Every 1 July the Australian financial year turns over. For 2026-27 the headline is indexation: after AWOTE and CPI releases in early 2026, the ATO published higher contribution caps and a higher general transfer balance cap. Those numbers matter if you are salary sacrificing, making after-tax contributions, or moving into pension phase. They sit alongside a separate change called Payday Super, which alters when employers must pay Super Guarantee, not how much.

The indexed caps connect directly to topics many households already track: the concessional contributions cap, the non-concessional bring-forward rule, and total super balance tests at 30 June. This article walks through what rises from 1 July 2026, what stays flat, and where the calendar trips people up. It is general information only. It does not tell you to contribute, start a pension, or change funds.

Indexed caps at a glance

Most of the movement from 1 July 2026 is mechanical indexation. The concessional cap rises from $30,000 to $32,500. The non-concessional cap, which is set at four times the concessional cap, rises from $120,000 to $130,000. A full three-year bring-forward therefore moves from $360,000 to $390,000 for members who qualify. The general transfer balance cap increases from $2 million to $2.1 million, which in turn lifts the total super balance cut-offs that govern after-tax contributions. Smaller indexed amounts include the defined benefit income cap, up to $131,250, and the small business CGT cap, up to $1,935,000.

The table below summarises the main thresholds. Use it as a reference point, then confirm your own caps in ATO online services or with a licensed adviser because eligibility depends on age, work status, and total super balance on 30 June.

| Measure | 2025-26 | From 1 July 2026 |

|---|---|---|

| Concessional contributions cap | $30,000 | $32,500 |

| Non-concessional cap (annual) | $120,000 | $130,000 |

| Bring-forward maximum (3 years) | $360,000 | $390,000 |

| General transfer balance cap | $2,000,000 | $2,100,000 |

| Defined benefit income cap | $125,000 | $131,250 |

| CGT cap (small business) | $1,865,000 | $1,935,000 |

| Super Guarantee rate | 12% | 12% (unchanged) |

| Division 293 income threshold | $250,000 | $250,000 (unchanged) |

Sources: ATO contributions caps and ATO transfer balance cap tables updated for 2026-27.

Concessional contributions: $32,500

Employer Super Guarantee, salary sacrifice, and personal deductible contributions all count toward the concessional cap. The $2,500 step-up reflects AWOTE indexation in $2,500 increments. If your total super balance was under $500,000 at 30 June 2026, you may still have unused concessional cap space from up to five prior years under the carry-forward rules, provided you were eligible in those years.

Division 293 still adds an extra 15% tax on concessional contributions when income for surcharge purposes exceeds $250,000. That threshold does not index on 1 July 2026. High-income earners planning large salary sacrifice packages should check both the cap and the surcharge, not only the headline $32,500 figure.

Non-concessional contributions and bring-forward

After-tax contributions face a harder gate than the annual cap suggests. If your total super balance at 30 June 2026 was at or above the general transfer balance cap of $2.1 million, your non-concessional cap for 2026-27 is zero, even if your personal transfer balance cap is lower because you started a pension in an earlier year when the general cap was smaller.

Below that line, bring-forward rules scale how much you can contribute in one hit. With TSB under $1.84 million at 30 June 2026, an eligible member under 75 may trigger up to three years of cap, or $390,000, in 2026-27. Between $1.84 million and $1.97 million the window narrows to two years ($260,000). Between $1.97 million and $2.1 million only the single-year cap of $130,000 applies. Many people who were locked out of non-concessional contributions when the general cap sat at $1.7 million or $2 million may find room again, but only if their balance on the prior 30 June sits below the new cut-offs.

Triggering bring-forward commits future years. A large contribution in July 2026 is not a free extra cap; it consumes 2027-28 and 2028-29 entitlements. Strategies such as recontribution that depend on after-tax cap space need the multi-year picture, not only the July headline.

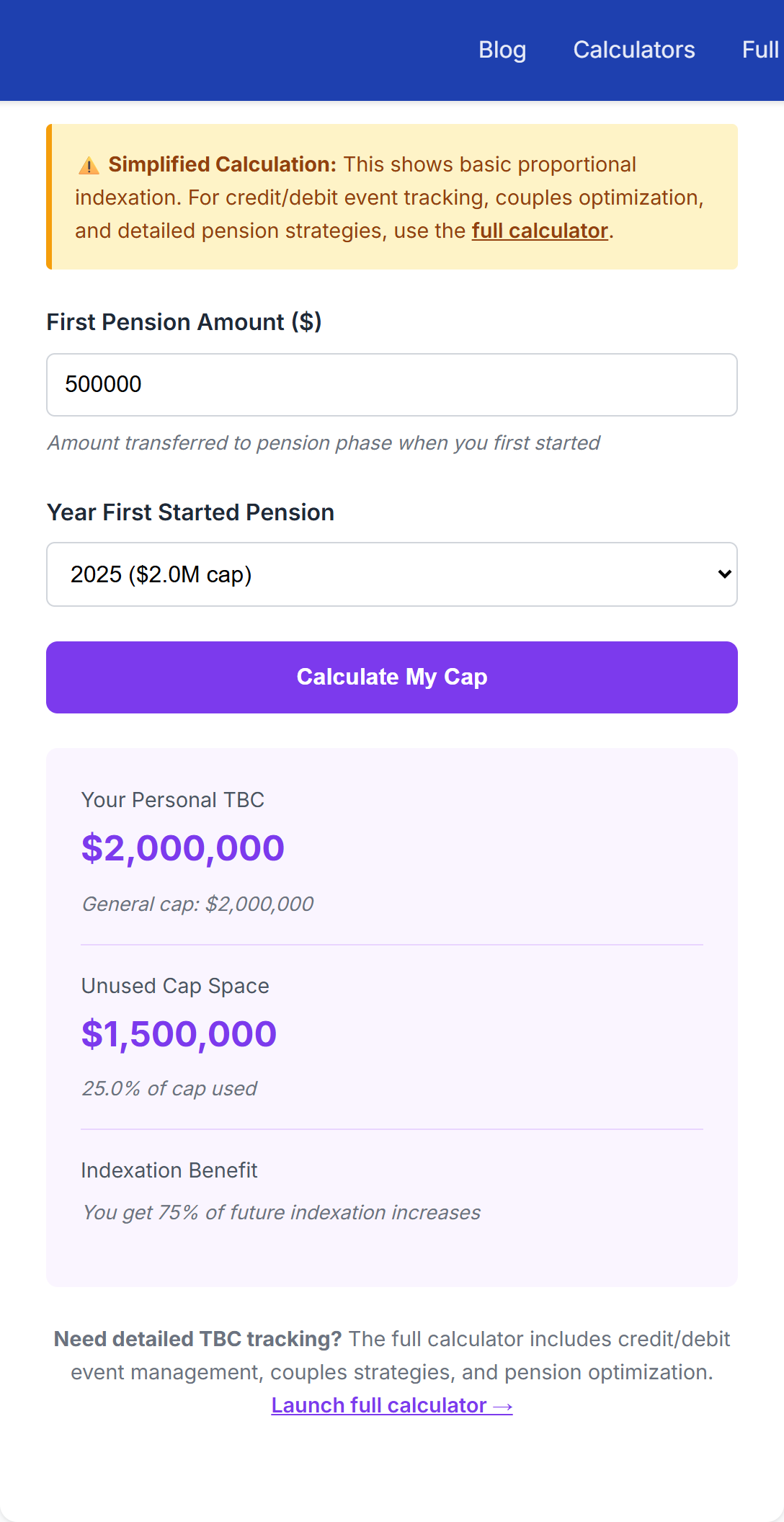

Transfer balance cap: $2.1 million

The general transfer balance cap limits how much super can support a retirement-phase pension where earnings are tax-free in the fund. From 1 July 2026 it rises to $2.1 million. Your personal cap depends on when you first entered retirement phase and how much proportional indexation the ATO has credited to your transfer balance account. Someone who used the full $1.7 million cap in 2022-23 does not automatically receive the entire accumulated indexation to $2.1 million in one step.

The higher general cap still matters for accumulation members because it sets the TSB thresholds for non-concessional eligibility. It also affects defined benefit income streams: the defined benefit income cap for tax purposes rises to $131,250 in 2026-27. Pension minimum drawdown percentages (4% under 65, 5% at 65-74, and so on) do not change on 1 July.

Advanced Calculator example: model accumulation and pension phase with caps that switch to 2026-27 values from 1 July. Set the scenario year when comparing June and July strategies in the same session.

Payday Super: timing, not a higher rate

From 1 July 2026, employers must pay Super Guarantee at the same time as salary and wages under Payday Super rules, rather than batching quarterly payments in many cases. For ongoing pay cycles, contributions must generally reach the employee's fund within seven business days of payday. For a new employee, or where it is the employer's first Super Guarantee payment to a new super fund for that worker, the first payment may be made within 20 business days instead.

Super Guarantee is calculated as 12% of qualifying earnings (QE). QE starts from ordinary time earnings and also includes all commissions, salary sacrifice amounts that would otherwise count as QE, and payments to workers under the expanded definition of employee (including independent contractors paid mainly for their labour). The main practical shifts for many employers are sacrificed amounts and contractor coverage, though commission treatment also widens under the ATO's QE rules.

The rate stays 12%. Current law does not legislate a step to 12.5% on this date. Payday Super is about payment timing and the earnings base, not a higher percentage on the payslip. Employees may notice more frequent super deposits and should check myGov or the fund portal if pays look unchanged after July while SG amounts on the payslip do move.

Division 296: additional tax on large balances

Division 296 is no longer draft policy. The Treasury Laws Amendment (Building a Stronger and Fairer Super System) Act 2026 received Royal Assent on 13 March 2026 and the tax applies from 1 July 2026. If your total super balance at the end of the financial year exceeds the large super balance threshold (set at $3 million for 2026-27), an additional 15% tax applies to the proportion of super earnings attributable to the part of your balance above that threshold. If your balance exceeds the very large super balance threshold (set at $10 million for 2026-27), a further 10% applies to the earnings proportion attributable to the part above that higher line.

Division 296 sits alongside Division 293, which still targets high income on concessional contributions above $250,000. Division 296 targets high balances regardless of salary. From later years the ATO compares your balance immediately before the financial year and at 30 June, using the higher figure. Reporting and payment run through the ATO after year end. Check current ATO guidance for how Division 296 earnings are calculated. This article does not model your liability. See the dedicated Division 296 article and ATO material for detail.

What does not change on 1 July 2026

Not everything on the retirement calendar moves with the super financial year. Age Pension rates and assets test thresholds follow Services Australia's indexation schedule, typically March and September, not 1 July. Deeming rates applied from 20 March 2026 remain in force until Services Australia announces otherwise.

Preservation age, Age Pension age (67), downsizer contribution rules, and minimum pension drawdown percentages are unchanged on this date. Individual income tax brackets were not indexed for 1 July 2026 in federal budget materials reviewed for this article. The Division 293 income threshold of $250,000 also does not index on 1 July.

30 June versus 1 July: where timing bites

Non-concessional eligibility for 2026-27 depends on total super balance at 30 June 2026, not the balance on 1 July. A withdrawal on 29 June that drops TSB below $2.1 million does not rewrite the test if the 30 June figure was already above the line. Conversely, a withdrawal after 30 June may create room for a later year but not retroactively for 2026-27 cap purposes.

Concessional contributions allocated to 2025-26 count against the $30,000 cap; from 1 July 2026 the $32,500 cap applies to new allocations. A large non-concessional contribution on 28 June 2026 falls in a different financial year, and potentially different bring-forward thresholds, than the same payment on 2 July 2026. Minimum pension payments for 2025-26 remain tied to the 1 July 2025 account balance; the 30 June deadline for meeting 2025-26 minimums has not moved.

Model 2026-27 with updated caps

See how indexed caps affect accumulation, pension phase, and long-run retirement income scenarios.

Open the Advanced CalculatorDisclaimer: This article is general information only. It is not financial product advice or personal advice. SuperCalc Pro Pty Ltd does not hold an Australian Financial Services Licence (AFSL). We do not recommend that you open, close, or change any super fund or product, or that you make particular contributions or start a pension. Tax rules, contribution caps, total super balance tests, transfer balance cap rules, and employer Super Guarantee obligations can change. For advice tailored to your situation, see the ATO, your super fund, Services Australia, or a licensed financial adviser, SMSF specialist, or tax agent.