You've spent decades accumulating super. Now comes the harder question: how do you draw it down without running out? The withdrawal strategy you choose can mean the difference between a comfortable retirement and running out of money at 85. If you're also expecting Age Pension or other retirement income, the maths gets more complex, and the taper can force you to spend down principal unless returns beat 7.8%. Modelling both together is essential.

Australia's Minimum Drawdown Rules

First, understand that the government mandates minimum withdrawals from super pensions. Unlike the American "4% rule," Australian retirees must withdraw at least these percentages:

| Age | Minimum Withdrawal |

|---|---|

| Under 65 | 4% |

| 65-74 | 5% |

| 75-79 | 6% |

| 80-84 | 7% |

| 85-89 | 9% |

| 90-94 | 11% |

| 95+ | 14% |

These are floors, not ceilings. You must withdraw at least this much, but you can withdraw more. Any withdrawal strategy must respect these minimums.

Key difference from the US: The popular American "4% rule" assumes you can withdraw just 4% indefinitely. In Australia, you're required to withdraw 5% from age 65, rising to 14% by 95. This fundamentally changes the maths.

Fixed Sustainable Income: Cleaner Budget, Less Upside

Fixed sustainable income starts with a simple promise: the same real income each year. If the figure is $80,000, the plan is built around $80,000 in today's dollars rather than a percentage that jumps around with the market.

The trade-off is obvious. You get a cleaner household budget, but you give up some upside if markets are kind. The method also depends on the historical period being tested. A number that survived one bad sequence is not a guarantee against a worse future sequence, but it is a tougher test than assuming a smooth average return.

This style suits people who want a clear income floor and are prepared to accept that the plan may leave money on the table in strong markets.

Dynamic SWR: Responsive, But Less Tidy

Dynamic safe withdrawal rate is less tidy. It recalculates income as the balance and remaining time horizon change. Good markets can lift spending. Bad markets can pull it down.

A retiree with $1 million and a 30-year horizon might begin around one income level, then adjust as the portfolio and remaining years change. The useful feature is not precision to the dollar. It is the willingness to cut spending after bad years and release more after good years instead of pretending nothing has changed.

The advantage is responsiveness. A 70-year-old with $1 million and 20 years left can usually draw more than a 65-year-old with the same balance and 30 years left. The cost is that the household has to tolerate income moving around.

Vanguard Dynamic Spending: Smoother Adjustments

Vanguard's dynamic spending method tries to avoid the whiplash of pure recalculation. It sets a target withdrawal rate, then limits how much income can rise or fall in a single year.

That restraint cuts both ways. In a bad year, spending may fall less sharply than a fresh percentage calculation would suggest. In a strong year, the method may hold back some of the upside. It is a compromise for households that can accept adjustments but not violent swings.

The appeal is practical. Income moves, but not violently. You accept smaller rises in good years so the bad years do not force a brutal cut.

Floor and Ceiling: Guardrails for Real Life

The floor-and-ceiling method uses guardrails. Spending continues normally while the withdrawal rate stays inside a chosen band. If the portfolio falls far enough that the withdrawal rate becomes too high, spending is cut. If the portfolio grows enough that the rate becomes too low, spending can rise.

It is not set-and-forget. Someone has to check the guardrails each year. But it avoids two common mistakes: cutting spending after every market wobble, or refusing to cut after a genuinely damaging sequence.

For many households this is the most intuitive version: spend normally until the plan gets too close to an edge, then adjust.

What the Comparison Really Shows

The choice is not between a clever strategy and a foolish one. It is a choice about temperament. Some households value a steady pay packet above all else. Others can handle variable spending if it improves the odds of keeping the plan alive. The Age Pension also changes the comparison, because it can soften the effect of lower super balances later in retirement.

| Strategy | Income Stability | Portfolio Protection | Complexity |

|---|---|---|---|

| Fixed Sustainable Income | High (constant real income) | High (tested against historical data) | Low (set and forget - same amount every year) |

| Dynamic SWR | Medium | High | Medium (requires annual recalculation) |

| Vanguard | Medium-High | Medium-High | Medium (requires annual monitoring) |

| Floor/Ceiling | High | High | Medium (requires annual guardrail checks) |

Withdrawal strategy dropdown showing all four strategy options

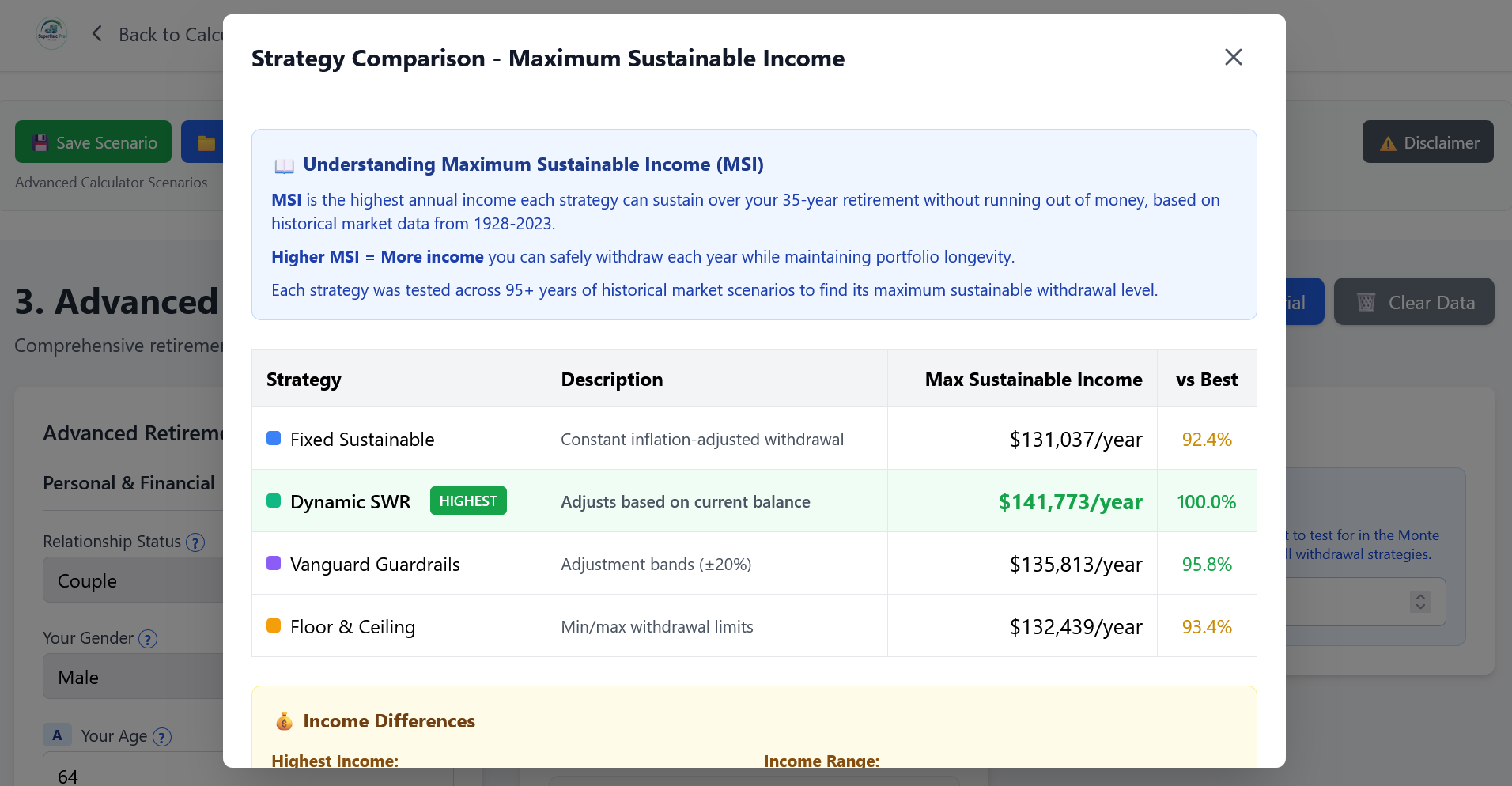

Comparison of income outcomes across all four withdrawal strategies

The Age Pension Changes Everything

If you're eligible for the Age Pension, the maths changes significantly. The pension provides a guaranteed income floor, meaning you can potentially be more aggressive with super withdrawals. Your super becomes a "top-up" rather than your sole income source.

As your super balance declines through withdrawals, your Age Pension entitlement increases (due to the assets test). This creates a natural smoothing effect that most calculators ignore. A retiree who starts with $500,000 in super might receive a partial Age Pension. As they draw down their super over the years, their pension increases, partially offsetting the declining super withdrawals. This dynamic interaction means your total sustainable income can be tens of thousands of dollars higher per annum when the Age Pension is included in the calculation.

Key insight: Model scenarios with AND without pension. The difference in total sustainable income can be substantial, often tens of thousands of dollars per annum higher when pension is included. For example, a couple with $100,000 in super might receive $40,000+ per year from the Age Pension alone, dramatically increasing their total retirement income. This interaction between super drawdowns and pension entitlements is one of the most overlooked aspects of Australian retirement planning.

Compare All 4 Withdrawal Strategies

Test Fixed Sustainable Income, Dynamic SWR, Vanguard Dynamic Spending, and Floor/Ceiling against your balance and Age Pension eligibility.

Run the 60-Second Stress-TestRun your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator