot. Contributing less than the maximum $300,000 could give you some super boost while keeping you within pension eligibility thresholds. This allows you to test the waters and see how the contribution affects your pension before committing the full amount.

See the projection, not just the rule: Enter your assets with and without the downsizer contribution and the app shows you the pension impact in dollar terms, year by year. You see whether the tax-advantaged super growth outweighs the pension reduction, and at what asset level the trade-off flips. Open the Advanced Calculator →

Run your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator