If you hold shares or other investments outside super and want to move them into your SMSF, you might assume you have to sell them first, contribute the cash, and then buy the same investments inside the fund. You can do it that way, but you don't have to. An in-specie transfer lets you move the assets directly, without turning them into cash in between.

The term "in-specie" just means "in kind." You're transferring the actual asset, not its cash equivalent. So instead of selling your 1,000 BHP shares, contributing $45,000, and buying 1,000 BHP in the SMSF's name, you transfer the shares themselves. The SMSF ends up holding the same shares you held personally, just under different ownership.

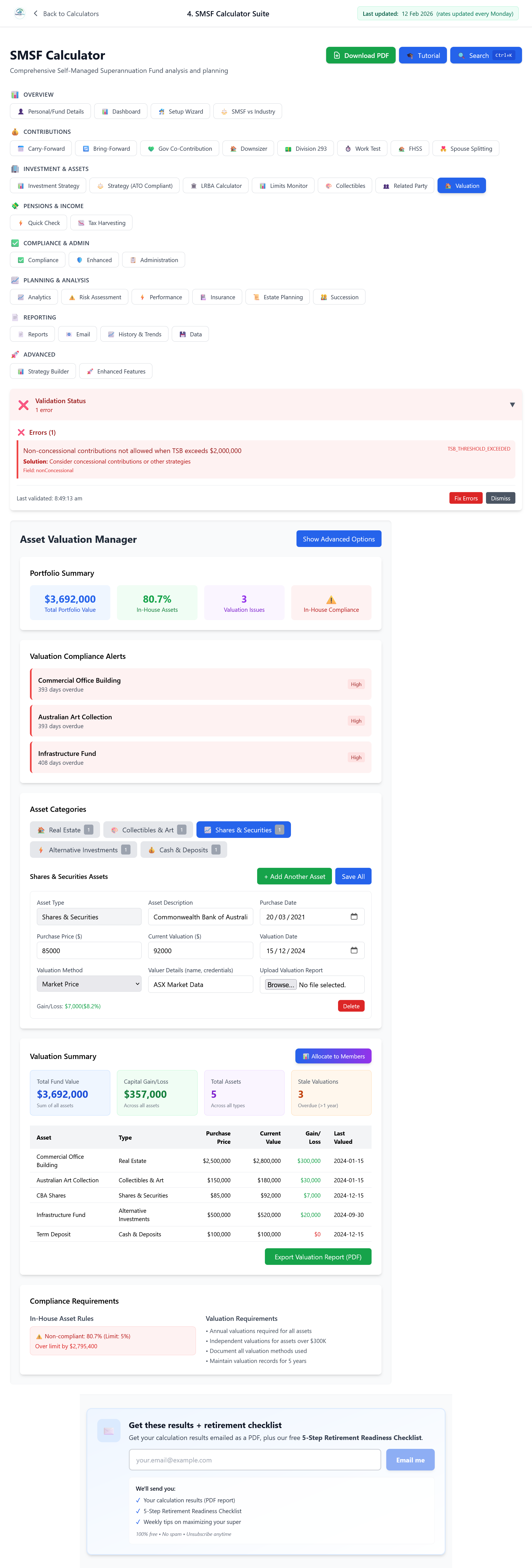

Plan and record in-specie transfers in one place. The SMSF calculator lets you enter each asset in Investment & Assets → Valuation, record each one (listed shares, property, alternatives) with purchase date, current value, valuation date and method (e.g. market price for ASX shares), so your fund’s books match what you’ve transferred. The Contributions section (Carry-Forward, Bring-Forward, caps) shows how much room you have before you transfer, so you don’t blow your non-concessional or concessional cap. The Limits Monitor and Compliance tabs flag when you’re near caps or when valuations are due. Use it to plan the transfer, record the contribution and value, and keep the fund compliant.

Open the SMSF SuiteWhat you can transfer in-specie

Not everything can be transferred into an SMSF from a related party. Super law limits what funds can acquire from members and their associates, and in-specie transfers have to fit those rules.

Listed securities are the most common. ASX-listed shares and ETFs can be transferred from your own name into your SMSF, subject to the usual contribution caps. Unlisted managed funds can sometimes be transferred too, if the fund manager allows it. Some do, some don't.

Business real property is a special case. Commercial property that's used wholly and exclusively in a business can be transferred to an SMSF even from a related party. That's one of the real advantages of SMSFs for business owners: you can transfer your business premises into your super fund and then lease them back.

Residential property is different. You can't acquire it from a related party. If you own an investment property personally, you can't just transfer it into your SMSF. You'd have to sell it on the open market to an unrelated buyer. The same goes for collectables and personal use assets. No shifting your art collection or classic car into super.

| Asset type | Can transfer? | Notes |

|---|---|---|

| Listed shares (ASX) | Yes | Most common in-specie transfer |

| Listed ETFs | Yes | Same rules as shares |

| Unlisted managed funds | Yes | If the fund manager permits it |

| Business real property | Yes | Commercial property used in the business |

| Residential property | No | Cannot acquire from a related party |

| Collectables or artwork | No | Cannot acquire from a related party |

How in-specie contributions work

When you transfer shares into your SMSF as a contribution, a few things happen at once. The transfer is valued at market value on the date of transfer. For listed shares, that's usually the closing price on the ASX that day. That market value drives both the contribution amount and the CGT outcome.

The market value counts against your contribution caps, the same as a cash contribution. If you transfer $50,000 worth of shares, that's a $50,000 contribution. It can be concessional (if you claim a tax deduction) or non-concessional (if you don't), but either way it uses your cap.

Here's the bit that catches people out. You trigger a capital gains tax event personally. For CGT, you're treated as having sold the shares at market value on the transfer date. If you bought them for $30,000 and they're now worth $50,000, you have a $20,000 capital gain. You might get the 50% CGT discount if you've held them for more than 12 months, but the CGT itself still applies.

⚠️ CGT still applies. In-specie transfers don't avoid capital gains tax. You're deemed to have sold at market value. What you gain is avoiding brokerage on both the sale and the repurchase, and the SMSF gets a fresh cost base at the transfer value.

The SMSF takes the shares at market value, and that becomes its new cost base. If those $50,000 shares later grow to $70,000 and the fund sells them, the fund's capital gain is $20,000, not the $40,000 gain from your original purchase. The CGT "clock" also resets, so the fund has to hold the shares for 12 months from the transfer date to qualify for any CGT discount.

A simple example

Say you own 1,000 CBA shares that you bought five years ago for $30,000. They're now worth $50,000 and you want to move them into your SMSF.

You transfer the shares in-specie as a non-concessional contribution. That triggers a $20,000 capital gain in your own name, which is halved to $10,000 under the CGT discount (assuming you've held them more than 12 months). At a 37% marginal rate, that's $3,700 in CGT.

The $50,000 transfer uses $50,000 of your non-concessional cap. The SMSF now owns the shares with a cost base of $50,000. If the shares grow to $70,000 and the fund sells them in pension phase, the $20,000 gain is tax-free. If it sells in accumulation phase, the gain is taxed at 10% (assuming the fund held them more than 12 months).

Compare that to selling personally, contributing cash, and rebuying. You'd pay the same $3,700 CGT, plus brokerage on the sale (say $50) and brokerage on the repurchase inside super (another $50). The in-specie transfer saves you $100 in brokerage. Not huge, but real. For bigger transfers, the savings scale up.

In-specie rollovers between funds

In-specie isn't only for contributions. You can also move assets between super funds without selling them. That's called an in-specie rollover, and it's handy when you're setting up an SMSF or consolidating super.

If you're rolling over from a retail or industry fund to your new SMSF, you might be able to transfer your existing investments directly instead of having the old fund sell everything and send cash. Not all funds offer it. Many only do cash rollovers. But it's worth asking.

The big plus with in-specie rollovers is that they don't trigger CGT. The cost base travels with the asset. So if your old fund bought shares for $30,000 and they're now worth $50,000, your SMSF inherits the $30,000 cost base. The unrealised gain stays deferred until the shares are eventually sold.

In-specie rollovers between SMSFs work the same way. If you're winding up one SMSF and rolling into another (for example when a couple merges two funds), assets can move directly without CGT events.

How you actually do it for listed shares

Transferring listed shares in-specie involves a few steps. First, the SMSF trustees need to pass a resolution accepting the in-specie contribution and recording the details: which member is contributing, which shares, and the market value.

You need a market valuation. For listed shares that's straightforward: the ASX closing price on the transfer date. Keep a record of it. A screenshot or printout showing the price on that date is enough.

The physical transfer happens via an off-market transfer form that you complete with your broker. That moves the shares from your personal HIN (Holder Identification Number) to the SMSF's HIN. Your broker and the SMSF's broker (if they're different) will process it. It usually takes a few business days.

Last step: record the contribution in the SMSF's books. Note whether it's concessional or non-concessional, the value, and the date. That flows into the fund's annual return and your own contribution cap tracking. The SMSF calculator's Valuation tab is set up for exactly this: you add the asset, enter the transfer value and date, and the calculator keeps it in your fund total and contribution history so you can see cap usage and stay on side of the ATO.

Business real property: the big one

Transferring business real property into an SMSF is one of the most powerful SMSF strategies, but it's also complex. If you own commercial property that your business uses, you can transfer it to your SMSF and then lease it back from the fund.

The benefits are real. Rent from your business to the SMSF is tax-deductible to the business. The rental income in the SMSF is taxed at 15% in accumulation or 0% in pension. The property sits in super, so it's not in your personal name for creditors. And when you eventually sell, any capital gain is taxed concessionally.

But the transfer itself attracts stamp duty (there's no exemption for super), and you need an independent valuation for market value. The property has to be used wholly and exclusively in a business. A mixed-use property with a residential part doesn't qualify. And the ongoing lease has to be at market rent, properly documented, with the SMSF acting as an arm's length landlord.

Worth knowing: In-specie transfers are especially useful when you've got large unrealised gains and you want to get money into super. You still pay the CGT (you can't dodge it by contributing), but you avoid double brokerage and get the assets into the tax-advantaged super environment. The main thing is to make sure you've got enough contribution cap space for the market value of what you're transferring.

What it costs to keep modelling

Try the SMSF Suite free first. Unlimited SMSF tools plus Advanced Retirement are All Access at $399 a year, or $39.99 a month if you’d rather not commit upfront.

Open the SMSF Suite →Free SMSF suite runs first, no card required. Subscribe only if the tools are useful enough to keep using.