A recontribution strategy is one of the more discussed technical moves in Australian retirement planning. At its core, you take money out of super (usually as a lump sum once you have met a condition of release) and contribute it back as a non-concessional (after-tax) amount. The balance may end up much the same in dollar terms, but the split between tax-free and taxable components inside the fund can shift. That shift matters for death benefits paid to adult children and other non-dependants, and sometimes for how people think about pension phase and long-term income. It does not create new money. It rearranges tax labels within super law.

Recontribution sits in the same neighbourhood as lump sum versus pension decisions and non-concessional contribution caps, but it is not the same as either. You need access to super, room under contribution caps, and often a specific reason to care about the tax-free proportion. This article explains what the strategy involves, why some households explore it, and where the rules stop you. It is general information only. It does not tell you to run a recontribution or that one would benefit you.

Tax-free and taxable components: why the label matters

Every super account holds a mix of tax-free and taxable components. The tax-free part generally comes from after-tax contributions and certain other amounts that were never taxed in the fund. The taxable part reflects employer contributions, salary sacrifice, and investment earnings that have been taxed at 15% inside super. Some accounts, particularly in public sector schemes such as PSS or CSS, also include an untaxed element where contributions were never taxed in the fund. Death benefits paid to non-dependants on the untaxed element are taxed differently (typically 30% plus Medicare Levy, not 17%). Recontribution logic described here applies to the standard taxed component; members with untaxed elements need fund-specific advice. Your member statement or fund portal may show the proportions, though not all members look at them until retirement or estate planning comes up.

While you are alive and drawing your own super from age 60, both components are generally tax-free in your hands on withdrawal, subject to current law. That general rule assumes a standard taxed accumulation or pension account. It does not apply in the same way to untaxed elements (see above), to withdrawals between preservation age and 59, or to certain defined benefit amounts that remain partly assessable. The distinction becomes sharper at death. A dependant beneficiary (typically a spouse, child under 18, someone financially dependent on the deceased, or someone in an interdependency relationship with the deceased) can usually receive a death benefit without the tax that applies to the taxable component of a lump sum paid to a non-dependant. For non-dependants, that tax is 17% on the taxable portion (15% tax plus 2% Medicare Levy). Adult children who are not financially dependent are the classic non-dependant case. On a large balance with a small tax-free proportion, that 17% can mean a substantial tax bill for the estate. Recontribution is one way some people try to increase the tax-free share before death, within the rules.

You cannot withdraw only the taxable portion from an accumulation account. Withdrawals are paid in the same proportions as the account's tax components. If your balance is 70% taxable and 30% tax-free, a $100,000 lump sum contains $70,000 taxable and $30,000 tax-free in the eyes of the tax system. When you re-contribute that $100,000 as a non-concessional contribution, the full amount is added to the tax-free component. Repeat the cycle within cap limits and the tax-free proportion rises over time.

What a recontribution cycle looks like

Suppose you are 65, have met a condition of release, and hold $800,000 in super with a 60% taxable / 40% tax-free split. You withdraw $120,000 as a lump sum. From age 60 that withdrawal is generally tax-free in your hands on a standard taxed account (not an untaxed public sector balance). The $120,000 leaving the fund contained $72,000 taxable and $48,000 tax-free in proportion to the account. You then contribute $120,000 back as a non-concessional contribution in the same financial year (if cap space allows). The re-contributed amount is entirely tax-free component. Your total balance is still about $800,000 before fees and market movement. The tax-free share rises from $320,000 (40%) to $392,000 (49%) in one cycle: the account started with $320,000 tax-free, lost $48,000 of that on withdrawal, then gained $120,000 back as tax-free contribution. On those numbers, a non-dependant beneficiary's death benefit tax on the amount replaced could fall by about $12,240 (17% of the $72,000 taxable component that left the fund and was replaced by tax-free contribution), before fees, advice costs, and Centrelink effects. That is a meaningful shift for estate planning, though repeating it depends on cap room and whether the effort justifies the saving for your beneficiaries.

In practice the steps involve paperwork and timing. You request a withdrawal from your fund, receive cash (often within days to weeks), then lodge a non-concessional contribution form and transfer from your bank account. For most industry and retail funds, the money must leave super as cash and return as a cash contribution. In-specie transfers are generally an SMSF-only option in limited circumstances, not something most members can use to shortcut the process. If the cash sits in a bank account between steps, it may count as a financial asset for Centrelink deeming and the assets test until it re-enters super. That gap matters for Age Pension age households even if the strategy is tax-neutral inside super.

People in pension phase face an extra layer. You cannot usually recontribute directly from an account-based pension without first commuting part or all of the pension to accumulation, or taking a lump sum withdrawal. Commutations debit your transfer balance account and do not restore transfer balance cap space you have already used. Minimum drawdown rules still apply for the year. Starting or restarting pension phase after recontribution is subject to whatever unused cap space you still have within your personal transfer balance cap, not a fresh general cap. Pension-phase recontribution is possible for some balances but the cap arithmetic is unforgiving. Confirm with your fund, the ATO, and a licensed adviser before relying on a sequence.

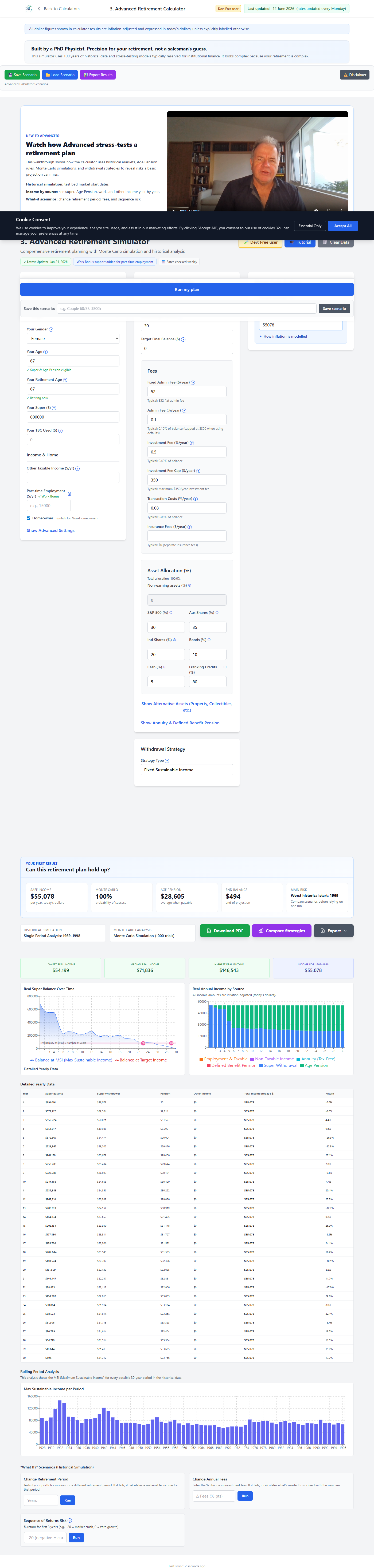

Advanced Calculator example: single retiree age 67 with $800,000 super and a fixed real income strategy. Lowest real income $54,199/year, median $71,836/year, highest $146,543/year across historical simulations; the selected 1969–1998 period shows $55,078/year. Charts below show year-by-year super balance and income from drawdown plus Age Pension. The calculator does not model tax-free vs taxable components.

Contribution caps and eligibility gates

Recontribution only works if you can legally put the money back in. Non-concessional contributions are capped at $120,000 per financial year for 2025-26 (indexed in future years). Members who were under 75 on 1 July of the financial year in which they trigger it can use the bring-forward rule to contribute more than one annual cap in a single year, up to three years of caps ($360,000 at current rates when fully available), which triggers a multi-year cap lock-in. Bring-forward is not all-or-nothing at the $2 million TSB cutoff. For 2025-26, the ATO published bring-forward table (based on TSB at the prior 30 June) is: at or above $2 million, no non-concessional cap; $1.88 million to $1.999 million, only the annual $120,000 with no bring-forward; $1.76 million to $1.879 million, up to two years ($240,000); below $1.76 million, up to three years ($360,000). Thresholds change each financial year as caps and the general transfer balance cap index. A member with TSB of $1.9 million might read "$360,000 bring-forward" elsewhere and over-contribute. Check your available cap in ATO online services before relying on any headline figure.

Your total super balance (TSB) on 30 June of the previous financial year is the other major gate. If your TSB was at or above the general transfer balance cap (currently $2 million for 2025-26, rising to $2.1 million from 1 July 2026), your non-concessional cap for the year is zero. You cannot recontribute no matter how much you withdrew. This test compares TSB to the general cap, not your personal transfer balance cap, which may be lower if you started a retirement income stream before full indexation applied. A personal cap of, say, $1.9 million does not restore NCC room if your TSB still exceeds the general cap. Check both figures in ATO online services. TSB includes accumulation and pension balances across all funds. A withdrawal lowers TSB temporarily, but the test for this year's cap was set last 30 June. Planning often spans multiple financial years so that a withdrawal in one year creates cap room in the next, but that requires careful sequencing and is easy to get wrong.

Contribution age rules also apply. Non-concessional contributions can generally be made until you turn 75. If you turn 75 during a financial year, the fund must receive any final contribution within 28 days after the end of the month in which you turn 75. That is a cut-off for your birthday year, not a standing grace period that applies every year. The work test for non-concessional contributions between 67 and 74 was removed from 1 July 2022. A work test still applies if you want to claim a personal tax deduction for concessional contributions in that age band. That change removed one barrier to recontribution for retirees aged 67 to 74, but caps and TSB tests still bind. Excess non-concessional contributions attract tax and administrative pain. The ATO can release excess amounts in some cases, but prevention is cheaper than cure.

Who might explore the idea (and who usually does not)

Recontribution strategies appear most often in conversations about estate planning where adult non-dependant beneficiaries are likely. If the intended recipients would pay 17% (15% plus Medicare Levy) on a large taxable component at death, shifting part of the balance to tax-free can reduce that bill. The benefit must be weighed against years of effort, cap limits, advice fees, and the possibility that law or beneficiary circumstances change. See binding death benefit nominations for how nominations interact with who receives benefits, though nominations do not change the tax components themselves.

Some people approaching pension phase with a high taxable proportion consider recontribution while still in accumulation, before starting an account-based pension, to begin retirement with a higher tax-free share in the income stream. The income tax on pension payments to the member is generally nil from age 60 regardless of components, so the live member benefit is often smaller than the estate benefit unless other factors apply. Recontribution also does not reduce exposure to Division 296, the additional tax on super earnings for balances above the large super balance threshold, set at $3 million for 2026-27. Better Targeted Super Concessions is now law (royal assent March 2026) and applies from 1 July 2026. Check the ATO website for current guidance on how Division 296 is calculated and reported. Either way, recontribution changes tax component labels inside the same dollar balance; it does not lower total super balance for a Division 296 test.

Households with modest balances, dependant-only beneficiaries, or TSB already near the cap often gain little from the exercise. The transaction costs, Centrelink exposure during the cash gap, and cap complexity may outweigh a small shift in tax components. People who need every dollar for living expenses should not treat super as an estate-planning workshop. Liquidity and sustainability come first.

Centrelink and the cash-in-the-middle problem

Tax law and social security law diverge again. Super in accumulation phase is generally not counted under the Age Pension assets test until you reach Age Pension age, but once you withdraw a lump sum the cash usually becomes an assessable financial asset. It is also subject to deeming under the income test: Centrelink applies a set deemed rate to financial assets, not your actual bank interest. When deeming rates sit below typical savings account rates, as they often do in the current environment, the income test may count less than the interest you actually receive during a brief cash gap. Deeming rates change with policy and may not match market returns. If you recontribute quickly, the assessable amount may be brief. If the process straddles a Centrelink reporting period or you hold cash for months, pension entitlements can change until Services Australia reassesses your household's circumstances and what else has changed in the meantime.

Money that returns to super in accumulation before Age Pension age may again fall outside the assets test until you reach that age. Money in pension phase is assessed differently. Couples where one partner has reached Age Pension age and the other has not add another layer: Services Australia assesses the household as a whole. Super in accumulation for the younger partner may stay outside the assets test until they reach Age Pension age, but cash withdrawn and held during a recontribution can still affect the older partner's entitlement while it sits outside super. Mixed-age couples need to model the household impact, not only the member running the strategy. None of this makes recontribution automatically bad for Centrelink purposes, but it means the strategy is not purely a tax-component exercise. Always confirm treatment with Services Australia or a licensed adviser for your household before acting.

Common traps and misconceptions

The first trap is assuming recontribution creates extra super or reduces tax on your own living income after 60. For most retirees drawing their own benefits, it does neither. The payoff, when there is one, is often downstream for non-dependant beneficiaries or in specific cap-management scenarios.

The second trap is cap breaches. Triggering the bring-forward rule without a multi-year plan, or recontributing after a TSB test has zeroed your cap, leads to excess contributions tax and ATO correspondence. Third, market timing: withdrawing before a market recovery and recontributing after prices rise changes your economic outcome even if tax components improve. Fourth, insurance: group cover linked to super can lapse if a partial withdrawal drives the balance below the fund's minimum account threshold (often $6,000 to $10,000, varying by fund) or if the account is closed. A partial withdrawal from a large balance usually poses no insurance risk. Fifth, anti-avoidance: schemes that exist only to manipulate components without genuine contribution intent can attract ATO scrutiny under Part IVA. Document a legitimate contribution and keep records. The ATO has historically indicated that genuine recontribution arrangements are unlikely to attract Part IVA scrutiny, but there is no current binding ruling and contrived or excessively aggressive arrangements remain at risk. Check current ATO material or seek advice before relying on any comfort.

A persistent myth is that you can "strip" taxable component by partial withdrawal alone. You cannot. Only the recontribution leg adds 100% tax-free amounts. Another myth is that recontribution restores transfer balance cap space after commuting a pension. It does not. Commutations reduce the running balance in your transfer balance account. If you have not previously used your full personal cap, that reduction creates room to restart pension up to your remaining cap, but your cap ceiling itself is unchanged and your cap history is not reset.

How to sense-check your own position

Start with facts from your fund: current balance, tax-free and taxable proportions, and whether you are in accumulation or pension phase. Confirm the fund accepts non-concessional contributions, its forms and processing times, and any product-level limits that sit on top of the legislative caps. Check your TSB on myGov or ATO online services and your available non-concessional cap. Map intended beneficiaries and whether they would be dependants or non-dependants for death benefit tax. If the taxable component is small or beneficiaries are dependants, recontribution may be a solution looking for a problem.

If the numbers suggest a possible benefit, model the multi-year cap path (single year $120,000 versus bring-forward $360,000) and the Centrelink impact of holding cash between steps. The Advanced Calculator can help with sustainable income and balance trajectory after large in-and-out movements, though it will not replace component accounting from your fund or the ATO. For component splits and death benefit tax, a licensed adviser or tax agent familiar with super law is the appropriate next step.

Model balance and income after a capital event

See how a withdrawal or recontribution within your caps might fit into long-run retirement drawdown and Age Pension scenarios.

Open the Advanced CalculatorDisclaimer: This article is general information only. It is not financial product advice or personal advice. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). We do not recommend that you open, close, or change any super fund or product, or that you undertake a recontribution strategy. Tax rules, contribution caps, total super balance tests, transfer balance cap rules, death benefit tax, and Centrelink treatment can change. For advice tailored to your situation, see the ATO, your super fund, Services Australia, or a licensed financial adviser, SMSF specialist, or tax agent.