There's a seven-year hole in Australian retirement planning. Your super becomes accessible at preservation age 60 (for most people), but Age Pension doesn't start until 67. Those seven years? You're funding them entirely yourself. How you draw down in that gap — and whether you can stomach sequence risk — matters as much as the dollar amount.

Get Your Free Retirement Readiness Checklist

A quick 15-point checklist to see if you're on track. Plus weekly tips on super, Age Pension, and retirement planning.

No spam. Unsubscribe anytime.

At $70,000 per year (a comfortable but not extravagant retirement), those seven years cost $490,000. That's before the Age Pension kicks in to supplement your income. If you're spending $50,000 per year, it's still $350,000. Every year earlier you retire adds another year's expenses to that number.

Can you afford to retire at 60? $490K for 7 years sounds simple, but sequence risk, inflation, and market crashes change everything. Model your exact scenario before you quit. Stress-test your retirement plan →

The Maths Changes at 60

Preservation age is 60 for anyone born after 1 July 1964. Once you hit 60 and meet a "condition of release," super becomes accessible. The main condition is permanent retirement, defined as ceasing employment with no intention to work again (or working less than 10 hours per week). There's also Transition to Retirement (TTR) if you're still working, and unrestricted access at 65 regardless of employment status.

What's notable is the tax treatment. At 60, super withdrawals become completely tax-free. Not just the contributions you've made, but the earnings as well. Zero tax on money coming out. That's a significant advantage over working income or other investment earnings.

How Much Super at 60

The ASFA (Association of Superannuation Funds of Australia) publishes retirement spending benchmarks. Here's what different retirement lifestyles cost annually, and rough super balances at 60 that would fund them (assuming 5% real returns, living to 90, and part Age Pension from 67):

Single Person

| ASFA Standard | Annual Cost | Example Super at 60 |

|---|---|---|

| Modest | $32,000 | $450,000 |

| Comfortable | $52,000 | $750,000 |

| Higher spend | $80,000 | $1,200,000 |

Couple (Combined)

| ASFA Standard | Annual Cost | Example Super at 60 |

|---|---|---|

| Modest | $46,000 | $600,000 |

| Comfortable | $72,000 | $1,000,000 |

| Higher spend | $110,000 | $1,600,000 |

Note: These are illustrative examples based on ASFA standards and standard assumptions about investment returns and longevity. Your circumstances will differ.

ASFA says $750K for comfortable? Or $1.2M? Generic benchmarks miss YOUR situation. Run your own numbers with your spending, your super balance, your Age Pension entitlement. Calculate your personalized plan →

The Gap Years Problem: The expensive part isn't ages 67 to 90; it's ages 60 to 67. During those seven years, you have no Age Pension to offset withdrawals. If you're drawing $70,000 per year from super earning 5% ($35,000 in a $700,000 balance), you're withdrawing $35,000 more than you're earning. That accelerates depletion.

Once Age Pension starts at 67, even a part pension of $15,000 per year means you're only withdrawing $55,000 from super, not $70,000. That extends sustainability significantly.

Transition to Retirement Mechanics

Transition to Retirement (TTR) is a pension structure that allows super access while still employed. It's available from preservation age (60 for most). There's a minimum drawdown (4% of balance) and maximum (10% of balance). Earnings in a TTR pension are taxed at 15%, the same as accumulation phase.

The traditional TTR strategy involves salary sacrificing into super while simultaneously drawing from the TTR pension to replace lost take-home pay. The tax arbitrage comes from contributions being taxed at 15% instead of marginal rates (which can be 32.5%, 37%, or 45%). For someone on $120,000 salary sacrificing $30,000 and drawing $30,000 from TTR, the tax saving is around $8,000 per year.

TTR changes at 65. Once you hit 65, you get unrestricted access to super regardless of employment, and the pension becomes tax-free (0% tax on earnings instead of 15%).

Sequence of Returns Risk

This is the statistical problem that trips up early retirees. If markets crash in your first few years of retirement while you're withdrawing money, your portfolio can be permanently damaged even if markets recover later.

Example: Start with $1,000,000 at age 60, withdrawing $70,000 per year.

Scenario 1 (good sequence): First 5 years return +8%, +6%, +5%, +7%, +4%. Balance after 5 years: $964,000. You're in good shape.

Scenario 2 (bad sequence): First 5 years return -10%, -5%, +3%, +8%, +12%. Same average over longer periods, but you're selling assets in down years to fund withdrawals. Balance after 5 years: $811,000. You've lost $153,000 compared to Scenario 1, even though the arithmetic average returns are similar.

There's no way to eliminate this risk. Market timing doesn't work. What exists is portfolio structure (holding cash buffers so you're not forced to sell in downturns), spending flexibility (reducing withdrawals in bad years), and the option to return to work if things go badly.

The Legal Structure of Accessing Super

Conditions of release are legislated. The ATO defines them. At age 60, the main conditions are:

Permanent retirement: You've stopped working and don't intend to be employed again (or work less than 10 hours per week). This is a declaration you make; it's not ATO-verified unless audited. If you later decide to return to work more than 10 hours per week, you can't contribute more to that super account (though you can start a new accumulation account).

Transition to Retirement: You're 60 or older and still employed. You can start a TTR pension and access between 4-10% of your balance annually while continuing to work and contribute.

Terminal medical condition, permanent incapacity, severe financial hardship: These exist but are rarely the path to planned early retirement.

At 65, the condition changes to "reaching age 65." Employment status becomes irrelevant. You have full access to super regardless of whether you're working.

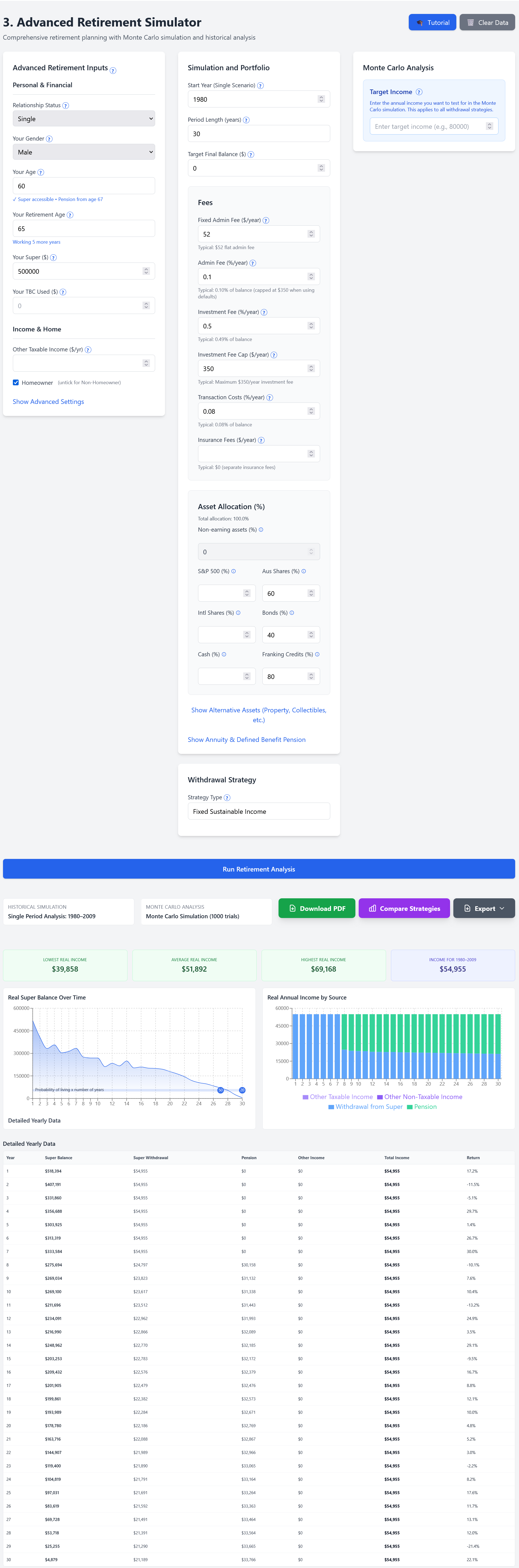

What the Calculator Shows

Calculator projection showing balance depletion over time with early retirement at 60

Running the numbers with real historical market data from 1928 to 2025, you can see how different retirement years would have played out. Starting in 1966 (bad sequence) vs 1982 (good sequence) produces wildly different outcomes even with identical starting balances and spending.

The calculator runs Monte Carlo simulations, testing your retirement plan against 1,000+ random market sequences. It shows probability of success, not guarantees. A 90% success rate means 100 out of 1,000 scenarios result in running out of money before age 90. Whether that's acceptable depends entirely on your risk tolerance and backup plans.

What Happens Timeline

At age 60, super becomes accessible if you meet a condition of release. Withdrawals are tax-free. This is when the seven-year self-funded period starts if you fully retire.

At age 65, you get unrestricted access to super regardless of employment. If you have a TTR pension, it converts to a standard account-based pension with 0% tax on earnings (instead of 15%).

At age 67, you become eligible for Age Pension if you meet the means tests (asset test and income test). Even a part pension significantly extends super longevity because it reduces annual withdrawals.

The downsizer contribution becomes available at 55 if you're selling a home you've owned for 10+ years. You can contribute up to $300,000 from sale proceeds into super (outside normal contribution caps). If you're retiring at 60 but selling your home at 62, this can provide a mid-retirement boost.

Ready to Retire at 60? Test It First.

Don't guess with $500K+ on the line. Model your exact scenario: your super balance, your spending, 7 years without Age Pension. Test against real market crashes from 1928-2025. See if your plan survives.

Stress-Test Your PlanDisclaimer: This article is educational information about superannuation rules and retirement planning concepts. It does not constitute financial advice and does not consider your personal circumstances. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services License (AFSL). Consult a licensed financial adviser for advice specific to your situation.