Contents

What is Division 296 tax?

What is Division 296 tax?

Division 296 tax is an additional tax on the proportion of super earnings linked to very large super balances from 1 July 2026. It applies when Total Super Balance exceeds $3 million, with an extra tier above $10 million, and is separate from Division 293 tax on concessional contributions.

Division 296 is an additional tax on superannuation earnings attributable to the part of a member's Total Super Balance (TSB) above the large super balance threshold. It is enacted law under the Treasury Laws Amendment (Building a Stronger and Fairer Super System) Act 2026, which received Royal Assent on 13 March 2026 and applies from 1 July 2026 (2026-27 financial year). For 2026-27 the large super balance threshold is $3 million and the very large super balance threshold is $10 million. Both thresholds index to CPI in $150,000 and $500,000 steps respectively.

Unlike Division 293, which targets high earners through concessional contributions, Division 296 targets high balances regardless of income. An additional 15% tax applies to the proportion of Division 296 earnings relating to the balance above $3 million. Where balance exceeds $10 million, a further 10% applies to the earnings proportion above that higher line. See also super rules from 1 July 2026 for how this sits alongside indexed caps.

The stated policy rationale is that very large super accounts receive concessional fund earnings tax that is generous relative to top marginal personal rates. Division 296 reduces that concession on the slice of earnings attributable to balances above the thresholds. It does not tell you to withdraw super or restructure funds; it describes how the tax works so you can seek advice if it may apply to you.

Large super balance threshold (LSBT): $3,000,000, CPI-indexed in $150,000 steps. Very large super balance threshold (VLSBT): $10,000,000, CPI-indexed in $500,000 steps. Additional tax: 15% on the earnings proportion above LSBT, plus 10% on the proportion above VLSBT. Applies to Total Super Balance across all funds from 1 July 2026. Defined benefit interests use a different earnings calculation. Status: enacted law (Royal Assent 13 March 2026).

Who is affected?

Treasury modelling during the legislative debate estimated on the order of 80,000 Australians could eventually be affected, a small fraction of all super members. Because thresholds now index to CPI, the nominal lines rise over time but real exposure still grows as balances compound. A balance of $2.5M today, growing at 7% annually, crosses $3M in approximately four years without additional contributions.

Division 296 applies to members whose Total Super Balance across all funds exceeds the relevant threshold when tested under ATO rules for the financial year from 2026-27 onwards. That includes SMSFs, APRA-regulated funds, retail funds, or any combination. Pension-phase assets still count toward the balance test. The pension-phase rules do not remove a member from Division 296 merely because they are drawing a pension.

How the tax is calculated

Division 296 uses Division 296 fund earnings, not a raw change in Total Super Balance. The ATO publishes how funds and members report those earnings. At a high level the calculation still has three conceptual steps: work out earnings, work out what proportion of the balance sits above each threshold, then apply 15% and (where relevant) 10% to the earnings attributable to those proportions. You can model these steps in the Division 296 calculator.

Step 1: Division 296 earnings

Earlier drafts used Total Super Balance movement as a proxy, which would have included unrealised capital gains. The enacted law does not tax unrealised gains in that way. SMSF trustees still need annual asset valuations for compliance, but a paper property uplift alone does not automatically create Division 296 earnings under final law unless realised under the ATO's rules. If earnings are zero or negative for the year, no Division 296 tax applies.

Step 2: Proportions above $3 million and $10 million

Not all earnings face the additional rates. Only the fractions attributable to balance above each threshold are taxed at the higher rates. If year-end TSB is $3.4M, the proportion above $3M is ($3.4M - $3M) / $3.4M = 11.8%. From later years the ATO uses the greater of TSB immediately before the financial year and at 30 June when testing whether thresholds are exceeded.

Step 3: Apply 15% and 10%

This is additional tax on top of standard fund earnings tax in accumulation phase. For balances well above $3M the effective rate on the excess portion moves toward 30% at the LSBT tier, with a further layer above $10M.

Realised earnings under final law

The most contested feature of earlier drafts was taxation of unrealised capital gains through a Total Super Balance movement test. That design attracted heavy criticism from SMSF trustees with illiquid property and unlisted assets, who could have faced cash tax bills without a sale. The enacted law taxes Division 296 fund earnings, which the ATO describes in terms of realised outcomes rather than paper revaluations alone.

SMSF trustees still obtain annual market valuations for the SMSF return and audit. Those valuations matter for compliance and for Total Super Balance reporting, but they do not automatically mean every valuation uplift becomes Division 296 earnings under final law. APRA-regulated fund members generally see earnings track fund crediting rates and realised gains in any case. The cash-flow risk from taxing paper gains directly was substantially reduced compared with the 2024 bill draft, though large balances can still face meaningful tax on strong realised years.

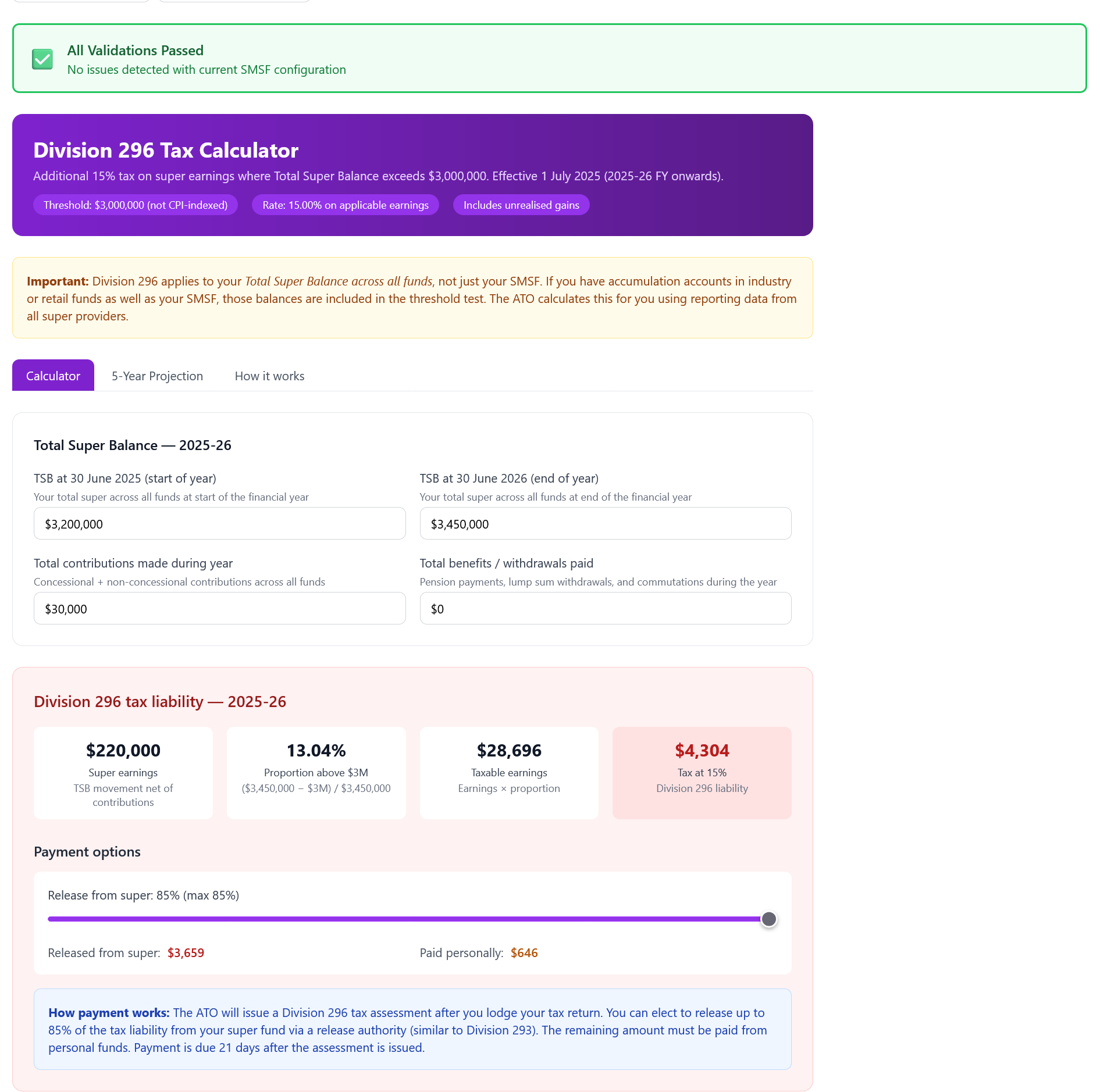

Worked example: $3.5M SMSF balance

Scenario: Single member SMSF, accumulation phase

| Item | Amount |

|---|---|

| TSB at 1 July 2026 (start of year) | $3,200,000 |

| Concessional contributions during year | $32,500 |

| Benefits paid / withdrawals during year | $0 |

| TSB at 30 June 2027 (end of year) | $3,450,000 |

| Division 296 earnings (illustrative) | $217,500 |

Step 1 - Division 296 earnings (illustrative):

Step 2 - Proportion above $3M:

Step 3 - Division 296 tax at 15%:

| Result item | Amount |

|---|---|

| Division 296 earnings | $217,500 |

| Proportion above threshold | 13.04% |

| Tax at 15% tier | $4,253 |

Illustrative only (~$4,250 from the arithmetic above). The calculator screenshot below can differ slightly with rounding or input detail (~$4,300). Actual Division 296 earnings come from ATO reporting rules, not necessarily TSB movement. No VLSBT tier applies while TSB remains below $10M.

Payment options

The ATO issues a Division 296 tax assessment after the member lodges their income tax return. Payment is due 21 days after the assessment date. There are two ways to pay.

Pay personally

You pay the full amount from personal (non-super) funds. The super fund retains its full balance. Many members with illiquid SMSF assets prefer keeping tax outside super when they can, though that requires personal liquidity.

Release authority from super

A member may elect to release up to 85% of the assessed tax from super via a release authority. The remaining amount must come from personal funds. Division 293 allows up to 100% release from super, so Division 296 always leaves at least a small personal cash component when release is used.

The 85% cap is designed to prevent a full-release scenario where tax is paid on earnings that were entirely funded by the member's own contributions, leaving the fund with no net benefit from those contributions.

Division 296 vs Division 293: key differences

| Feature | Division 293 | Division 296 |

|---|---|---|

| Trigger | Income for surcharge purposes > $250,000 | TSB above LSBT ($3M for 2026-27) |

| Tax base | Concessional contributions | Division 296 fund earnings (proportion above thresholds) |

| Additional rate | 15% | 15% above LSBT + 10% above VLSBT |

| Threshold indexed? | No, $250k unchanged since 2012 | Yes, CPI-indexed ($150k / $500k steps) |

| Applies from | 2012-13 | 2026-27 |

| Release authority limit | Up to 100% from super | Up to 85% from super |

| Applies to defined benefits? | Yes (different formula) | Yes (notional earnings formula) |

| Can both apply in same year? | Yes, they use different tax bases and are calculated independently | |

Planning strategies

Members above or approaching $3M in total super have a number of structural options worth reviewing with a licensed adviser. The right approach depends on the full picture: income, age, fund structure, defined benefit interests, estate planning objectives, and more. The strategies below are general in nature and involve trade-offs that require individual modelling. Use the Division 296 calculator to stress-test balance paths before you change contributions or withdrawals.

Spouse contribution splitting

Where one partner holds a large super balance and the other is below $3M, directing contributions to the lower-balance partner and splitting existing concessional contributions can reduce or eliminate the high-balance partner's Division 296 exposure. The most effective outcome is where both partners finish the year below $3M, so neither is liable. The spouse contributions guide covers the mechanics and contribution limits.

Non-concessional contribution timing

Non-concessional contributions increase TSB at the start of the next year without directly causing earnings in the year they are made. They do push the balance higher, which means more future earnings will fall above the $3M threshold. The value of large non-concessional contributions is worth reconsidering when the balance is near $3M.

Pension-phase assets and the Transfer Balance Cap

The Transfer Balance Cap controls how much can be held in tax-free pension phase. Pension-phase assets still count toward the $3M threshold test for Division 296 purposes. Maximising pension-phase assets within the cap reduces accumulation-phase earnings tax but does not avoid Division 296 when total super exceeds $3M.

SMSF asset mix and liquidity planning

Trustees with illiquid assets face the sharpest cash-flow risk from Division 296. Holding sufficient liquid assets to cover at least one year's estimated Division 296 liability reduces the risk of forced asset sales to meet the tax bill. An annual modelling exercise before 30 June, using updated asset valuations, helps avoid surprises at assessment time.

Partial withdrawal and re-contribution

Withdrawing super and re-contributing to a lower-balance spouse's account or investing outside super are options that many advisers consider in this context. Re-contributions may trigger the non-concessional caps, and withdrawals from accumulation phase carry tax implications depending on the taxable and tax-free components of the member's interest. Detailed modelling is needed before proceeding.

Model your Division 296 liability

Use the Division 296 calculator to estimate liability for 2026-27 and see a 5-year projection based on your current balance.

Open Division 296 CalculatorSpecial considerations for SMSF trustees

Division 296 creates some unique challenges for SMSF trustees that do not apply to the same degree for members of large APRA-regulated funds.

Annual valuations still matter. SMSF trustees must value all assets at market value each year for the annual return and audit. Those valuations feed Total Super Balance reporting even though unrealised gains are not taxed as Division 296 earnings under final law.

Audit and lodgement timing. The SMSF annual return and audit must be completed before the member lodges their individual tax return. Late lodgement delays the assessment and may attract ATO penalties. Timely SMSF reporting becomes more financially consequential for high-balance trustees from 2026-27.

Related-party transactions. Valuing related-party assets such as real property requires arm's length evidence. The ATO can scrutinise valuations where TSB reporting affects threshold tests.

Defined benefit interests within SMSFs. Pure defined benefit SMSFs are rare but do exist. Trustees of such funds should confirm with their adviser which earnings calculation applies, as the notional earnings formula differs from the adjusted TSB method used for standard accumulation accounts.

Frequently asked questions

Does Division 296 apply to the entire balance or just the amount over $3M?

Neither, exactly. The tax applies to the portion of earnings attributable to the balance above $3M. The proportion formula, (TSB_end - $3M) / TSB_end, determines what fraction of earnings is taxable. Only that fraction of earnings faces the additional 15%; the rest continues at the standard fund tax rate. The Division 296 calculator walks through this with your own balance inputs.

What if my balance drops below $3M mid-year?

From later years the ATO compares TSB immediately before the financial year and at 30 June, using the higher figure for threshold tests. For 2026-27 transitional rules may differ; check current ATO material. If you are below the threshold on the relevant test date, no Division 296 applies for that year regardless of mid-year spikes.

Can Division 296 tax be offset by fund losses in a future year?

If Division 296 earnings are negative or zero in a subsequent year, no Division 296 tax applies for that year. There is no general carry-back to recoup tax paid in earlier years. Confirm current law and ATO guidance with a licensed tax adviser.

Does Division 296 apply to pension-phase assets?

Yes. Division 296 applies to total super balances including pension-phase interests for threshold purposes. The pension-phase tax exemption within the Transfer Balance Cap continues at fund level. Division 296 is an additional personal assessment on the member.

What happens if I have super in multiple funds?

The ATO aggregates Total Super Balance reporting from all super providers. The Division 296 assessment is issued to the individual. The member decides which fund, if any, receives a release authority.

Is there a minimum age for Division 296 to apply?

No. Division 296 applies based on balance and earnings, not age. It can affect accumulation-phase members of any age and retirees drawing a pension from a total balance above the thresholds.