Important: General information only, not financial product advice or personal advice. SuperCalc Pro does not hold an Australian Financial Services Licence (AFSL). This article does not recommend contributing, claiming deductions, or switching funds. Income thresholds are indexed and change over time; confirm the numbers for your financial year on the ATO website before acting.

If you earn modest wages and still put something extra into super, the tax system sometimes pays you back twice: once through the super co-contribution (a government top-up on personal after-tax contributions) and once through LISTO, the low income super tax offset (a refund of contributions tax on concessional amounts). Neither is automatic marketing from your fund. Both are calculated by the ATO after you meet eligibility tests and usually lodging a tax return.

They are easy to confuse because both help people on lower incomes. They are not the same payment. The co-contribution rewards non-concessional personal contributions. LISTO softens the 15% contributions tax on concessional money already in the fund (employer SG, salary sacrifice, or personal amounts you treat as concessional). This guide walks through each in plain language so you know what to check, not what product to buy.

How the co-contribution works

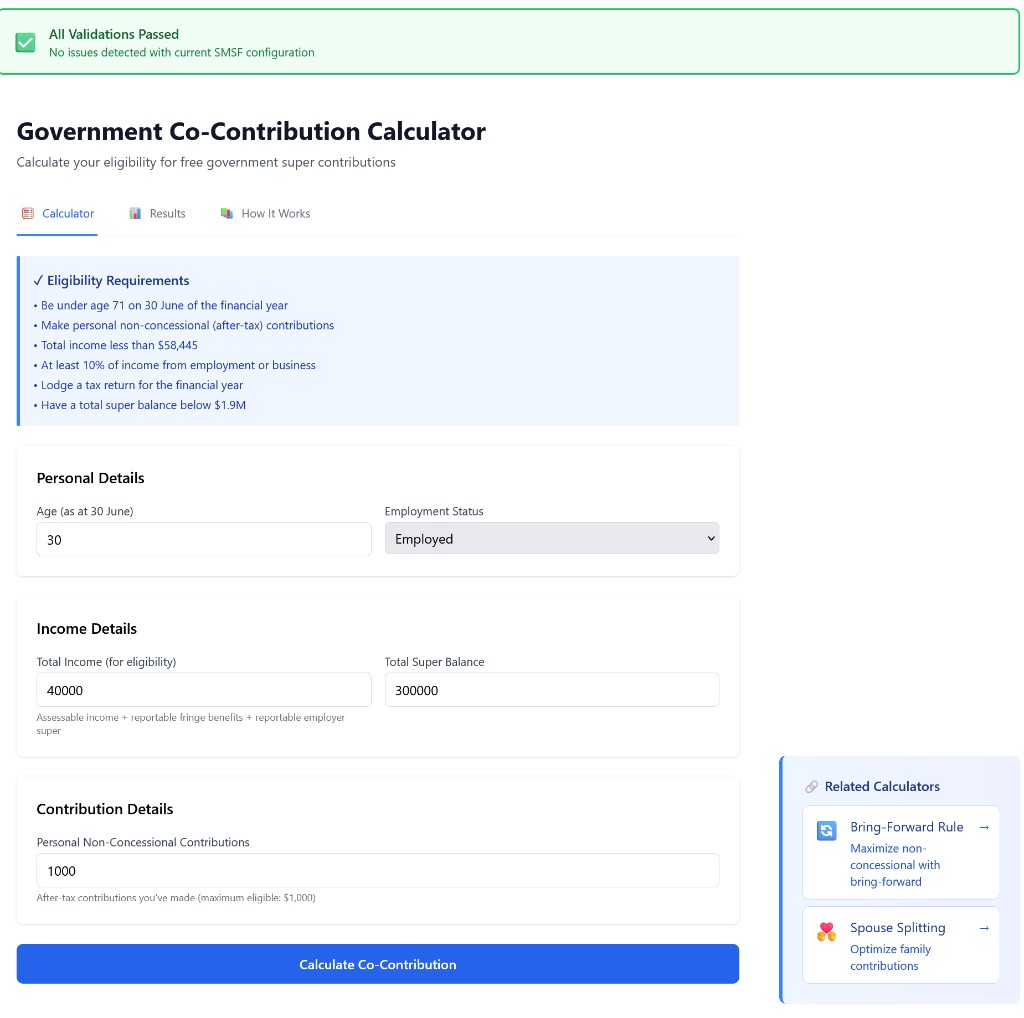

When you are eligible, the ATO pays 50 cents for every dollar of personal non-concessional contributions you make, up to a maximum government payment of $500 per financial year. In practice that means up to $1,000 of your own after-tax contributions can attract the full match if your income sits below the lower threshold, you are under 71 on 30 June, and every other test is satisfied. The matching rate is fixed at half of what you put in; the cap on the government side is what stops the payment at $500 even if you contribute more than $1,000.

For the 2025-26 financial year the ATO co-contribution income thresholds are $47,488 (lower) and $62,488 (upper). At or below $47,488 you can receive the maximum $500 match if other rules pass. Between those figures the maximum match tapers until it reaches zero at or above $62,488. Thresholds are indexed each year; check the ATO key super rates page if you are contributing in a different income year.

Co-contribution income is not just taxable salary. The ATO uses a total income style measure that includes assessable income, reportable fringe benefits, and reportable employer super contributions (RESC). A modest salary plus a large salary-sacrificed super package can push you above the threshold even when take-home pay feels tight. That is why people who consider themselves "not rich" still miss the co-contribution.

Only personal contributions you do not claim as a tax deduction count toward the match. Employer super guarantee, salary sacrifice, spouse contributions received, and downsizer amounts sit outside that line. If you give your fund a valid notice of intent and treat a personal contribution as concessional, that same dollars cannot also drive a co-contribution. The government payment still has to fit your wider contribution picture, including non-concessional caps and total super balance limits that can shut off after-tax contributions entirely.

Beyond income and contribution type, several administrative gates catch people who assumed the fund would "just know." At least 10% of your total income for the year must come from employment or carrying on a business. You normally need to lodge an income tax return for that year and have your tax file number on the account. Your total super balance on the prior 30 June must sit below the general transfer balance cap ($2.0 million for 2025-26, indexed) or you generally cannot make non-concessional contributions and the co-contribution path closes with them. Temporary residents generally do not qualify, so anyone on a visa should read the ATO residency guidance before counting on a match.

Illustrative shape only (not advice)

Suppose your total income for co-contribution purposes is $40,000, you are 42, you lodge a return, and you contribute $800 as a personal non-concessional contribution without claiming a deduction. If every test passes, the government match might be $400 (50% of $800), paid into your super after processing. If income were $55,000 (inside the 2025-26 taper band), the maximum possible match on $1,000 would be about $250, not the full $500, even before considering how much you actually contributed.

LISTO: contributions tax back for low incomes

LISTO (low income super tax offset) targets a different friction point. Concessional contributions generally suffer 15% tax in the fund on the way in. For very low earners that can be harsh compared with their marginal tax rate outside super. LISTO can refund up to $500 of that contributions tax per year by paying an offset amount into your super, usually after your tax return is processed.

Eligibility is driven by adjusted taxable income (not identical to the co-contribution income definition). For 2025-26, the ATO pays up to $500 LISTO when your adjusted taxable income is at or below $37,000; the offset tapers so that it is nil once income reaches $45,000. You must have concessional contributions in the fund for the year and meet lodgment, TFN, and residency tests similar to the co-contribution. Higher LISTO thresholds have been announced from 1 July 2027 but are not law for 2025-26.

Remember the split: LISTO needs concessional contributions in the account (SG counts). The co-contribution needs non-concessional personal contributions you do not deduct. A part-time worker might receive LISTO from employer SG alone while still needing a deliberate after-tax contribution to chase the co-contribution.

Can you get both?

Yes, in principle, if you satisfy both sets of rules in the same financial year. A common pattern for a low-income employee is employer SG (concessional) triggering LISTO, plus a small personal after-tax contribution triggering the co-contribution. The arithmetic is separate; the ATO does not net them against each other.

Planning mistakes run the other way too. Someone salary sacrifices heavily, receives LISTO on the concessional slice, but contributes nothing as non-concessional and wonders why the co-contribution never appears. Someone else makes a large personal contribution and claims it as a tax deduction, converting it to concessional, which can help LISTO logic but destroys co-contribution eligibility on that same dollars.

If your income is high enough that concessional stacking matters for tax rather than for LISTO, Division 293 sits in a different lane again. When income for surcharge purposes plus concessional contributions crosses the threshold the ATO applies for your year (often discussed around $250,000 combined for recent income years), an extra 15% tax can apply on part of your concessional amounts. The liability is raised through your personal tax return. You can pay it from personal cash, or you can ask the ATO to release the amount from super under the standard release authority, which can ease cash flow in the year of assessment but reduces capital inside the fund. Neither path changes whether you qualify for co-contribution or LISTO; it is simply a cash-flow and balance-sheet choice worth modelling before you commit to large sacrifice late in the year.

Illustrative co-contribution estimate in the SMSF Suite; confirm eligibility with the ATO.

How to check and what to do before 30 June

Start by estimating total income for co-contribution purposes, not just the figure on your payslip. Pull together assessable income, reportable fringe benefits, and RESC from payment summaries and payroll reports so you know whether you sit in the full match zone, the taper, or above the cut-off. In parallel, separate your concessional plan from any after-tax amount you want the ATO to match. If you intend to claim a deduction on a personal contribution, that amount is concessional and will not count toward the co-contribution.

Before you transfer money, confirm you still have non-concessional cap space given your total super balance on last 30 June. Funds have different processing cut-offs, so contributions that leave your bank in late June are not always received in time; earlier is safer when you are chasing a match. After 30 June the work shifts to lodgment: the ATO normally calculates co-contribution and LISTO entitlements once your tax return is in, and the payments show up in myGov and on the fund statement when processing finishes.

If you are also juggling concessional cap space, remember the headline concessional contributions cap for 2025-26 is $30,000 per person (employer SG, salary sacrifice, and personal deductible amounts all count toward that single pool). Employer SG from multiple jobs still aggregates, and unused concessional cap from earlier years may be available under carry-forward rules if you were eligible on prior 30 June dates. Read concessional cap basics and checking unused concessional cap in myGov before you stack strategies.

Where people stumble

The most expensive slip is treating a personal contribution as both deductible and co-contribution eligible. A valid notice of intent moves the money into the concessional bucket, which can interact with LISTO but kills the match on that same dollars. Another frequent miss is ignoring RESC in the income test: salary sacrifice never lands in your bank account, yet it still widens total income for co-contribution purposes.

A separate payroll trap catches people who only watch their payslip salary. Employer super guarantee is calculated on a defined earnings base. Some employers use ordinary time earnings; others apply SG to total remuneration under a packaged arrangement. Where sacrifice reduces the base used for SG, compulsory employer contributions can be lower than you expect even though the sacrificed amounts themselves are still concessional and still consume part of your $30,000 cap for 2025-26. Co-contribution and LISTO modelling that assumes a flat percentage of gross wages without reading the employment contract and payment summary can misstate how much concessional money actually hit the fund.

Funds rarely pre-approve co-contributions because they receive the government payment only after the ATO runs the numbers post-lodgment. Members who never lodge a return often wonder why neither LISTO nor a co-contribution appeared. Finally, LISTO is not the same as LITO (low income tax offset in your income tax return). One is super-specific; the other sits in personal tax. Confusing the two labels sends people hunting in the wrong place on myGov.

Model contributions against retirement income

Use the free cap optimizer for a quick concessional check, then stress-test decades of balance and pension outcomes in the Advanced Calculator.

Free cap optimizer Open Advanced CalculatorBottom line

The co-contribution is a matching payment on eligible personal after-tax super contributions, capped at $500 from the government when income and other tests line up. LISTO is a separate refund of up to $500 of contributions tax on concessional money for low adjusted taxable incomes. They answer different questions, use different income measures, and both lean on you lodging returns and reading myGov after the fact. Neither replaces advice on whether extra super fits your cash flow; they only explain what the ATO may pay if you already qualify.

Disclaimer: Legislation, thresholds, and ATO administration change. Examples are simplified. Nothing here is tax, legal, or financial product advice. Confirm eligibility with the ATO and a qualified professional.