If you run a self-managed super fund, you've taken on responsibilities that retail fund members never see. The ATO regulates SMSFs closely, and the penalties for getting it wrong range from fines to your fund being declared non-complying—which can mean a 47% tax hit on the entire balance. Nobody wants that. So here's a straightforward checklist of what you're expected to do, and when.

This isn't legal or financial advice. It's an educational overview so you know what's on the radar. For your own fund, you need an SMSF specialist accountant and, where appropriate, a licensed financial adviser. Use this as a conversation starter with them, not a substitute.

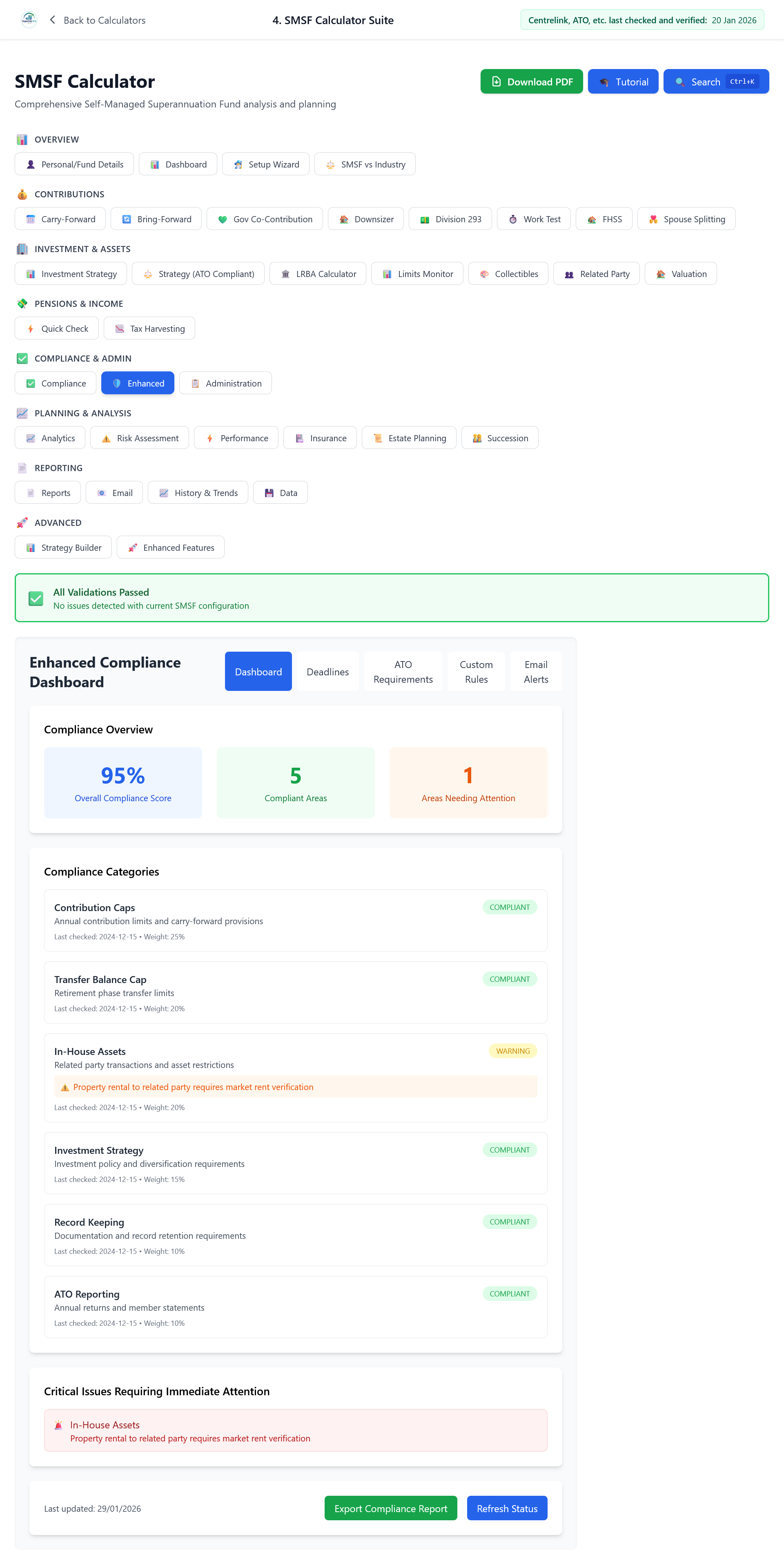

1. Investment Strategy

Every SMSF must have a written investment strategy. The ATO doesn't tell you what to invest in, but they do expect you to have thought about it and documented it. Your strategy should consider the risk, return, liquidity, and diversification appropriate for the members' circumstances and the fund's objectives.

You're also required to review the strategy regularly. "Set and forget" might work for a retail fund member; for trustees, it doesn't. If your personal situation or the market has changed, the strategy should reflect that. Many accountants recommend reviewing it at least annually and minuting the review.

Investment strategy checklist

- Written investment strategy in place

- Strategy considers risk, return, liquidity, diversification

- Strategy reviewed at least annually (and minuted)

- Investments are consistent with the strategy

2. Annual Return and Lodgement

Your SMSF must lodge an annual return with the ATO. For most funds the due date is 28 February (or the next business day), though you may get an extension if you're using a tax agent. Late lodgement can attract penalties. The return includes income, deductions, member contributions, and other information the ATO uses to check that the fund is operating within the rules.

Make sure all member contributions, pension payments, and rollovers are reported correctly. Errors here can trigger compliance action or delay the processing of member accounts.

3. Annual Audit

Every SMSF must be audited each year by an approved SMSF auditor. You can't skip this. The auditor checks that the fund has complied with super law and that the financial statements are accurate. If they find breaches, they're required to report them to the ATO. So getting your records and processes right before the auditor arrives isn't just good practice—it's how you avoid a compliance notice.

Choose an auditor who specialises in SMSFs. They'll know what the ATO is looking for and can often flag issues before they become problems.

Non-compliance is costly. If the ATO determines your fund has seriously breached the rules, they can make it "non-complying." That can mean the fund is taxed at 47% on the value of its assets. There's no grey area once that happens. Prevention is everything.

4. Arm's Length and Sole Purpose

All investments and dealings must be on arm's length terms. That means you can't lend money to yourself or your family on sweetheart terms, or buy assets from related parties at inflated prices. The fund must be run for the sole purpose of providing retirement benefits to members. Using the fund as a cheap loan facility or a way to get personal use of an asset is a fast track to compliance trouble.

Related-party transactions aren't automatically banned, but they have to be documented, commercial, and consistent with the sole purpose test. If in doubt, get advice before you do the transaction, not after the ATO asks about it.

5. In-House Asset Rules

In-house assets (broadly, investments in or loans to related parties or their entities) are restricted. Generally, the total value of in-house assets cannot exceed 5% of the fund's total assets. There are exceptions and nuances, but the 5% cap is the number most trustees need to keep in mind. Breaching it can lead to the fund having to dispose of assets and to penalties.

If your fund has any related-party investments or loans, your accountant or auditor will be checking this. Make sure you know the current value of those assets and the fund's total assets so you can confirm you're under the limit.

6. Borrowing and LRBAs

SMSFs can borrow in limited circumstances, typically through a limited recourse borrowing arrangement (LRBA). The rules are strict: the borrowing must be used to acquire a single asset (or collection of identical assets), and the lender's rights are limited to that asset. You can't use the rest of the fund as security.

If your fund has an LRBA, the terms must be commercial and documented. The ATO looks at whether the interest rate and other terms would be what unrelated parties would agree to. Again, this is an area where getting advice upfront is far cheaper than fixing a breach later.

7. Contributions and Caps

Trustees need to ensure that contributions accepted by the fund are within the law. Concessional and non-concessional caps apply to members. Accepting contributions that exceed a member's cap can create extra tax and administrative hassle. The fund is also responsible for reporting contributions correctly to the ATO.

If a member is 75 or older, concessional contributions can generally only be accepted if they're from an employer (and meet the work test or work test exemption where applicable). Getting contribution timing and reporting right is part of trustee duty.

8. Record-Keeping

The ATO expects SMSFs to keep proper records. That includes minutes of trustee meetings, investment strategy and reviews, copies of all annual returns, and financial statements. You must keep these for at least five years, and in some cases longer. If the ATO or your auditor asks for evidence that a decision was made properly, the only answer that holds up is a contemporaneous record.

| Obligation | Typical timing |

|---|---|

| Review and minute investment strategy | At least annually |

| Lodge SMSF annual return | By 28 Feb (or agent extension) |

| Complete annual audit | Before or with lodgement |

| Pay ASIC annual levy | When billed |

| Keep records | Minimum 5 years |

Bottom line: Running an SMSF gives you control, but control comes with a clear list of duties. Stay on top of the strategy, the return, the audit, and the rules around related parties and borrowing. When in doubt, talk to your SMSF accountant or auditor. One conversation can prevent a very expensive mistake.

Track Your SMSF in One Place

The SMSF calculator helps you model contributions, compliance, and retirement outcomes. See how your fund stacks up.

Open the SMSF SuiteRun your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator