When Australians reach preservation age and meet a condition of release, they face a structural choice that is easy to gloss over. You can withdraw part or all of your super as a lump sum, move some or all of it into an account-based pension (also called an allocated pension or income stream), or combine both over time. The question is not only how much tax you pay on the way out. It is what happens to the money afterwards, how Centrelink treats it, and whether the balance can support decades of spending.

Many retirees assume the decision is binary because they have heard that pension phase is tax-free. That is partly true, but incomplete. From age 60, lump sum payments and pension payments from super are generally tax-free in your hands, subject to the tax-free and taxable components of your account. The meaningful differences sit in earnings tax inside super, the transfer balance cap, minimum drawdown rules, and how Services Australia assesses what you hold once money leaves the super system. Keep the current super and Age Pension thresholds beside the calculator while comparing paths. This article outlines the trade-offs in plain language. It does not tell you which option to choose.

What each path means in practice

A lump sum withdrawal takes money out of super entirely (or reduces your accumulation balance to zero if you withdraw everything). The cash lands in your bank account or wherever you direct it. You can spend it, invest it outside super, pay down debt, or gift it subject to Centrelink rules. Super's tax concessions on investment earnings no longer apply to that portion. Any future income or capital gains on those investments follow normal personal tax rules.

An account-based pension keeps the money inside super in retirement phase. You receive regular payments (or ad-hoc payments within product rules) while the remaining balance stays invested. Investment earnings on assets supporting the pension are taxed at 0% up to your transfer balance cap. You must withdraw at least the legislated minimum drawdown each year, but you can usually take more if you need it. You can also take partial lump sums, called commutations, while leaving the rest in pension phase.

The third path, which many people actually use, is a hybrid. Start a pension for ongoing income, commute a portion for a specific purpose such as clearing a mortgage, and leave any amount above the transfer balance cap in accumulation phase (where earnings are taxed at 15%). The hybrid is not a compromise for indecisive retirees. It reflects the fact that super law treats lump sums and pensions as different events with different downstream effects.

Tax on the way out: often similar from age 60

For most people aged 60 or over, the headline tax rate on super withdrawals is the same whether the money leaves as a lump sum or a pension payment: generally nil on amounts that would otherwise be taxable in your hands. The tax-free component of your balance is always tax-free. The taxed component is also tax-free from age 60 for both lump sums and income streams under current law.

Below age 60 the picture changes. Lump sums from the taxable component are assessable at your marginal tax rate, with a 15% tax offset available on amounts within the lifetime low-rate cap (currently $235,000 for 2025-26, indexed over time). Amounts above that cap are taxed at your marginal rate without the offset. Pension payments between preservation age and 59 also attract tax but may include the same offset on the taxable portion. If you are retiring before 60, the lump sum versus pension comparison needs to include your marginal rate and how much of the balance is tax-free versus taxable. Confirm current thresholds with the ATO or a licensed adviser.

Where pension phase pulls ahead for many retirees is not the withdrawal tax rate but earnings tax inside super. In accumulation phase, fund earnings are taxed at 15%. In retirement phase, earnings on assets supporting an account-based pension are taxed at 0%, subject to the transfer balance cap. Take a full lump sum and invest it in a term deposit or share portfolio, and the income and gains are taxed at your personal rates. Leave the same balance in pension phase and the compounding happens in a tax-free environment. Over twenty or thirty years that gap can be large, which is why the choice is rarely only about this year's tax bill.

Transfer balance cap: pension phase has a ceiling

Not all of your super can sit in tax-free pension phase. The transfer balance cap (TBC) limits the amount you can move into retirement phase. The ATO sets a general TBC that is indexed over time. For 2025-26 it is $2 million; from 1 July 2026 it rises to $2.1 million. What actually limits you is your personal TBC, which may equal the general cap if you have never started a retirement-phase income stream, or may be lower if you have previously used cap space. Your personal cap depends on when you first entered retirement phase and how indexation applied to your account. Amounts above your available cap generally remain in accumulation phase, where earnings continue to be taxed at 15%, or you can withdraw them as lump sums.

Starting a pension creates a credit in your transfer balance account (TBA) equal to the value moved into retirement phase. That credit counts against your personal TBC. A partial commutation (lump sum from the pension) debits your TBA, so your current transfer balance falls. That does not increase your personal TBC. What it can do is create headroom within your existing personal cap: available cap space is generally your personal TBC minus your current TBA balance, which you can view in ATO online services. If a commutation brings your TBA below your personal TBC, you may be able to move further amounts into retirement phase up to that limit, subject to product rules and having accumulation balance available.

A full commutation closes the pension and records a debit in your TBA. Starting a new account-based pension later is generally possible only within whatever cap space that leaves, not as a fresh start at the full general cap. Do not confuse this with a pension account that has simply fallen in value because of investment losses. Market declines do not debit your TBA, and the ATO's investment earnings example on transfer balance accounts shows you cannot top up a pension from accumulation if you have already used all your personal cap space, even when the account balance has fallen. Commutations and investment losses are treated differently.

Your highest-ever TBA balance is also tracked separately. It affects proportional indexation of your personal TBC when the general cap rises, not your current available cap space in the same way. Someone who previously transferred close to their personal cap at commencement may receive little or no future indexation even after commuting, because indexation is based on unused cap percentage measured at that highest-ever point. Commuting can restore room to transfer within your existing personal cap; it does not rewrite that indexation history. See the ATO transfer balance account guidance or a licensed adviser for your personal TBC, TBA, and available cap space.

People with balances well below the cap rarely think about this limit until a spouse dies or a reversionary pension transfers. For larger balances, the hybrid structure is common: pension up to available cap space for tax-free earnings, accumulation or lump sum for the remainder. That is a tax and product design issue, not a moral verdict on lump sums.

Centrelink and the Age Pension

Tax law and social security law do not mirror each other. Something that is tax-efficient in super can still reduce your Age Pension, and vice versa.

Superannuation in accumulation phase is generally not counted under the Age Pension assets test until you reach Age Pension age. The income from that accumulation balance is also not assessed under deeming until you reach Age Pension age. That can matter if you retire at 62 and leave super in accumulation for several years before the pension tests apply. Once you withdraw a lump sum, the cash and most investments you buy with it become assessable assets. They also feed into the deeming rules for the income test: Centrelink assumes financial assets earn a set rate regardless of what they actually earn. A large lump sum sitting in cash or shares can therefore reduce pension entitlements through both tests, depending on which test binds for your household.

An account-based pension is treated differently from both accumulation super and cash held outside super. For people of Age Pension age, the pension account is usually an assessable asset under the assets test. Under the income test, Services Australia applies a deductible amount to each payment. That deductible amount represents the return-of-capital portion of the payment and reduces the income counted from the stream. It is not the same as asset-test exempt (ATE) income stream treatment, which applies to certain lifetime, life-expectancy, and defined benefit pensions under specific rules, not to standard account-based pensions. Do not assume an account-based pension receives ATE treatment. The net Age Pension outcome depends on your balance, payment rate, age, and which test binds for your household. Rules change; confirm with Services Australia or a licensed adviser.

If you are years away from Age Pension age, Centrelink may still matter for a partner who is already eligible. Household income and assets are combined. A younger retiree who commutes super to cash and holds it in joint names can affect a partner's pension even when the younger person's super would not yet be asset-tested. See income test vs assets test for how the two tests interact. Always confirm treatment with Services Australia or a licensed adviser before relying on a strategy.

Sustainability: lump sums spend differently from pensions

Behavioural research consistently finds that people treat lump sums and streams differently. A single large payment feels like wealth. A monthly pension payment feels like income. Retirees who take everything as cash at once often spend faster than they expected, or sit on the money in low-return deposits because they fear running out. Neither outcome is guaranteed, but the pattern is common enough that advisers discuss "mental accounting" in retirement planning.

From a pure numbers perspective, drawing super down as a controlled income stream maps more cleanly to long-term planning. You set a withdrawal strategy (fixed dollar, percentage of balance, or one of the dynamic rules discussed in drawdown strategies), test it against bad market sequences, and adjust when minimum drawdown rules force higher payments in later decades. A full lump sum at retirement removes the guardrails. You can still budget carefully, but nothing in the product structure requires you to pace withdrawals across thirty years.

That said, a lump sum is not automatically reckless. Some retirees have a defined need for a block of capital: clearing a mortgage before Age Pension age, funding a renovation that lets them stay at home, or bridging a gap until other income starts. The question is whether the purpose justifies removing that capital from super's tax-free earnings environment and whether the remaining balance, if any, is still large enough to fund the years ahead.

When a lump sum is commonly considered

General information sources often mention lump sums in a few recurring scenarios. Paying off debt with a high interest rate can improve cash flow and reduce stress, though the comparison needs to include lost investment returns inside super and any Centrelink impact of holding less debt but more assessable assets elsewhere. Major one-off expenses, such as replacing a car or paying for aged care deposits, may be easier to fund from a commutation than from trying to match a large bill to regular pension payments.

Estate planning sometimes favours keeping a pension with a reversionary nomination for a spouse while commuting only what the household needs in cash. Death benefit tax for non-dependants can also differ between lump sum and pension pathways, though that is a separate topic covered in death benefit and BDBN articles. None of these scenarios produces a universal answer. They are reasons people compare the paths, not instructions to take one or the other.

When pension phase is commonly considered

Retirees who want super earnings to compound tax-free, who need predictable income over decades, or who expect to rely partly on the Age Pension often lean toward keeping the bulk of super in pension phase. The account-based pension product is flexible: you can change payment amounts within product rules, take ad-hoc commutations when needed, and leave a reversionary income stream for a partner. Minimum drawdowns rise with age, which pushes cash flow up in later years when health costs often increase, whether or not that timing suits your spending preferences.

Pension phase also keeps money inside a regulated super environment with consumer protections, insurance options, and consolidated reporting. That administrative shell matters less to some self-directed investors who would prefer to manage a share portfolio directly, and more to people who want simplicity. Again, the trade-off is personal and situational.

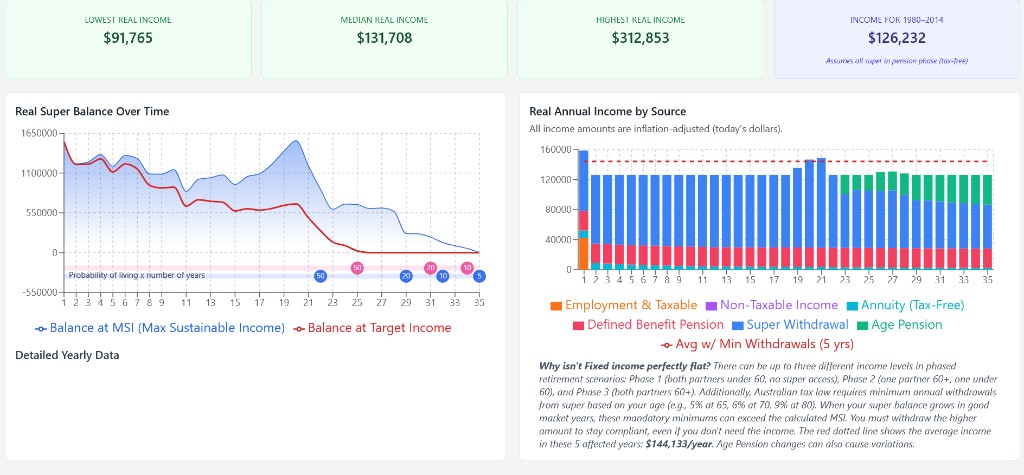

Advanced Calculator example: age 67, $800k super, fixed real income target with minimum drawdown rules applied. The chart shows how a pension-style drawdown paces super withdrawals over retirement rather than exhausting the balance in early years.

How to compare your own numbers

A useful comparison starts with three parallel pictures. First, tax: marginal rate on withdrawals if under 60, earnings tax inside super versus outside for the portion you might commute. Second, Centrelink: model household assets and deemed income with a full commutation versus an account-based pension at Age Pension age. Third, sustainability: run the same spending target through historical or Monte Carlo simulations with a pension drawdown path and with an early lump sum that shrinks the investable balance.

Many people discover that the tax saving from pension phase is modest in the first five years but compounds meaningfully over twenty. Others find that clearing a mortgage with a lump sum improves net cash flow enough to offset the lost super earnings. The Advanced Calculator and related tools are built for that kind of scenario testing, not for producing a single "correct" product choice.

Compare pension drawdown with your balance

See year-by-year income, balance, and Age Pension interactions when super stays in a drawdown strategy instead of leaving as a single lump sum.

Open the Advanced CalculatorDisclaimer: This article is general information only. It is not financial product advice or personal advice. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). We do not recommend that you open, close, or change any super fund or product, or that you take a lump sum rather than a pension or vice versa. Tax rules, transfer balance cap amounts, Centrelink treatment, and pension product terms can change. For advice tailored to your situation, see the ATO, your super fund, Services Australia, or a licensed financial adviser.