Most trustees treat their SMSF investment strategy like a terms-and-conditions checkbox. Download a template, plug in some broad percentages, file it away until audit time.

That approach will get you into trouble. If your strategy says you're a conservative investor and your portfolio is 100% speculative tech stocks, you're not just making a bad bet, you're in breach of the law. The auditor sees that mismatch. The ATO sees it. And the penalties for non-compliance are serious.

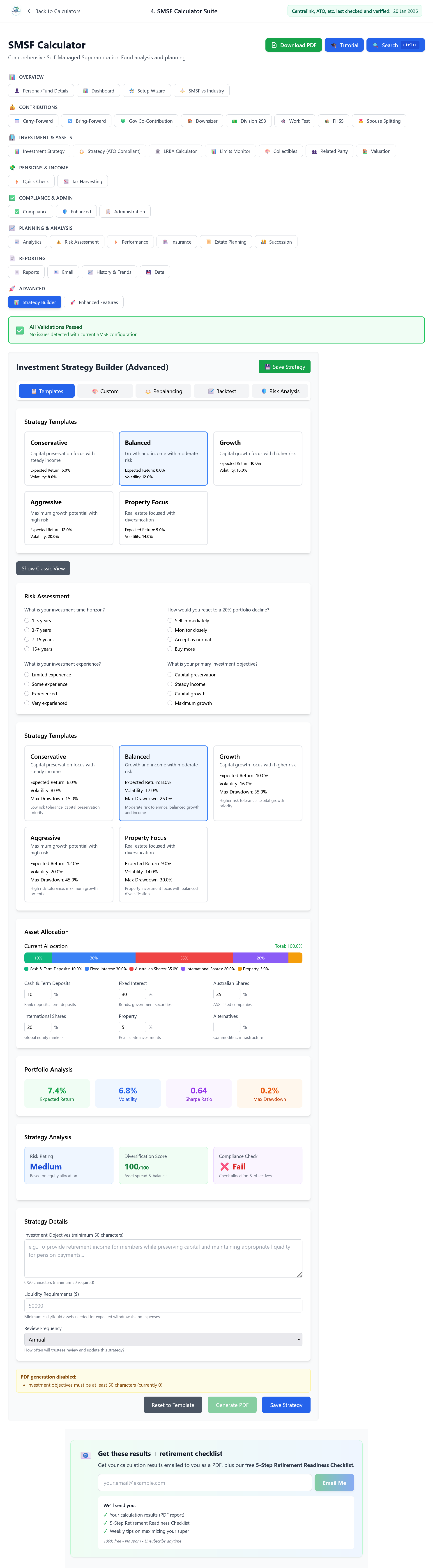

The Five Areas You Must Address

Regulation 4.09 of the SIS Regulations spells it out. Your strategy has to cover five areas. Skip one because you think it doesn't apply, and you've already failed the compliance test.

1. Risk and Return

You can't just say "we want to make money." You need to document the risk-return trade-off for your fund. Why is this asset mix appropriate for your members' ages and retirement objectives? What volatility are you prepared to accept? If you're 64 and 100% in crypto, you need a clear explanation of how that aligns with your goals. The auditor will ask.

2. Diversification

You don't have to be diversified. You can legitimately hold 100% of your fund in a single commercial property. But you must demonstrate that you considered the risks of concentration. If you're undiversified, your strategy needs to explain why that's appropriate and how you'll manage risk if that market turns.

3. Liquidity

Can the fund meet its obligations? This is the trap for property-heavy funds. If you own a $2M warehouse and have $5,000 in cash, how are you paying the auditor? The annual return? Pension payments? Your strategy has to spell out how you'll meet ongoing expenses and liabilities.

4. Ability to Pay Benefits

What happens when a member wants to roll out, or passes away? If your assets are tied up in illiquid investments, can you pay a death benefit or rollover without a fire sale? You need to document how you'll meet these prospective liabilities.

5. Insurance

You're not required to hold insurance inside the fund. You are required to consider it, and document that consideration. "We have cover elsewhere" is a valid reason. "We didn't think about it" is not. Your trustee minutes should reflect an annual review of insurance for each member.

The Auditor's Trap: A mismatch between your strategy and your actual holdings is one of the most common audit findings. If your strategy says "0–20% property" and you buy a house, you're in breach the day the contract settles. Update the strategy before you buy, not after.

Use Ranges, Not Fixed Percentages

Fixed targets like "50% Australian equities" create compliance headaches. Markets move. After a good month you might be at 52%. Technically you're outside your own rules.

Use ranges instead. "Australian equities: 40% to 60%." That gives you room to let winners run without rewriting the strategy every time the market shifts.

When to Update

Review your strategy at least annually, ideally when you prepare the year-end financials. But update it whenever something material changes:

- A member joins or leaves the fund.

- A member starts a pension (liquidity needs just changed).

- You shift from shares into property, or the reverse.

- A major market event changes your risk tolerance.

The Test: If an ATO officer read your strategy, would they understand why you own what you own? Would it tell the story of your fund? If not, you're leaving yourself exposed.

Run your own numbers

Use SuperCalc Pro to test your retirement plan with Australian super, Age Pension rules, and historical market stress tests.

Open Advanced Retirement Calculator