Many SMSF trustees assume their will controls where their super goes when they die. It does not. Superannuation is held in trust by the fund. The trustees of the fund decide where your balance goes, in line with the fund's trust deed and any valid binding death benefit nomination you have made. If you have not made a valid nomination, or yours has expired or is invalid, the remaining trustees (often your spouse or adult children) have discretion. That can lead to outcomes you did not intend, extra tax, and family conflict.

Understanding how death benefits actually work is the first step. When you die, your SMSF balance becomes a death benefit that must be paid out. The trustees are bound by the deed and by any binding death benefit nomination that is still valid. Benefits can be paid to dependants (such as your spouse or children under 18), to your legal personal representative (the executor of your will, who then distributes according to your will), or to non-dependants such as adult children. Who receives the benefit affects how much tax is paid. Getting the nomination wrong can cost hundreds of thousands of dollars.

How SMSF Death Benefits Actually Work

When you die, your balance in the SMSF becomes a death benefit. The trustees must pay it out. They do not have a choice about whether to pay. They do have a choice about who receives it, but only within the limits set by the trust deed and by law. If you have left a valid binding death benefit nomination, the trustees must follow it. If you have not, they decide. In practice that often means your surviving spouse or adult children, as fellow trustees, decide. That can match your wishes. It can also create disagreement, delay, or a result you would not have chosen.

Death benefits can go to dependants (spouse, children under 18, or someone else financially dependent on you), to your legal personal representative so it is distributed under your will, or to non-dependants. The tax treatment depends on who receives the benefit and whether it is paid as a lump sum or pension. Many people assume that because they have named someone in their will, their super will go to that person. Super is outside the estate. The will does not direct it. Only a valid binding death benefit nomination, or the trustees' discretion if there is none, does.

The Tax Trap

Death benefits paid to dependants (spouse, children under 18) are generally tax-free. Death benefits paid to non-dependants are not. The taxable component of a lump sum paid to an adult child is taxed at 15% plus Medicare levy. On a large balance the number is big. For example, if your SMSF has a $1.5 million taxable component and you leave it to an adult child as a lump sum, the tax can be in the order of $225,000 or more. If you leave it to your spouse, the tax is typically nil. The difference is not a small rounding error. It is a structural result of who receives the benefit.

Many trustees do not realise this and nominate adult children directly. Others intend to leave everything to their spouse but never complete or renew a binding nomination, so the trustees later decide to split the benefit. The better approach for many people is to leave the benefit to their spouse (tax-free) or to their legal personal representative so that the executor can distribute according to the will, sometimes with better tax outcomes. That is a matter for individual advice. The point here is that the will alone does not fix it. You need a valid direction that the fund trustees must follow.

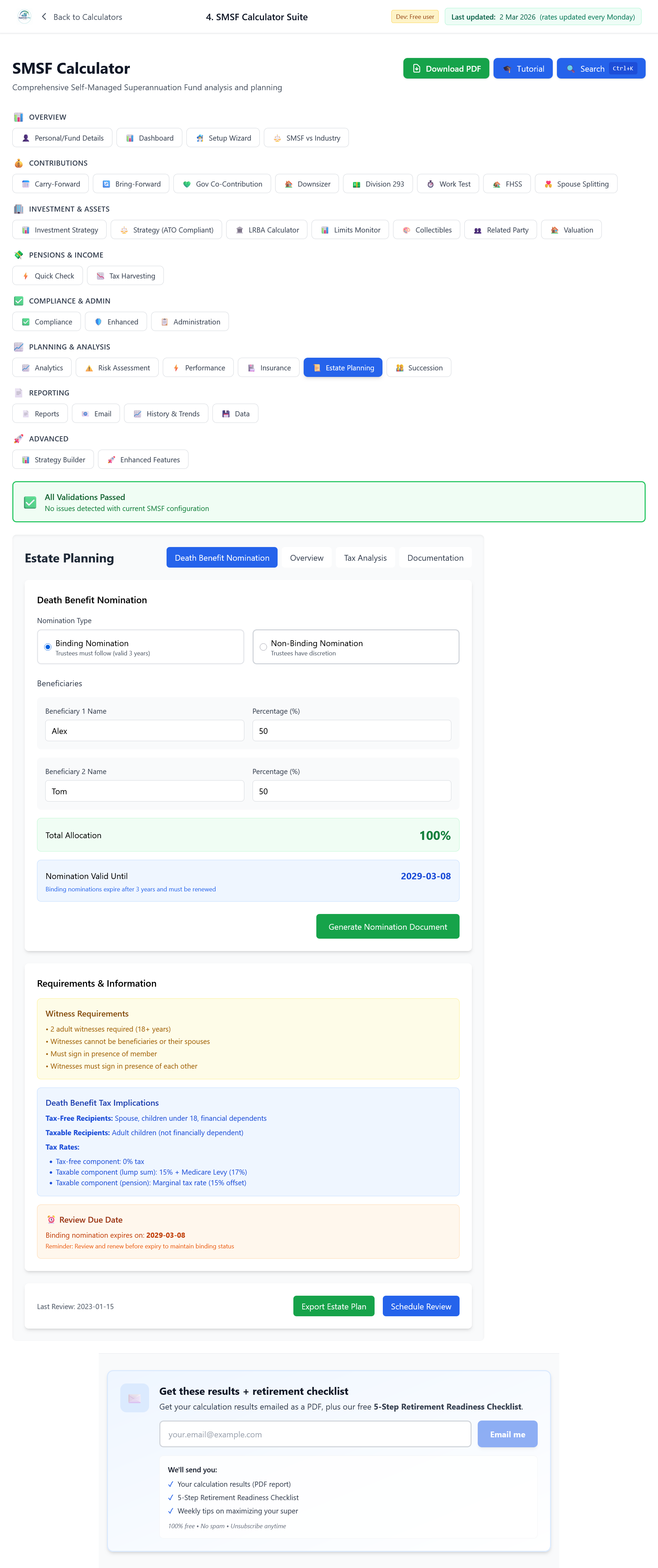

SMSF suite: Estate Planning panel with death benefit nominations and tax implications.

Binding Death Benefit Nominations: The Critical Document

A binding death benefit nomination (BDBN) is a written direction to the SMSF trustees about who should receive your death benefit. If it is valid and binding under the deed, the trustees must follow it. That removes discretion and reduces the risk of dispute or an outcome you did not want.

BDBNs have strict requirements. They must be in writing, signed and dated, and witnessed by two people who are not beneficiaries. They must comply with your fund's trust deed. Some deeds require renewal every three years. If the nomination is invalid or has lapsed, the trustees again have discretion. Invalid or lapsed nominations are common. People move house, change relationships, or forget to renew. When that happens, the document they thought would protect their wishes no longer does.

Common Mistakes

Trustees often assume their will controls super. It does not. Some have no binding death benefit nomination at all, so the trustees have full discretion. Others have a nomination that is out of date, incorrectly witnessed, or inconsistent with the deed, so it is not binding. Some leave super directly to adult children without considering the tax cost. Others never review their nomination, and it expires. Each of these can cost a lot of money or produce a result that does not match the member's intentions.

⚠️ The bottom line: Your will does not control your SMSF. You need a valid binding death benefit nomination that fits your deed, and you need to review it regularly. Do not assume that one document covers everything.

Review Your SMSF Estate Planning

Use the SMSF suite to see how death benefit nominations and beneficiary types affect tax, then get your BDBN and estate plan checked by a solicitor or licensed adviser.

Open the SMSF Suite2 free SMSF runs, no signup. See Pro pricing for full estate planning and compliance tools.

What it costs to keep modelling

Try the SMSF Suite free first. Unlimited SMSF tools plus Advanced Retirement are All Access at $399 a year, or $39.99 a month if you’d rather not commit upfront.

Open the SMSF Suite →Free SMSF suite runs first, no card required. Subscribe only if the tools are useful enough to keep using.

Disclaimer: This article contains general information only. It is not financial product advice, personal advice, or legal advice, and it is not a recommendation to acquire or hold any product or to set up or change any nomination. It does not take into account your objectives, financial situation, or needs. Before making any decision about SMSF estate planning, binding death benefit nominations, or your will, you should read the relevant fund documents and seek advice from a holder of an Australian Financial Services Licence (AFSL) or an authorised representative, and from a solicitor for legal and estate planning matters. SuperCalc Pro Pty Ltd does not hold an AFSL.