What is the Work Bonus?

The Work Bonus is an Age Pension rule that reduces how much employment or self-employment income counts under the pension income test. It lets eligible pensioners earn some work income before their pension is reduced, and unused amounts can build up in a Work Bonus balance.

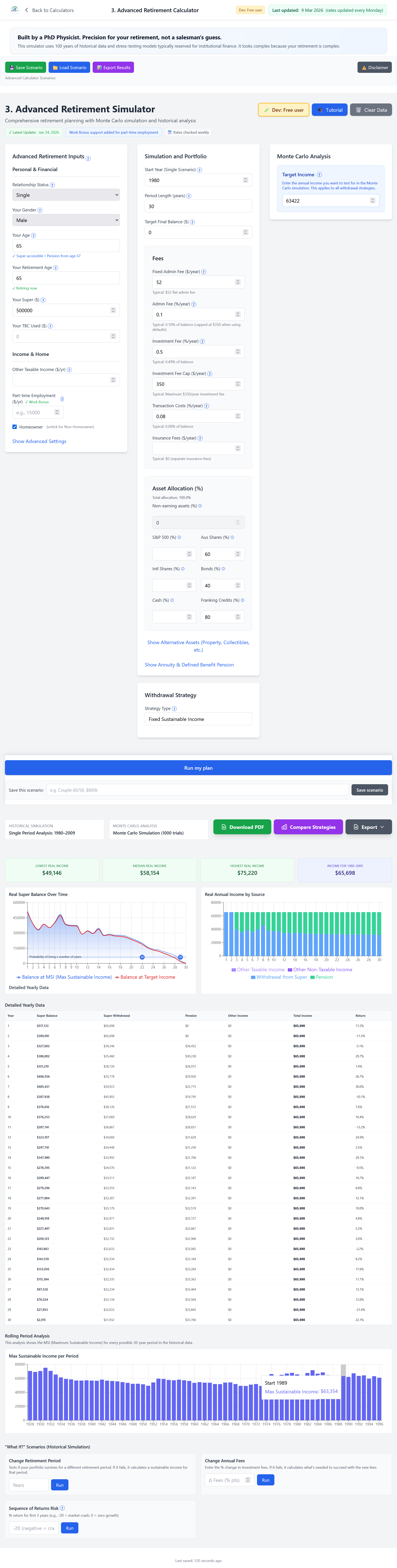

Many people work part time or casually after they qualify for the Age Pension. The Work Bonus lets you earn up to $300 per fortnight from employment before that income is counted in the income test. That can make a real difference to how much pension you keep when you work. This article explains how the Work Bonus works, the income bank, and who benefits. It does not recommend that you work or stop working; it is general information only. You can see how work income and pension interact year by year in our Advanced Calculator.

Centrelink uses both an assets test and an income test for the Age Pension. You get the lower of the two results. The income test has an income-free area; above that, your pension reduces by 50 cents per dollar of income (singles) or 25 cents per dollar per person (couples). The Work Bonus adds an extra disregard for employment income only: the first $300 per fortnight of wages, salary or self-employment income (from active participation, such as hands-on work) is not counted. Passive self-employment, such as managing investments or a rental property, does not qualify. Deemed income, dividends, rent and other investment income do not get the Work Bonus. So if you are on a part pension and you take a part-time job, the first $300 per fortnight of that job is exempt from the income test.

Advanced Calculator: enter employment income to see Work Bonus and pension year by year

What Is the Work Bonus?

The Work Bonus is a rule that exempts a set amount of employment income from the Age Pension income test each fortnight. The exempt amount is $300 per fortnight (this rate has been in place since 1 July 2019). From January 2024, the income bank cap was made permanent at $11,800 and new pensioners can receive a starting credit of $4,000. So if you earn $300 or less per fortnight from work, that income is not assessed. If you earn more, only the amount above $300 per fortnight counts toward the income test for that fortnight. Employment income means wages, salary, commissions and income from self-employment where you are actively participating in the work (for example, bookkeeping or plumbing). It does not include passive self-employment such as managing an investment portfolio or an investment property. It also does not include deemed income on investments, dividends, rent, super pension payments or other non-employment income.

The Work Bonus Income Bank

If you do not use the full $300 in a fortnight, the unused amount can be added to a Work Bonus income bank. The bank has a maximum balance (currently $11,800). New pensioners can start with a starting balance (e.g. $4,000). When you have work income above $300 in a fortnight, you can use the bank to offset the extra so that more of your employment income is exempt. The bank carries forward until used. Rules and limits are set by the government and can change; check Services Australia for current figures.

Who Benefits?

Anyone on the Age Pension (or qualifying for it) who has employment income benefits from the Work Bonus. If you are on the full pension with very low income, the Work Bonus may not change your payment much. If you are on a part pension and the income test is the one that applies to you, earning up to $300 per fortnight from work (or more with the bank) can mean you keep more pension than you would without the Work Bonus. Couples each have their own Work Bonus. This is not advice about whether to work; it is an explanation of the rule. For advice tailored to your situation, contact Centrelink or a licensed financial adviser.

How It Fits With the Income Test

The income test has an income-free area (a threshold below which your pension is not reduced by income). The Work Bonus sits on top of that for employment income only. So a single pensioner with no other income could have the standard income-free area plus $300 per fortnight of work income exempt. Above the income-free area and the Work Bonus, the taper applies: 50 cents per dollar for singles, 25 cents per dollar per person for couples. The taper is the same whether the income is from work or from investments; only the Work Bonus exemption is for work.

Run Your Own Numbers

Pension and work income interact with your assets, other income and whether you are single or a couple. The Advanced Calculator lets you enter employment income and see your Age Pension and total income year by year, with the Work Bonus applied. We do not recommend that you open, close or change any super fund or product. This is general information only. For advice specific to your circumstances, see Services Australia or a licensed financial adviser.

See Work Income and Pension Together

Enter your situation and employment income in the Advanced Calculator. It applies the Work Bonus and shows your pension and total income year by year.

Open the Advanced CalculatorWhat it costs to keep modelling

Run Advanced Retirement free first. Unlimited scenarios, historical stress tests, and PDF exports are $149 a year, or $14.99 a month if you’d rather not commit upfront, typically less than one hour of paid advice for the same modelling work.

Run the Advanced Calculator →No card required to try it. Subscribe only if the model is useful enough to keep using.

Disclaimer: This article is general information only. It is not financial product advice or personal advice. SuperCalc Pro does not hold an Australian Financial Services Licence (AFSL). We do not recommend that you open, close, or change any super fund or product. Work Bonus rules and figures are set by the Australian Government and can change. For current rules and advice specific to your situation, see Services Australia or a licensed financial adviser.