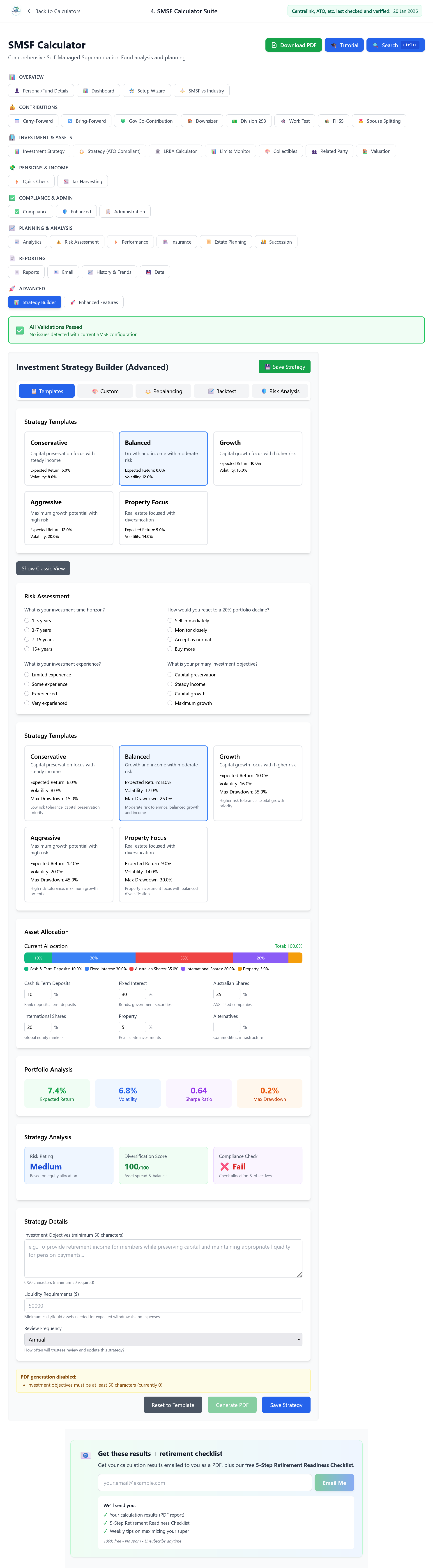

Every SMSF must have a written investment strategy that addresses five specific areas required by law. Many trustees use a generic template that says "balanced portfolio" or "growth assets," but those often do not meet the legal requirements. If your strategy does not address all five areas, it is not compliant, and that can amount to a breach that may result in penalties. For a full breakdown of what the law requires, see our article on SMSF investment strategy requirements. For a broader compliance checklist, see the SMSF compliance checklist.

The most common mistake is a "set and forget" strategy: a document written once, never reviewed, that does not match actual investments. If your strategy says "diversified portfolio" but you hold 100% in a single property, that is a breach. If your strategy says "adequate liquidity" but all your assets are illiquid property, that is a breach.

Your investment strategy must be reviewed at least annually, and that review must be documented in trustee minutes. Many trustees have a strategy but never review it, or they review it but do not document the review. Both are breaches that can result in penalties of 20 penalty units (currently $6,600 per trustee, at $330 per unit from 7 November 2024). Penalties apply per individual trustee, so they can multiply where there are multiple trustees.

The Five Legal Requirements

Section 52B of the SIS Act requires your investment strategy to address four specific areas. A fifth, consideration of insurance for members, is required by Reg 4.09 of the SIS Regulations. In practice your strategy must address all five:

1. Risk and Return Characteristics

Your strategy must consider the risk and return characteristics of your investments. You need to understand the risks you are taking and the returns you expect. A strategy that says "we invest in property for growth" is not enough. You need to explain why property is appropriate for your risk profile and return objectives.

2. Diversification

Your strategy must consider diversification. That does not mean you must be diversified. You can have a concentrated portfolio if you can justify it. But you must consider diversification and document why your level of diversification, or lack of it, is appropriate.

If you have 100% in a single property, your strategy must explain why this concentration is appropriate. "Property always goes up" is not a sufficient explanation. You need to show that you have considered the risks of concentration and made an informed decision.

The five areas the law requires: risk and return, diversification, liquidity, ability to pay benefits, and insurance.

3. Liquidity

Your strategy must consider liquidity, that is, your ability to convert assets to cash when needed. If you are drawing a pension, you need liquidity to make pension payments. If you are still accumulating, you need liquidity to pay benefits when members retire or leave the fund.

If all your assets are in illiquid property, your strategy must explain how you will meet liquidity needs. "We will sell the property if needed" is not enough. Property sales take months, and you need to make pension payments monthly. You need a plan for maintaining adequate liquidity.

4. Ability to Pay Benefits

Your strategy must consider your ability to pay benefits when members need them. That includes pension payments, lump sum withdrawals, and death benefits. If you are drawing a pension, you need assets that can generate income. If you have illiquid assets, you need a plan for meeting benefit payment obligations.

5. Insurance

Your strategy must consider whether members should hold insurance through the fund. This requirement comes from Reg 4.09 of the SIS Regulations (the four areas above come from s.52B of the Act). That does not mean you must have insurance. You can decide it is not appropriate. But you must consider it and document your decision.

Many trustees skip this requirement. They do not consider insurance, do not document the decision, and do not review it. That is a breach, even if the decision is that insurance is not needed.

The Annual Review Requirement

Your investment strategy must be reviewed at least annually, and that review must be documented in trustee minutes. The review should consider whether the strategy is still appropriate, whether actual investments match the strategy, and whether any changes are needed.

Many trustees have a strategy but never review it. Others review it but do not document the review. Both are breaches. The ATO expects to see annual reviews documented in trustee minutes, showing that trustees have actively considered the strategy and made informed decisions.

Common Mistakes

Many SMSF trustees make investment strategy mistakes. They use a generic template that does not reflect actual investments. They do not address all five required areas. They do not review the strategy annually. They do not document reviews. They have a strategy that says one thing but invest in another.

These mistakes can result in penalties, audit findings, and in serious cases the fund being made non-complying. The cost of fixing a non-compliant strategy is often far higher than the cost of getting it right from the start.

The bottom line: Your investment strategy is not optional. It is a legal requirement. It must address all five areas, be reviewed annually, and match your actual investments. A "set and forget" strategy can become a costly breach.

Check Your Investment Strategy

Use the SMSF Suite to step through the five required areas and track your review date.

Open the SMSF SuiteWhat it costs to keep modelling

Try the SMSF Suite free first. Unlimited SMSF tools plus Advanced Retirement are All Access at $399 a year, or $39.99 a month if you’d rather not commit upfront.

Open the SMSF Suite →Free SMSF suite runs first, no card required. Subscribe only if the tools are useful enough to keep using.

Disclaimer: This article is for general information only. It is not financial product advice, personal advice, or a recommendation. It does not take into account your objectives, financial situation, or needs. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). SMSF investment strategy requirements are complex and the penalties for non-compliance can be severe. You should consult a licensed SMSF specialist or accountant for advice specific to your circumstances before finalising or changing your investment strategy.