The ATO's compliance data makes sobering reading. Each year they identify thousands of SMSF breaches, and many trustees have no idea they have done anything wrong. The most common breaches are not deliberate fraud. They are honest mistakes made by people who do not fully understand their obligations.

But ignorance is not a defence. The penalties are severe: administrative penalties up to $18,780 per breach, the fund being made non-complying (taxed at 45% on all assets), or trustees being disqualified. These are not theoretical. They happen to real trustees every year.

The good news is that most breaches are avoidable if you know what the rules require and you have a way to check your fund against them. Below are the most common compliance failures, what the law says, and how the right tools can help you stay compliant.

1. Investment Strategy That Does Not Match Reality

Every SMSF must have a written investment strategy that genuinely reflects how your fund invests. A very common breach is having a generic template that says "balanced portfolio with 60% growth assets" when your fund actually holds 100% in a single property.

Your strategy must address five areas: risk and return, diversification, liquidity, ability to pay benefits, and insurance. If your strategy says you are diversified but you are not, that is a breach. If it says you have adequate liquidity but all your assets are in illiquid property, that is a breach. The strategy must be reviewed at least annually, and that review must be documented in trustee minutes.

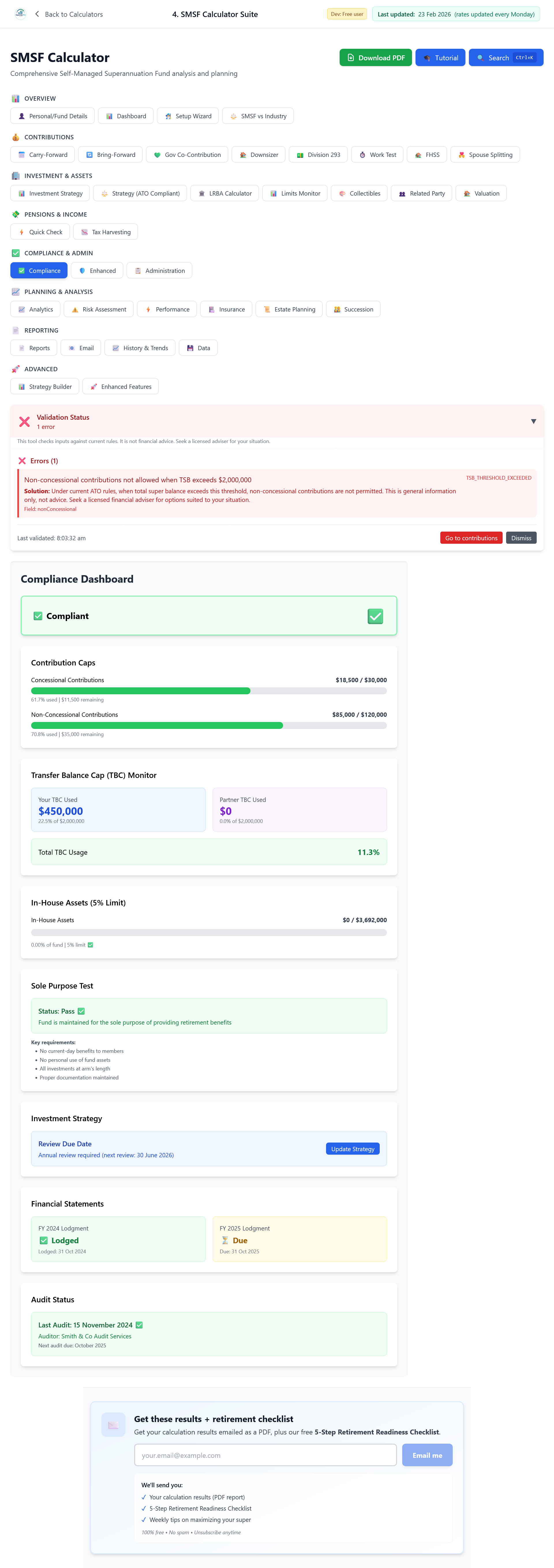

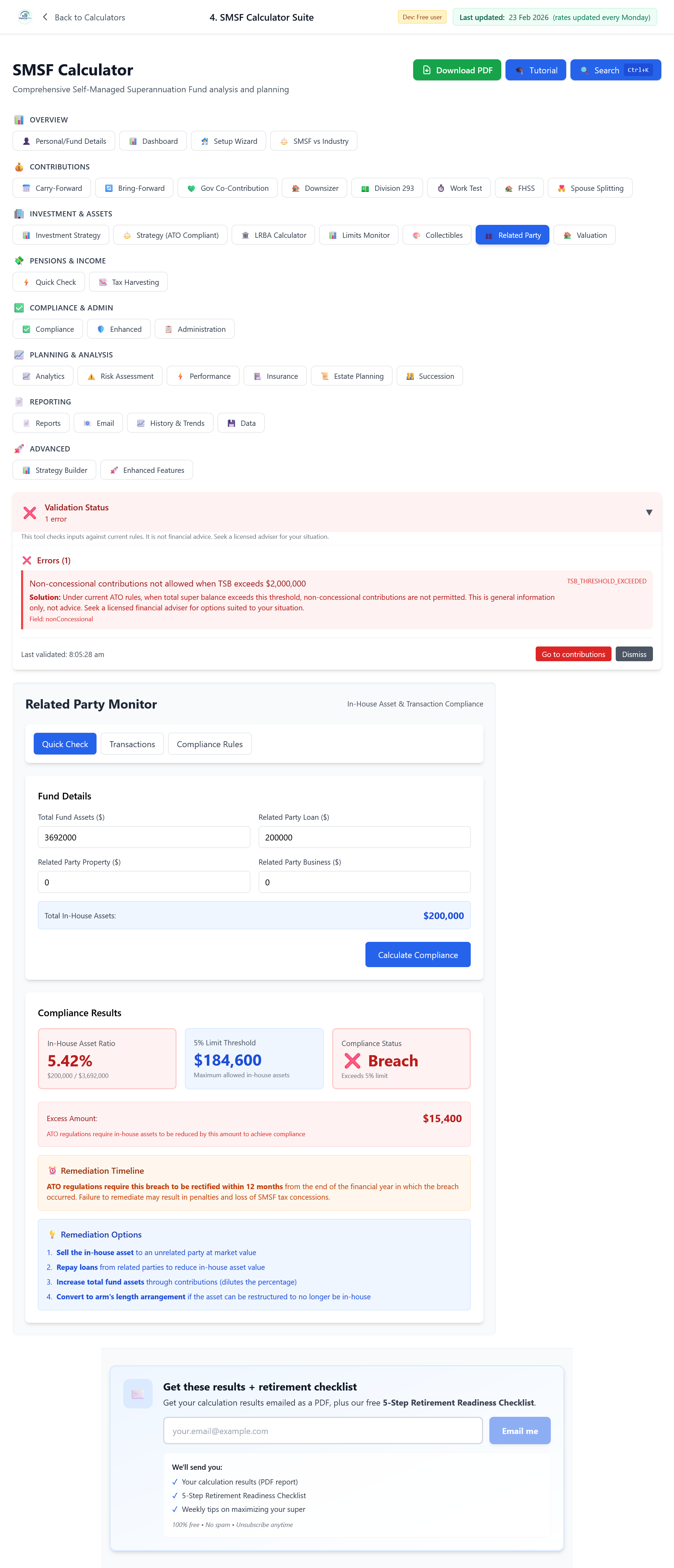

2. In-House Assets Exceeding 5%

In-house assets are investments in or loans to related parties. The law limits these to 5% of your fund's total assets. Many trustees breach this without realising it.

Common in-house assets include loans to family members, investments in companies controlled by members, and leases of fund assets to related parties (business real property leased to a member's business is excluded). If your fund has $500,000 in assets and you have lent $30,000 to your son, that is 6%. That is a breach. You must fix it and prepare a written plan to get in-house assets below 5%. The ATO expects that plan to be carried out as quickly as possible.

3. Sole Purpose Test Breaches

The sole purpose test says your SMSF must be maintained solely to provide retirement benefits. Any current benefit to members from fund assets is a breach. You cannot live in a residential property owned by your SMSF, even temporarily. You cannot display artwork owned by the fund in your home. You cannot use a fund-owned car, boat, or holiday house. You cannot lend money from the fund to yourself or family for personal use. The fund is a separate legal entity. Its assets must stay separate from personal use until you access them in retirement.

4. Missing or Inadequate Trustee Minutes

Trustee minutes are a legal requirement. They must document all significant decisions. Many funds have no minutes, or minutes that do not record decisions properly. Every significant decision should be minuted: accepting contributions, making investments, paying pensions, changing investment strategy, appointing or removing trustees. The minutes do not need to be long, but they must exist, be dated, and record who was present and what was decided. Auditors will ask for them. If you cannot produce minutes, that is a compliance issue in itself.

5. Contribution Cap Breaches

Exceeding contribution caps is one of the most common breaches, and it is often unintentional. Many people forget that employer super guarantee contributions count toward the concessional cap. If your employer contributes $12,000 and you salary sacrifice $20,000, you have exceeded the $30,000 cap by $2,000. Excess concessional contributions are included in your assessable income. Excess non-concessional contributions attract penalty tax of 47%. Both are expensive and avoidable with proper tracking.

6. Minimum Pension Payment Failures

If you are drawing a pension from your SMSF, you must withdraw at least the minimum amount each financial year. The minimum percentage depends on your age at 1 July, from 4% under 65 up to 14% at 95 and over. The deadline is strict: payments must be made by 30 June. There is no grace period. If you miss the minimum, the ATO can deem your pension to have ceased. All investment earnings for the year can become taxable at 15%, and you may need to restart the pension and use more Transfer Balance Cap space. This is one of the most common audit findings. It is avoidable with planning and reminders.

7. Separation of Assets Failures

SMSF assets must be clearly separate from personal assets. Bank accounts must be in the fund's name. Shares must be registered to the trustee on behalf of the fund. Property titles must show the trustee as owner. A very common breach is shares held in a personal name. People open a personal brokerage account, buy shares "for the SMSF," but never transfer them into the fund. Until shares are in the trustee's name, they are not fund assets. Any contributions used to buy them may be invalid.

8. Late or Non-Lodgement of Annual Returns

Your SMSF annual return must be lodged by the due date, typically by 28 February. Late lodgement attracts penalties and can trigger ATO scrutiny. The annual return is also how you report member contributions, pension payments, and other information to the ATO. Missing the deadline can cause problems with contribution cap tracking and other compliance matters.

⚠️ The consequences are serious: Breaches can result in the fund being made non-complying (taxed at 45% on all assets), administrative penalties up to $18,780 per breach, or disqualification as a trustee. Prevention is far better than cure.

How to Stay Compliant

Staying compliant means understanding your obligations and having a system to meet them. Review your investment strategy annually and document the review. Keep proper minutes of all trustee decisions. Track contributions so you do not exceed caps. Make minimum pension payments well before 30 June. Keep fund assets clearly separate. Lodge on time. If you are unsure about anything, seek advice from a licensed SMSF specialist or accountant.

Use the SMSF Suite to stay on top of compliance

The SMSF Suite gives you one place to check investment strategy, in-house assets, contribution caps, pension minimums, sole purpose, and ATO deadlines. You get the Compliance Dashboard, Related Party Monitor, Investment Strategy Builder, contribution and carry-forward tools, and deadline tracking. Run your fund with the right checks so you can spot issues before they become breaches.

Open the SMSF SuiteWhat it costs to keep modelling

Try the SMSF Suite free first. Unlimited SMSF tools plus Advanced Retirement are All Access at $399 a year, or $39.99 a month if you’d rather not commit upfront.

Open the SMSF Suite →Free SMSF suite runs first, no card required. Subscribe only if the tools are useful enough to keep using.

Disclaimer: This article is general information only and does not constitute financial, tax or legal advice. SuperCalc Pro Pty Ltd does not hold an AFSL. SMSF compliance is complex and rules change. Consult a licensed SMSF specialist or accountant for advice specific to your circumstances.