The First Home Super Saver Scheme, usually shortened to FHSS, lets eligible first home buyers save part of a home deposit through super. It does not let you withdraw compulsory employer super. It lets you withdraw certain voluntary contributions, plus an amount of deemed earnings calculated by the ATO. Check the current super caps and FHSS limits before treating an old contribution figure as current.

The idea is simple: concessional contributions are usually taxed at 15% inside super rather than at your marginal tax rate. For many workers that creates a tax advantage while saving. The catch is that the money moves through the super system, so contribution caps, release rules, timing, and the lost retirement compounding all matter.

Contents

What the FHSS scheme actually does

FHSS does not turn your whole super balance into a house deposit. It is much narrower than that. You make voluntary contributions into super, later apply to the ATO for an FHSS determination, and if eligible you can release the allowed amount to help buy a first home.

The scheme can apply to voluntary concessional contributions, such as salary sacrifice or personal deductible contributions, and voluntary non-concessional contributions made from after-tax money. Compulsory employer Superannuation Guarantee contributions are not eligible. If your employer contributes 12% SG, that money stays in super and cannot be released under FHSS.

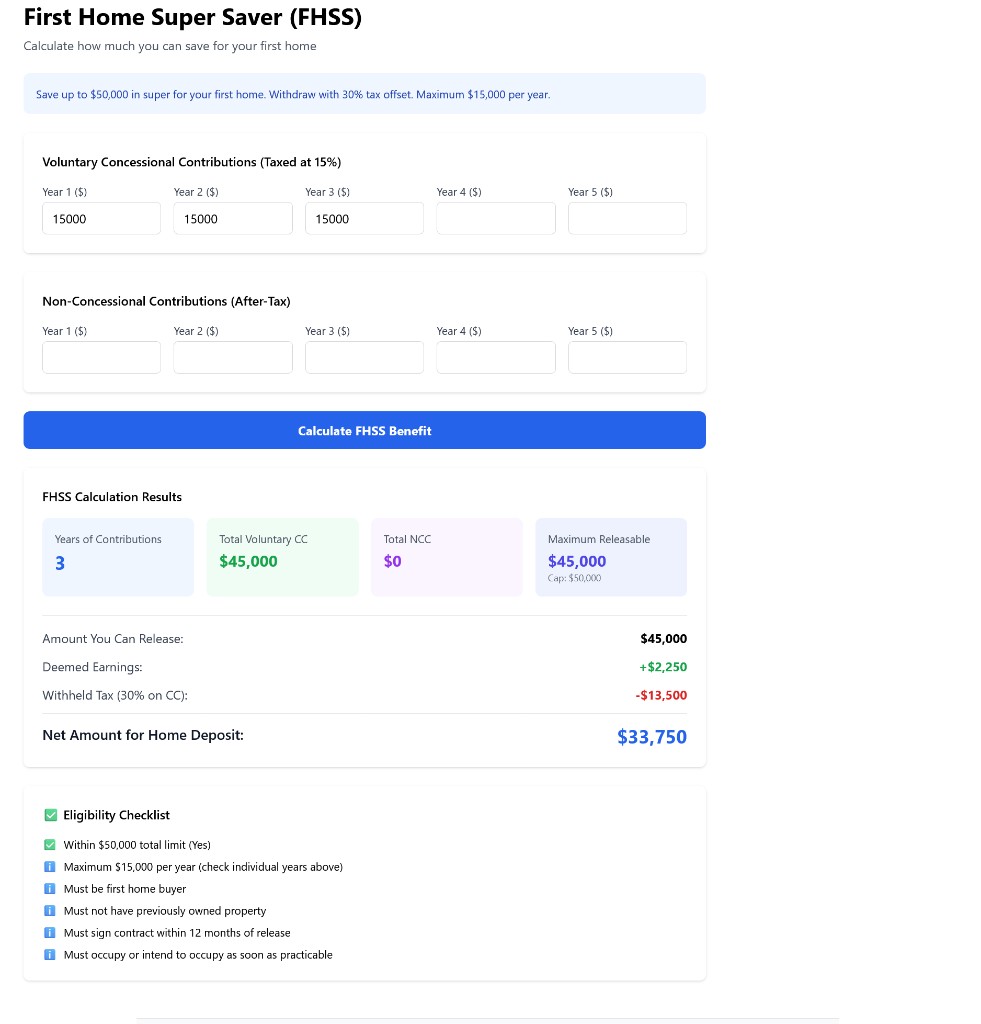

- Up to $15,000 of eligible voluntary contributions from any one financial year can count.

- Up to $50,000 of eligible voluntary contributions can count in total.

- Eligible concessional contributions are released at 85% of the contributed amount because 15% contributions tax has already been paid inside super.

- Eligible non-concessional contributions are released at 100% because they were made from after-tax money.

- The ATO also adds associated earnings, calculated using a deemed rate (generally based on the 90-day Bank Bill rate plus 3 percentage points), not your fund's actual investment return.

The contribution and release limits

The annual and total limits are easy to misread. The $15,000 annual limit is not a separate bonus and it is not a deduction cap. It is the maximum amount of eligible voluntary contributions from one financial year that can later be counted for FHSS. The $50,000 total limit is the maximum eligible contribution base across all years.

Those limits sit inside the ordinary super contribution caps. A salary sacrifice amount used for FHSS still counts toward the concessional contributions cap. For 2025-26 that cap is $30,000. If salary sacrifice, employer SG, and personal deductible contributions together exceed the cap, the excess contribution rules can apply. That is why FHSS planning has to be done alongside normal contribution cap tracking, not separately.

| Contribution type | Counts for FHSS? | Release treatment |

|---|---|---|

| Employer SG | No | Cannot be released under FHSS |

| Salary sacrifice | Yes, if voluntary and within limits | 85% of contribution plus associated earnings |

| Personal deductible contribution | Yes, if notice of intent process is completed | 85% of contribution plus associated earnings |

| Voluntary non-concessional contribution | Yes, if within limits | 100% of contribution plus associated earnings |

Who can use FHSS

In broad terms, FHSS is for people who have not previously held a relevant ownership interest in Australian real property. That test is broader than owner-occupied housing. It can include prior interests in investment property, vacant land, commercial property, leasehold interests in land, and company title interests in land. The ATO checks eligibility when you apply for a determination and again when you request release.

The property you buy with FHSS released amounts must be residential premises in Australia. Vacant land can qualify if you intend to build a home on it. You must genuinely intend to occupy the property for at least six months within the first 12 months after it is practical to move in. FHSS is not available to fund investment-only purchases.

Couples can each use FHSS if each person is eligible. That means two eligible buyers can potentially combine two separate FHSS releases toward the same home. Eligibility is tested individually. One partner may be eligible while the other is not.

You must be 18 years or older when requesting an FHSS determination. Contributions can be made earlier, but age is relevant at the determination stage.

How the release is taxed

Concessional contributions entered super before personal income tax was paid, so they are taxed when released. The assessable FHSS released amount is taxed at your marginal tax rate, less a 30% tax offset. Associated earnings are also assessable. Voluntary non-concessional contributions are not taxed again when released because they were made from after-tax money.

If the ATO does not know your expected marginal rate at release, withholding can default to 17%. The final tax position is reconciled through your tax return. This is one reason FHSS feels more complex than simply saving in a standard account. The headline benefit depends on your marginal tax rate, contribution mix, deemed earnings, and release timing.

Worked example: salary sacrifice through FHSS

Scenario: $15,000 salary sacrifice in one financial year

Assume a worker salary sacrifices $15,000 into super for FHSS purposes and is in the 30% marginal tax bracket, ignoring Medicare levy and other offsets for simplicity.

| Item | Amount |

|---|---|

| Salary sacrifice contribution | $15,000 |

| Contributions tax inside super at 15% | $2,250 |

| Net contribution available for FHSS release before earnings | $12,750 |

| Illustrative associated earnings added by ATO | $800 |

| Gross assessable release amount | $13,550 |

The released concessional component and associated earnings are assessable income, but receive a 30% tax offset. If the person's marginal rate is 30%, the tax offset can broadly cancel the marginal tax on the released amount. If their marginal rate is higher, there can still be net tax payable. If it is lower, withholding and tax return reconciliation matter.

The $2,250 deemed earnings figure in this example is illustrative only. Actual associated earnings vary with the ATO deemed-rate methodology in the relevant period and how long each eligible contribution remained in super before release.

The attraction is that the original $15,000 was not taxed at the person's full marginal rate when contributed. In this simplified example, keeping the money outside super and paying 30% tax would leave $10,500 for savings. Contributing through super leaves $12,750 before deemed earnings and release tax. The gap can help, but it is not free money. It is a tax timing and contribution-structure benefit within strict rules.

Model your FHSS release before relying on it

Use the FHSS calculator in the SMSF Suite to estimate the releasable amount, release tax, and the long-term retirement balance trade-off.

Open the FHSS calculatorThe hidden cost: lost compounding

The FHSS scheme is usually discussed as a deposit tool. It is also a retirement trade-off. Money released under FHSS leaves the super environment. If it would otherwise have remained invested for 30 or 40 years, the long-term compounding forgone can be meaningful.

That does not mean the scheme is bad. It means the comparison has to include both sides. A larger deposit may reduce lenders mortgage insurance, reduce interest paid, or bring home ownership forward. Against that, the super balance is lower and future earnings on the released amount no longer compound in the fund. The right comparison is not "FHSS versus doing nothing". It is FHSS versus saving outside super, after tax, with realistic timing and property costs.

For younger workers, the compounding cost is larger because the money has more decades to grow. For older first home buyers, the retirement cost may be smaller, but contribution cap and tax interactions can still matter.

Common traps

Confusing FHSS with a general super withdrawal

You cannot simply withdraw any part of your super balance because you are buying a first home. FHSS is limited to eligible voluntary contributions plus associated earnings. Ordinary preservation rules still apply to the rest of your super.

Forgetting employer SG counts toward the concessional cap

Employer SG is not eligible for FHSS release, but it still counts toward the concessional contributions cap. A worker on $150,000 receives $18,000 of SG at the 12% rate, leaving $12,000 of standard concessional cap space before any salary sacrifice or personal deductible contribution.

Assuming actual fund returns determine the release amount

The ATO calculates associated earnings using a deemed rate. If your fund performs very well, FHSS does not let you release all of that actual gain. If your fund performs poorly, the deemed earnings calculation can still add an amount to the release calculation.

Missing the timing sequence

FHSS involves an ATO determination and a separate release request. You can request determinations on more than one occasion, but release can generally be requested once. Do not assume funds appear instantly. Property transactions move quickly and settlement deadlines can be unforgiving.

Forgetting the post-contract notification requirement

After signing a contract to purchase or construct the property, you must notify the ATO within 90 days. Missing this step can create avoidable compliance issues.

Frequently asked questions

Can I use FHSS if I am buying with a partner who already owns property?

Possibly. FHSS eligibility is assessed individually. If you are eligible and your partner is not, you may still be able to use your own FHSS release toward the purchase. Your partner would not be able to use FHSS if they fail the first home buyer eligibility rules.

Can I use FHSS more than once?

You can request an FHSS determination more than once. The key limitation is on release requests, which are generally one-time. That distinction matters: a determination does not by itself force a release.

Does FHSS affect my non-concessional contribution cap?

Voluntary non-concessional contributions made for FHSS still count toward the non-concessional contribution cap. FHSS changes the release treatment, not the ordinary cap system.

What if I do not buy a home after release?

If you release money under FHSS and do not purchase within the required timeframe, you can generally either recontribute the amount to super or pay FHSS tax. The FHSS tax is generally 20% of the assessable FHSS released amounts. The ATO also provides an automatic 12-month extension window before these consequences are finalised. Check current ATO rules and dates before requesting release.