What is a phased retirement calculator for couples?

A phased retirement calculator for couples models different retirement ages, wages while one partner still works, super preservation access, and Age Pension eligibility year by year. SuperCalc Pro does this in the Advanced Retirement Calculator with historical stress testing and Monte Carlo survival probability.

Important: General information only, not financial product advice. SuperCalc Pro does not hold an Australian Financial Services Licence (AFSL). The article does not recommend opening, closing, or changing any super fund or product. Seek advice from a licensed financial adviser, SMSF specialist, or accountant as appropriate.

Most couple calculators still assume both partners stop work on the same day. That is tidy for software, less tidy for households. One partner hits preservation age and wants out; the other has five years of mortgage or a job they are not ready to leave. Households with one partner retired and one still working need different maths from a tool that only accepts one retirement date.

Centrelink assesses you as a couple, but super access and wages do not line up on one calendar. A household with one partner retired and one still working can look fine on a napkin projection while the year-by-year cash flow is wrong. What you need is to run each phase through to full retirement (and Age Pension where it applies), not a higher average return plugged into a single retirement date.

Why a single retirement date fails for couples

A typical free calculator asks for one retirement age and one combined super balance. That is the wrong shape for most couples. Preservation age is 60 for people born from 1 July 1964 onward, but partners rarely reach that line on the same calendar year. The older partner may start a pension while the younger partner's balance is still locked and still receiving employer contributions. Minimum drawdown rules apply per account, not per household feeling.

Age Pension adds another layer. Eligibility is generally 67, and Centrelink tests the couple as a unit. When one partner is still working, employment income can reduce or delay pension support for the household even if the retired partner is already drawing super. Deeming on financial assets still runs in the background. The deeming rules do not pause because one person has left work.

Sequence risk hits phased households harder than the headline balance suggests. If the first partner retires into a weak market and starts drawing while the working partner's contributions are modest relative to the drawdown, capital can shrink in the years that matter most. A plan that survives on a smooth 7 percent average can fail when the first five retired years are ugly. That is the same sequence problem as any retirement, but the timing of who draws first amplifies it.

The five household phases worth modelling

Household income rarely jumps straight from "both working" to "both on the pension." The transitions matter. In practice you move through something like the following:

- Both partners working, with employer SG still landing in super.

- One retired and one working: wages, tax, super drawdowns, and any part-pension tests all interact.

- Both retired but under Age Pension age, living mainly on super.

- One partner on Age Pension while the other is still working or under pension age.

- Both at pension age, with super drawdowns topping up whatever the means tests allow.

Skip a transition in the model and you are guessing which years actually carry the plan.

Engine-backed example: three-year stagger

Inputs (same as the Advanced Calculator example scenario)

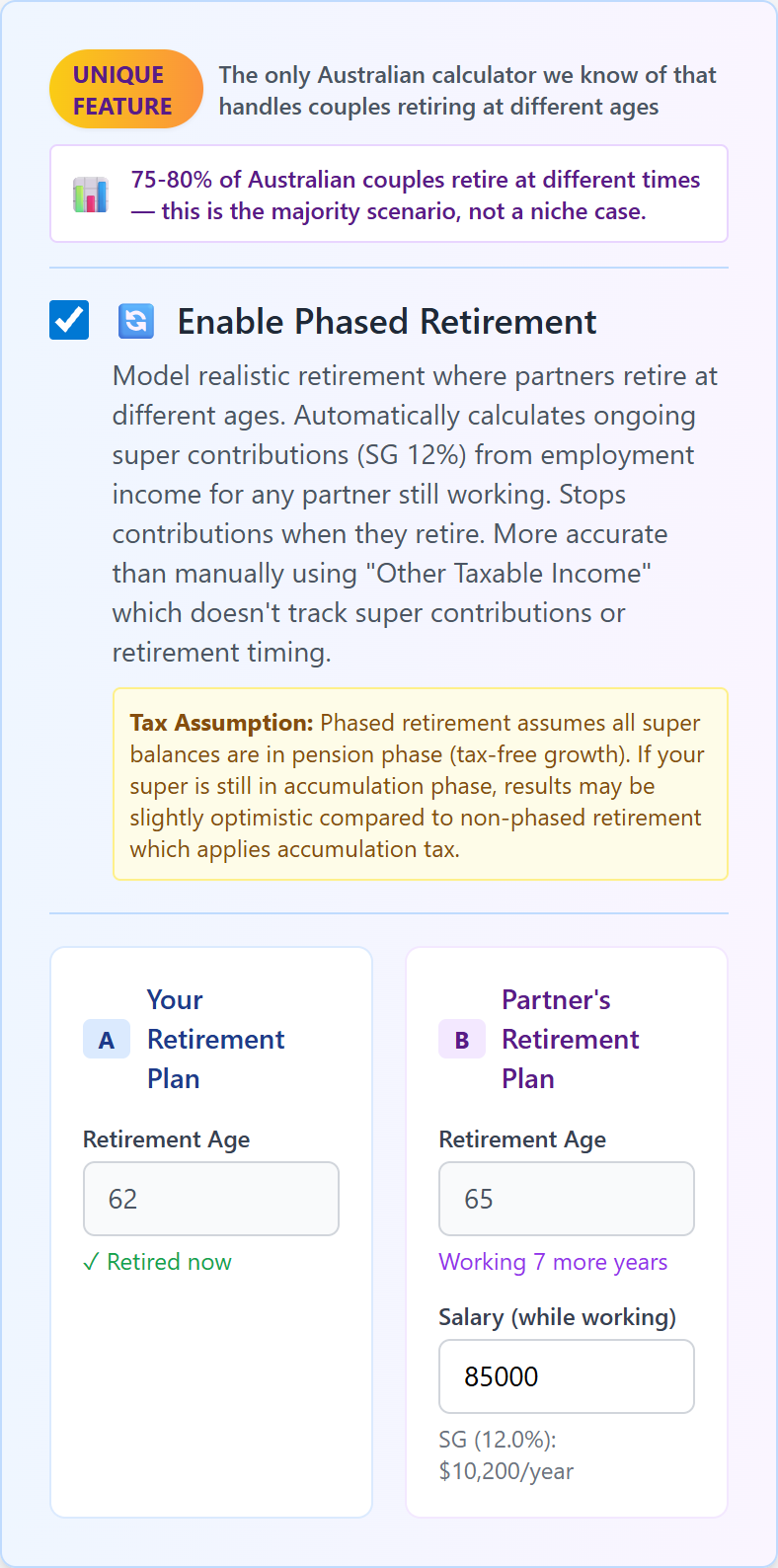

Partner A is 62 with $520,000 in super and retires now. Partner B is 58 with $310,000 in super, earns $85,000, and retires at 65. The household is homeowner with $70,000 in other assessable assets, Age Pension is modelled, and the plan runs 34 years. Allocation: 25% S&P 500, 35% Australian shares, 20% international, 15% bonds, 5% cash, with engine-default admin and investment fees.

Flat comparison (common calculator error): both partners retire at 62, phased retirement off, no wages after that date. Across 65 historical start years (1928 through 1992), the median maximum sustainable income is $84,682 per year (real, in today's dollars). MSI here includes modelled Age Pension where eligible, not super drawdown alone.

Phased model: Partner A retires at 62, Partner B keeps working to 65 with $85,000 salary and employer super guarantee until exit. Median MSI rises to $105,898 per year, a gap of $21,216 (about 25% on those rounded medians). We also computed the uplift for each of the 65 start years separately (phased MSI divided by flat MSI, year by year) and took the median of those 65 ratios: 25.5%, with a 10th-to-90th percentile band of roughly 20% to 35%. The two headline percentages differ slightly because one compares rounded medians and the other is the median of per-year ratios. Your numbers will differ with different balances, ages, fees, and allocation.

1973 start year (stress case): flat both-at-62 MSI is $61,156. Phased MSI is $89,606. In year five of that path the phased household still has B's $85,000 wage plus a super draw of about $21,700, while the flat model is drawing the full $61,156 from super alone and the combined balance has fallen to $240,231. Wages and SG during the stagger reduce early drawdown pressure in this scenario; other inputs can produce a smaller uplift or none at all.

Method: Fixed maximum sustainable income via binary search on the same historical return paths, with Australian Age Pension, deeming, minimum drawdowns, and phased SG modelled in the SuperCalc Pro engine. General information only, not personal advice.

Stagger is not a free lunch. If the working partner's income pushes the household into a tighter pension taper, or if the first retiree draws too hard in a weak market, a phased plan can underperform a conservative "retire together and spend less" approach. The engine output above is specific to the inputs shown. Change the salary, the retirement ages, or turn pension off and the uplift can shrink or reverse.

Whose super to draw first?

There is no universal rule, but the trade-offs are stable. Drawing from the older partner's super first uses the account that is already accessible. Leaving the younger partner's balance invested can mean more years of compounding before it must feed income. Equalising balances through spouse contributions or contribution splitting can change Age Pension outcomes later, because assets and income tests look at the household, not at whose name is on the account.

Transition to retirement pensions add another lever for the still-working partner in some cases, though the benefit depends on age, work pattern, and tax position. "Whose super" is a year-by-year call tied to access rules, not a one-off allocation you set at 60 and forget.

For pension timing, read younger partner Age Pension alongside this piece. A couple can have one partner on full or part pension while the other is still in the workforce. That mixed state is normal, not exotic.

Historical stress testing beats a single average

Phased retirement does not remove market risk. It moves the first drawdown earlier or later depending on who stops first. The Monte Carlo retirement calculator landing page explains how synthetic paths and replayed history differ. For couples, run both. Historical simulation answers how the plan would have fared in real Australian return sequences, including bad decades. Monte Carlo answers how sensitive the plan is to assumptions about future volatility.

When historical replay and Monte Carlo disagree, that usually tells you which assumption is doing the work. Maybe the working partner's wage is carrying more of the plan than you thought. Maybe the first retiree is drawing too hard relative to ongoing SG. Treat a single median MSI line as one output from the model, not the whole story.

How to run the numbers in SuperCalc Pro

Start from the Advanced Retirement Calculator landing page if you want context on methodology, then open the app. Set relationship status to couple. Enter each partner's current age, super balance, and intended retirement age. Enable phased retirement so employment income and super guarantee continue until each partner's retirement date. Add homeowner status, spending target, and any fees you pay in real life.

Run historical simulation first. Look at sustainable income, worst start year, and the year-by-year table of income by source. You want to see wages dropping out on the right dates, super pensions starting when preservation age allows, and Age Pension appearing when eligibility rules say it should. Then run Monte Carlo for survival probability at your spending goal.

Change one input at a time. Delay Partner A's retirement by two years. Cut spending by 10 percent. Test what happens if Partner B works part-time instead of full-time. Phased models are useful precisely because those knobs exist.

Official sources

Preservation age, pension age, and Centrelink means tests change with legislation. Verify current rules before acting:

ATO: when you can access your super

Load the couple phased-retirement example

The built-in scenario (62/58, $520k/$310k, B works to 65 on $85k) matches the engine numbers in the box above. Adjust ages and balances, then replay history.

Open the Advanced Retirement CalculatorBottom line

Phased retirement for couples is a sequencing problem: preservation age, wages, drawdowns, and Age Pension eligibility move at different speeds. A calculator with one retirement date cannot tell you whether Partner A can stop at 62 while Partner B works to 65 without running out of runway in year four of a bad market.

Run the phases. Stress-test the years when only one income source is doing the work. Any uplift percentage in the box above comes from stated inputs and engine methodology; rerun it with your own ages, balances, and wages before treating it as a forecast.

Disclaimer: This article is general information only. It is not financial product advice or personal advice. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). We do not recommend that you open, close, or change any super fund or product. Simulation results depend on inputs and methodology. Past data does not predict future performance. Government rules and rates change. For advice tailored to your situation, see the ATO, Services Australia, or a licensed financial adviser.