If you have moved part or all of your super into retirement phase as an account-based pension (also called an allocated pension), you cannot simply leave the balance untouched forever. The rules require a minimum drawdown each financial year: a percentage of your account balance that must be paid out to you. The percentage depends on your age. This article explains the usual age brackets, why the rules exist, and how they interact with preservation age and long-term income planning. It is general information only, not personal advice. Rates and rules are set in tax law and can change; confirm current figures with the ATO, your fund, or a licensed adviser.

Minimum drawdown is a floor, not a ceiling

The percentages below are minimums. You must take at least that much (subject to how your fund calculates the dollar amount), but you may take more if you need the cash or your strategy assumes higher spending. Many retirees discuss this alongside the transfer balance cap and how much sits in pension phase versus other structures.

Standard age brackets (indicative)

The table below shows the commonly quoted minimum drawdown percentages used for account-based pensions. For an ongoing pension, your age on 1 July determines the percentage for that whole financial year. In the first year a pension starts, your age on the commencement date is used instead, and the dollar minimum is usually pro-rated for the part of the year the pension is in place. Funds publish the exact dollar minimum based on your reported balance.

| Age (typical brackets) | Minimum drawdown (% of balance) |

|---|---|

| Under 65 | 4% |

| 65 to 74 | 5% |

| 75 to 79 | 6% |

| 80 to 84 | 7% |

| 85 to 89 | 9% |

| 90 to 94 | 11% |

| 95 or more | 14% |

From time to time, the government has temporarily reduced these percentages (for example, during COVID-19). Always use the percentage that applies for the current financial year. The ATO and your fund’s website list the official rates.

How the dollar amount is worked out

Your fund applies the relevant percentage to your account balance at a date set out in the product rules, usually 1 July each year for ongoing pensions. If you start a pension part-way through the year, the minimum for that first year is often pro-rated based on how many days the pension was in place. If you take more than the minimum in a year, the extra does not change next year’s minimum percentage, but it does reduce the balance that the next 1 July percentage applies to.

One practical trap is that not every movement out of the pension account necessarily counts as a pension payment for minimum drawdown purposes. A partial commutation treated as a lump sum may not satisfy the annual minimum pension payment requirement. That is a paperwork and classification issue to check with the fund before relying on a withdrawal to meet the minimum.

Why this matters for retirement planning

Unlike a simple “4% rule” story from overseas, Australian retirees in pension phase must plan for a rising minimum percentage as they age. By the time you reach your late 80s and 90s, the required percentage is much higher. That can push cash flows up even if you would prefer to spend less, unless other strategies apply (which depend on your circumstances and are not covered here as advice). Many people model this alongside other income streams and Age Pension outcomes.

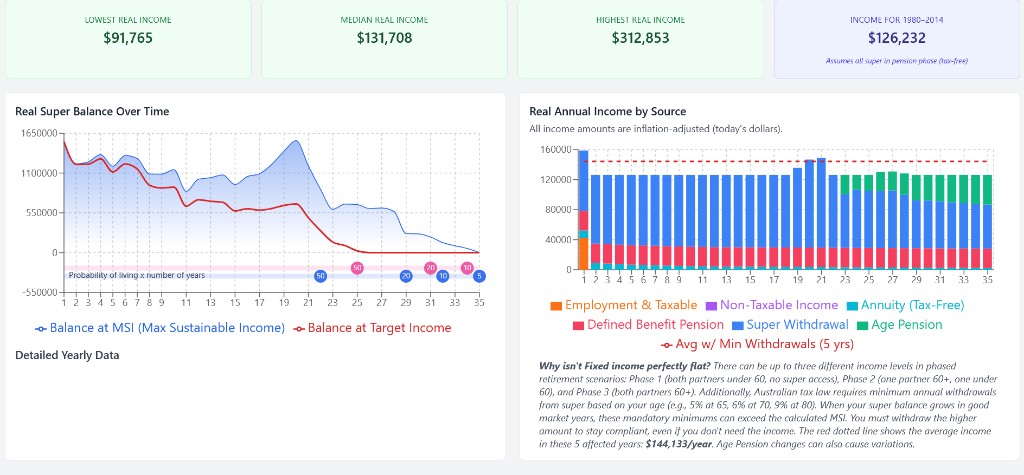

Advanced Calculator example: the red dotted line shows extra withdrawals from super when minimum drawdown rules require more than the calculated income plan.

Transition to retirement (different rules)

If you are still working and have a transition to retirement (TTR) pension, you usually face both a minimum and a maximum withdrawal each year. The age table for full retirement-phase pensions does not apply in the same way. Once you fully retire or reach 65 (subject to current law), your arrangement may move to a standard account-based pension and the percentages in the table above typically apply. Product disclosure statements and your adviser can clarify your fund’s terms.

Model minimum drawdown with your balance

See year-by-year balance, income, and Age Pension interactions with the percentages that apply to your age.

Open the Advanced CalculatorDisclaimer: This article is general information only. It is not financial product advice or personal advice. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). We do not recommend that you open, close, or change any super fund or product. Minimum drawdown percentages, tax rules, and pension settings can change. For current rates and advice tailored to your situation, see the ATO, your super fund, or a licensed financial adviser.