Age gaps are common in Australian couples. So is the situation where one partner reaches the Age Pension qualifying age of 67 before the other. What many people do not realise is that once you qualify, Centrelink treats you as a member of a couple from day one. That means you get the couple rate, not the single rate, and your partner's income and assets count in your means test even though they are not yet receiving anything. For couples planning a phased wind-down from work, the interaction between the younger partner's income, the older partner's pension, and the income and assets tests is one of the most commonly misunderstood parts of retirement planning. This article is general information only. It is not personal or financial product advice. For advice on your own situation, see Services Australia or a licensed financial adviser.

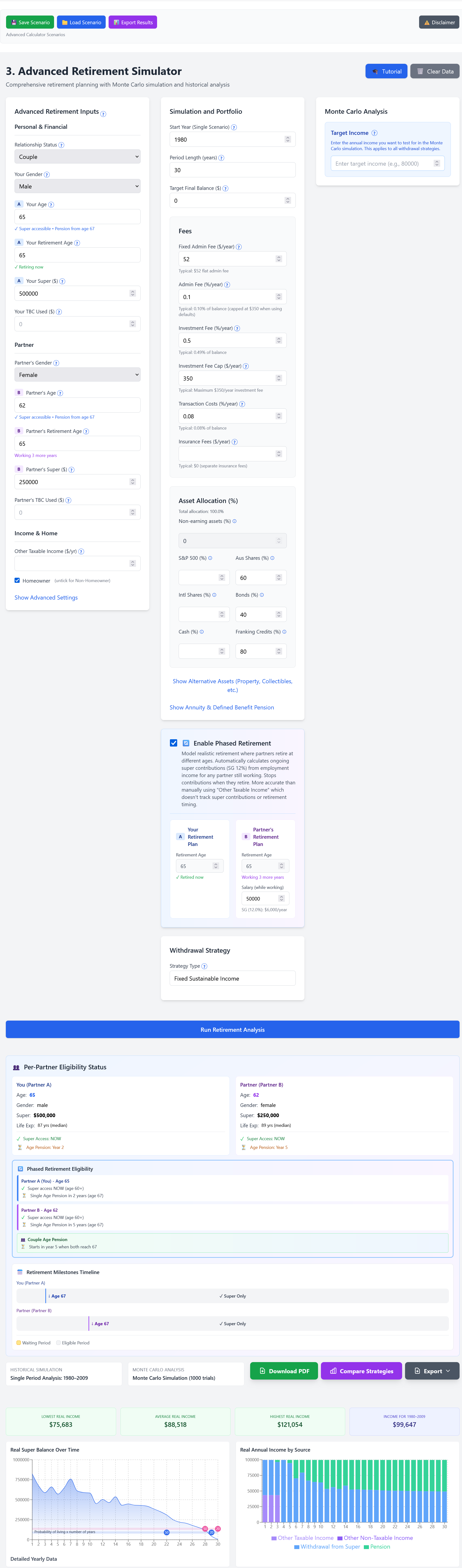

The Advanced Calculator models this three-phase household transition directly. Enter each partner's age, super balance, salary, and retirement age. The simulator automatically moves through the phases: both working, one retired and one still working, then both retired. It uses the combined household asset base throughout and applies the correct pension thresholds for each year. You can open it here.

The Couple Rate vs the Single Rate

The full Age Pension for a single person is higher per person than each person's share of the couple rate. That is by design: Centrelink assumes couples share living costs. From 20 March 2026, the full single rate is $1,200.90 per fortnight. The full couple rate is $905.20 per fortnight per person ($1,810.40 combined). If you reach pension age and your partner has not, you receive the couple rate - $295.70 less per fortnight than the single rate. That gap stays in place until your partner also qualifies, or until you stop being assessed as a couple.

How Centrelink Assesses the Means Test

The taper rate and the income-free area both apply at the couple level. For a couple, the combined income-free area is higher than for a single person, but the income from both people counts. Here is what goes into the test when only one partner is eligible:

| What counts | Included in means test? |

|---|---|

| Both partners' financial assets (bank, shares, managed funds) | Yes |

| Both partners' non-financial assets (car, contents, etc.) | Yes |

| Family home | No (exempt asset) |

| Younger partner's income (wages, investment income) | Yes |

| Older partner's investment income (deemed) | Yes |

| Younger partner's super (accessible - over preservation age) | Yes - assets test |

| Younger partner's super (preserved, not accessible) | Generally no - assets test |

| Younger partner's super pension payments (if drawing TTR) | Yes - income test |

Preservation age is 60 for anyone born after 30 June 1964. If the younger partner is, say, 63 and still working, their super balance is in accumulation phase and not accessible. In most cases that balance is excluded from the assets test. But their wages, salary, and any investment income still count in the income test. Once they start drawing down (for example via a transition to retirement pension), those payments become assessable income too.

The Phased Retirement Angle

Many couples do not retire at the same time or at the same pace. A common pattern is for the older partner to stop working first and begin receiving the Age Pension, while the younger partner keeps working full time, then scales back to three days a week, then two, before eventually stopping. This is phased retirement in practice, and Centrelink's assessment follows the younger partner's income through every step.

When the younger partner is still working full time, their income is likely to push the couple's combined income above the income-free area, reducing or eliminating the older partner's pension. As the younger partner reduces hours, that income falls, and the pension can increase. The transition is gradual. This is worth modelling before the older partner applies, not after, because the timing of when to claim can affect how much pension you actually receive during the transition years.

Transition to Retirement and the Income Test

Some people in the 60-67 bracket use a transition to retirement (TTR) income stream to supplement reduced wages while they scale back. If the younger partner starts a TTR pension, those pension payments count as income in the income test. The younger partner's super balance, now paying a TTR pension, also counts as an asset. This can reduce the older partner's Age Pension further during the phasing period.

It is worth checking whether the tax benefits of a TTR arrangement outweigh the impact on the couple's combined pension. That calculation depends on the younger partner's wage level, their super balance, and how much pension the older partner is currently receiving. A licensed financial adviser can model this. The Advanced Calculator can show the pension impact of different income levels as the younger partner reduces work, letting you see the household income across each stage.

When the Younger Partner Reaches Pension Age

The picture changes meaningfully when the younger partner also turns 67 and qualifies. From that point, both partners are assessed for the Age Pension. The couple rate stays the same per person, but now both are entitled to receive it, so household pension income roughly doubles. If the younger partner's super was previously excluded from the assets test (because it was in preserved accumulation phase), it now counts as an assessable asset. A large balance shifting into the assets test at that point can reduce or cancel one or both payments. Running the numbers a few years ahead lets you plan for that transition.

| Phase | Who receives pension | Rate | Younger partner's super counted? |

|---|---|---|---|

| Before older partner turns 67 | Neither | - | No (preserved) |

| Older partner 67+, younger 60-66 (not yet accessible) | Older partner only | Couple rate | Generally no |

| Older partner 67+, younger 60-66 (TTR in payment) | Older partner only | Couple rate | Yes - asset and income |

| Both partners 67+ | Both (if eligible) | Couple rate each | Yes - asset |

The Work Bonus for the Older Partner

If the older partner does some casual or part-time work after claiming the pension, the Work Bonus applies: the first $300 per fortnight of their employment income is exempt from the income test. This applies only to their own employment income, not to the younger partner's income. The couple's income test still counts both people's income from all other sources. So the Work Bonus can help at the margin if the older partner picks up occasional work, but it does not shield the younger partner's wages.

Why Most Calculators Get This Wrong

Most publicly available Australian retirement calculators assume both partners retire at the same time or treat each partner as a separate individual. When a couple uses two single-person calculators and adds the results, the numbers are wrong because:

- The asset test threshold for couples is different from twice the single threshold

- The deeming threshold for couples is different

- The income-free area is a combined amount, not twice the single amount

- The younger partner's income directly reduces the older partner's pension, not separately assessed

- The transition year - when one partner hits 67 - changes the pension parameters for the whole household, not just one person

The deeper problem with the two-singles approach is that it produces a suboptimal result for maximum sustainable household income. To find the retirement timing that maximises what a couple can sustainably draw over 30 years, you need to compare scenarios: the older partner retiring now versus in two years, the younger partner retiring at 62 versus 65, whether the working partner's continued contributions outweigh the pension reduction their income causes. None of that is possible unless both partners' incomes, assets, super balances, and pension outcomes are modelled together in a single simulation. The ASIC MoneySmart retirement planner and most super fund calculators take a single retirement age and produce one number at that point. They cannot find the optimal retirement timing for a couple because they do not model the couple as a household across time.

Advanced Calculator: phased retirement simulation showing household income across all three phases year by year

Practical Steps Before Applying

A few things worth checking before the older partner lodges a claim:

- What is the younger partner currently earning, and what does their income plan look like over the next one to five years?

- What are the combined assessable assets, and is the younger partner's super accessible or preserved?

- Does the younger partner have a TTR arrangement in place or planned? If so, how does that affect the income test?

- Is the income test or the assets test currently the binding one, and will that change as the younger partner reduces work? (See our article on which test applies.)

- At what income level does the older partner's pension reduce to zero? Is the younger partner currently above or below that?

Services Australia has an online estimator tool, but it is a point-in-time estimate. The Advanced Calculator lets you model the trajectory: enter the current position and then step through future years as the younger partner reduces hours and eventually qualifies.

Run your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator